How to Build an Emergency Fund [Step by Step]

Contents

Emergency reserves are used to respond to unexpected expenses and alleviate financial pressure.

Determine reserve target amount through monthly expenditure assessment.

It is recommended to reserve 3-6 months of living expenses as a safety net.

Customize a dedicated reserve plan based on individual circumstances.

Adjust reserve targets dynamically according to changes in financial situation.

An automated saving mechanism ensures continuous accumulation of funds.

Make good use of budgeting tools to accurately control financial dynamics.

Develop a feasible savings plan that matches financial goals.

Utilize community supervision to maintain saving discipline.

Maintain saving motivation through phase rewards.

Replenish the emergency fund pool promptly after unexpected expenses.

Establish a clear trigger mechanism for fund replenishment.

Record financial progress to optimize fund management efficiency.

Step 1: Determine Target Reserve Amount

The Core Value of Emergency Reserves

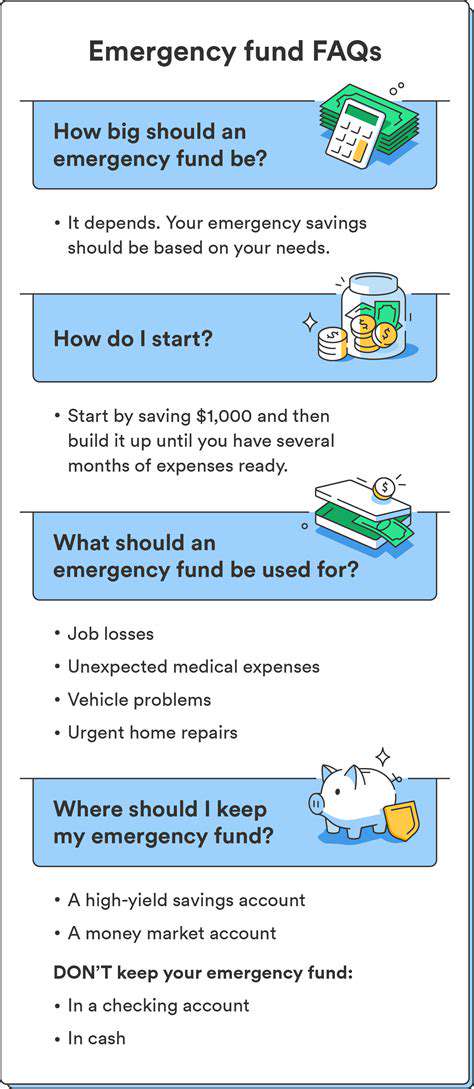

This financial parachute can cushion economic shocks during unforeseen circumstances and prevent falling into debt traps. Federal Reserve data shows that about 38% of American citizens cannot afford an unexpected expense of $400, highlighting the urgency of establishing a secure reserve. When a vehicle breaks down or an unexpected illness occurs, adequate reserves allow you to cope calmly without affecting your normal life.

Monthly Expenditure Overview

It is recommended to use a three-tier recording method: basic living expenses (rent/mortgage, utilities), necessary living costs (food, transportation), and discretionary spending (entertainment, dining out). By keeping accounts for three months, you can capture easily overlooked periodic expenses (such as annual insurance premiums).

Personalized Reserve Standards

It is recommended to consider income stability as the core factor: fixed salary earners can use a 3-month benchmark, while freelancers are advised to aim for 6-9 months of reserves. Families with members who have chronic illnesses can add an extra 15% medical reserve, and those with underage children should account for emergency education expenses.

Dynamic Adjustment Mechanism

Review reserve targets quarterly; significant life changes (promotion/unemployment/marriage/childbirth) should prompt immediate reassessment. When mortgage rates rise by 2%, timely adjustments to the reserve base are necessary to maintain fund coverage effectiveness.

Step 2: Set Monthly Savings Goals

Financial Sandbox Simulation

Use reverse budgeting: first deduct the savings amount and then allocate remaining funds. If the monthly income is 6000 yuan, try saving 20%, or 1200 yuan, by gradually adapting to a new budget structure through reducing non-essential spending (e.g., switching from dining out to packing lunch).

Stepwise Goal Setting

Beginner's advice is to adopt the 333 progressive method: save 3% of income in the first month, 6% in the second month, and 9% in the third month, gradually cultivating the saving habit. The key is to establish a mindset of prioritizing paying yourself and view savings as an irreversible regular bill.

Assistance from Smart Tools

It is recommended to use a budgeting app with AI analysis features (e.g., MoneyCoach) that automatically recognizes spending patterns and generates optimization suggestions. Set spending warning thresholds (e.g., when dining expenses exceed budget by 10%, automatically remind), improving fund control precision.

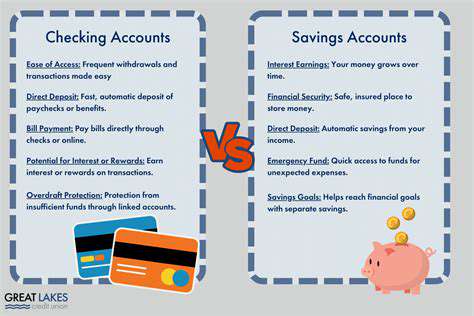

Step 3: Select Optimal Savings Accounts

Three Dimensions of Account Selection

Liquidity, profitability, and security constitute the golden triangle: preferentially choose money market funds that support instant redemption (annualized 2-3%), avoiding structured deposits with redemption limits. Be sure to diversify, keeping one month’s expenses in the main account while allocating the remainder to a 90-day notice deposit for higher returns.

Bank Service Comparison

Compare the hidden benefits of different institutions: some banks offer free financial planning services, while certain online banks provide account security insurance as a gift. It is advisable to open two accounts: an emergency account for daily needs (liquid) + a value-added reserve account (fixed).

Step 4: Build a Sustainable Savings System

Behavior Reinforcement Strategies

Use visual progress management: post a savings progress chart in the kitchen, filling a box for every 500 yuan saved. Join an online saving challenge community to maintain motivation through peer pressure. Research shows that public commitments can increase goal achievement rates by 65%.

Flexible Adjustment Plan

Design a buffer mechanism: when unexpected overspending occurs, allow the use of that month’s entertainment budget to make up for savings, but require double the deposit in the next month. This maintains discipline while avoiding abandonment of the plan due to excessive strictness.

Step 5: Emergency Fund Maintenance Mechanism

Smart Replenishment Strategy

Establish a dual-trigger mechanism: automatically initiate replenishment procedures when fund usage exceeds 30% or when the interval exceeds 6 months. Prioritize using additional income (bonuses/tax refunds) for replenishment to keep daily saving rhythm unaffected.

Fund Effectiveness Audit

Conduct stress tests every six months: simulate scenarios such as unemployment for 3 months or medical expenses of 20,000 yuan to test fund coverage capability. Adjust the reserve structure based on test results, converting part of the funds into more flexible allocations if necessary.

Read more about How to Build an Emergency Fund [Step by Step]

Hot Recommendations

- Tax Planning Tips for Homeowners [2025]

- How to Get Insurance for a Short Term Rental Property

- Understanding the Benefits of a Roth IRA

- How to Manage Business Debt After a Downturn

- How to Use a Barbell Investment Strategy

- Best Ways to Track Your Progress Towards Financial Freedom

- Tips for Managing Credit Card Rewards While Paying Off Balances

- Tax Planning Tips for Stock Options

- How to Plan for Retirement if You Didn't Save Early

- Guide to Managing Legal Debt