Saving Money Tips for Paying Off Debt Faster

Optimizing Your Budget: Prioritizing Debt Payments

Understanding Your Spending Habits

A crucial first step in optimizing your budget is understanding where your money is going. This involves meticulously tracking your expenses for a set period, ideally a month. Record every single transaction, from groceries and rent to entertainment and gas. Analyzing this data will reveal patterns and areas where you might be overspending. Identifying these areas is the first step towards making informed decisions about your budget allocation. It's often surprising how much is spent on seemingly insignificant items when viewed in aggregate.

Setting Realistic Financial Goals

Effective budgeting requires clear, achievable goals. Instead of aiming for unrealistic transformations overnight, set smaller, manageable targets. For example, saving a specific amount each month for a down payment on a car or a vacation fund. These goals provide motivation and direction, keeping you focused on your financial aspirations. Breaking down large objectives into smaller, more attainable steps makes the entire process less daunting and more likely to be sustained.

Creating a Detailed Budget

Once you understand your spending habits and have defined your goals, create a detailed budget. This document should categorize your income and expenses, outlining how much you earn and how much you're allocating to different areas. Consider using budgeting apps or spreadsheets to make this process easier and more organized. Careful categorization and allocation of funds ensure that your money is working for you, rather than the other way around. This organized approach lets you see exactly where your money is going and helps you stay on track.

Prioritizing Essential Expenses

Essential expenses, such as rent, utilities, and groceries, should be prioritized in your budget. These are the costs that you absolutely need to cover to maintain a stable living situation. Prioritizing these expenses ensures that your basic needs are met before allocating funds to discretionary items. Understanding what truly constitutes a necessity versus a want is key to effectively managing your budget and creating financial stability.

Exploring Ways to Cut Unnecessary Expenses

After identifying essential expenses, evaluate areas where you can potentially cut unnecessary spending. This could involve reducing entertainment costs, finding cheaper alternatives for groceries, or negotiating lower utility rates. Identifying and eliminating unnecessary expenses frees up funds that can be redirected toward your financial goals. Explore different options, and be creative in finding ways to save money without sacrificing your quality of life.

Reviewing and Adjusting Your Budget Regularly

A budget isn't a static document; it should be reviewed and adjusted regularly. Life circumstances change, and your spending habits may evolve over time. Regular reviews ensure that your budget remains relevant and effective in helping you achieve your financial objectives. By making adjustments as needed, you can stay on track and maintain a healthy financial standing. This dynamic approach allows you to adapt to changes and continue working toward financial success.

Leveraging Savings and Investment Strategies: Amplifying Your Efforts

Understanding Your Financial Baseline

Before diving into sophisticated investment strategies, it's crucial to understand your current financial situation. This involves analyzing your income, expenses, and existing savings. A detailed budget, outlining all sources of income and how those funds are allocated, is an essential first step. Identifying areas where you can cut back on unnecessary spending can free up resources for savings and investments. Careful tracking of your spending habits and patterns will provide valuable insights into potential areas for improvement.

Thorough financial analysis allows you to pinpoint areas where savings can be maximized and to create a more stable financial foundation for future investments. Understanding your current baseline is the first step towards creating a sustainable and effective financial plan.

Establishing a Savings Plan

A savings plan is a roadmap to your financial goals. It defines specific savings targets, whether it's for a down payment on a house, a dream vacation, or simply building a financial cushion for unexpected expenses. Clearly outlining your goals will provide motivation and direction for your savings efforts. This plan should be reviewed and adjusted regularly to ensure it aligns with your evolving financial needs and aspirations.

Defining realistic and achievable savings goals is key to long-term success. Consider the timeline for your goals and allocate savings accordingly. A well-structured savings plan will make achieving your financial aspirations more manageable and less daunting.

Exploring Investment Options

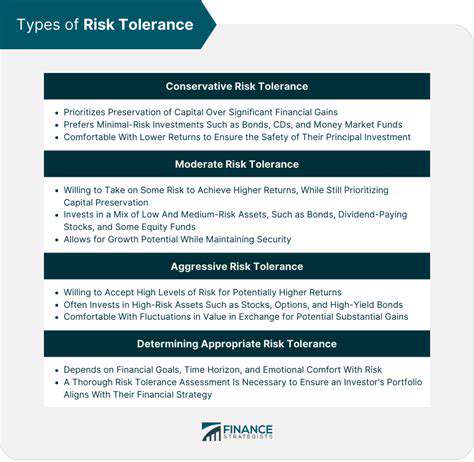

Once you have established a solid savings foundation, you can explore various investment options. Researching different investment vehicles such as stocks, bonds, mutual funds, and real estate can help you identify those that align with your risk tolerance and financial goals. Understanding the potential risks and rewards associated with each option is crucial for making informed decisions.

Diversification is another key component in successful investing. Spread your investments across different asset classes to mitigate risk and potentially enhance returns. This approach helps to balance potential losses in one area with gains in another. Seeking professional financial advice can provide valuable insights and guidance in this process.

Maximizing Savings Through Budgeting

Effective budgeting is a cornerstone of successful savings and investment strategies. Creating a detailed budget allows you to track your income and expenses, identify areas where you can cut back, and allocate funds towards savings and investments. Regularly reviewing and adjusting your budget based on your changing needs is essential for maintaining financial stability.

A well-maintained budget allows you to stay mindful of your spending habits and make conscious choices about how you allocate your resources. This awareness is crucial for long-term financial success and helps you avoid unnecessary financial stress.

Long-Term Financial Planning

Long-term financial planning involves setting goals for the future and developing strategies to achieve them. This includes considering retirement planning, education funding for children, and other significant life events. A solid financial plan will give you a clear roadmap to secure your financial future and achieve your aspirations.

Long-term financial planning encompasses a wide range of crucial considerations, from retirement savings to estate planning. It necessitates a careful evaluation of your current financial standing, anticipated future expenses, and desired lifestyle to create a comprehensive and effective strategy.

Strategies for Building Wealth

Building wealth is a multifaceted process that involves a combination of saving, investing, and managing debt effectively. Understanding different investment strategies and exploring various avenues for generating income can significantly contribute to accumulating wealth. This process often requires patience, discipline, and a long-term perspective.

Strategies for building wealth may include exploring different investment vehicles, such as real estate, stocks, or bonds. It is also important to consider how to manage debt effectively to free up more funds for investment and savings. Understanding tax implications and seeking professional financial advice are essential steps to building a secure financial future.

The Importance of Regular Review and Adjustment

Financial strategies are not static; they need to adapt to changing circumstances. Regularly reviewing your savings and investment plans, and adjusting them as needed, is essential for maintaining progress toward your goals. This process allows you to adapt to unexpected events or changes in your financial situation.

Regular reviews are vital for staying on track with your financial goals. Life throws curveballs, and your financial plan must be flexible enough to accommodate them. Reviewing and adjusting your strategies periodically ensures that your financial plan remains aligned with your current needs and aspirations, ultimately leading to greater financial security and success.

Read more about Saving Money Tips for Paying Off Debt Faster

![Best Investment Strategies for Volatile Markets [2025]](/static/images/30/2025-05/StrategicAssetAllocation3AAdaptingtoMarketConditions.jpg)

![How to Create a Monthly Budget That Works [2025 Guide]](/static/images/30/2025-05/ReviewingandRevisingYourBudgetRegularlyforLong-TermFinancialStability.jpg)

Hot Recommendations

- Budgeting for Travel: How to Save for Your Next Trip

- Guide to Understanding Retirement Account Rollovers

- Understanding Sector Rotation Strategy

- How to Choose Beneficiaries for Your Assets

- How to Combine Value and Growth Investing Strategies

- How to Use Stop Loss Orders When Investing

- How to Use Day Trading Strategy (High Risk)

- Understanding Investment Diversification

- How to Use a Core Satellite Investment Strategy

- Understanding Preferred Stocks