Tips for Avoiding Payday Loan Traps

Decoding the Nuances of Contractual Language

Understanding contracts is crucial for any transaction, big or small. Often, the seemingly simple language can hide complex clauses and potential pitfalls. Careful scrutiny of the fine print is essential to ensure you fully grasp the terms and conditions before signing. This involves not only reading every word but also understanding the context and implications of each clause. You should seek professional legal advice if you are unsure about any part of a contract, as this can save you significant headaches down the line. Reviewing the entire document, paragraph by paragraph, can be beneficial for a clear understanding of the agreement.

Contracts are legally binding agreements, and the language within them carries significant weight. Misinterpretations or overlooked details can lead to costly errors or disputes. Thus, taking the time to thoroughly review the fine print is paramount to safeguarding your interests. Understanding the specific rights and obligations outlined within the document is imperative for a successful and equitable outcome. This includes identifying potential clauses that might be unfavorable or ambiguous.

Identifying Potential Risks and Clauses

Contracts often contain clauses that may present risks or limitations. These clauses might involve liability, indemnification, or specific performance. Identifying these clauses and understanding their implications is crucial to evaluating the overall risk associated with the agreement. For instance, a clause that limits liability could protect one party while potentially exposing the other to significant financial loss. Therefore, a detailed examination of all sections is necessary for a complete understanding.

Another key element is the identification of clauses that may be ambiguous or unclear. These ambiguous clauses can lead to disputes and legal challenges. Clarifying these ambiguities with the other party or seeking legal counsel can help prevent potential problems later. By thoroughly scrutinizing the language, you can proactively identify potential risks and mitigate any potential issues down the road. It is important to be aware of any clauses that deviate from standard industry practices.

Negotiating Terms and Seeking Clarification

Don't be afraid to negotiate terms that don't align with your interests. You have the right to ask questions and seek clarification on any aspect of the contract you don't fully understand. If a clause is unclear or potentially disadvantageous, actively seek clarification. This proactive approach demonstrates your due diligence and can lead to a more favorable agreement. Communication is key; don't hesitate to discuss your concerns with the other party.

If you are not satisfied with the terms, you have the option to renegotiate or decline the agreement altogether. Seeking advice from a legal professional can provide valuable insights and guidance throughout the negotiation process. This process helps ensure you understand the contract's implications fully before committing. Remember, you are not obligated to accept a contract that does not meet your needs or protect your interests.

Thorough comprehension of the contract and its terms is crucial for safeguarding your interests. Reviewing the contract carefully, understanding the implications of each clause, and actively seeking clarification when needed are essential steps in the process.

Budgeting for Success: Creating a Financial Plan

Understanding Your Income and Expenses

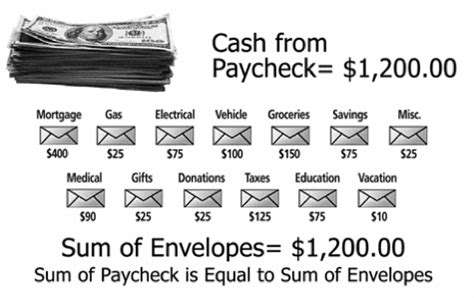

A crucial first step in successful budgeting is understanding your income and expenses. This involves meticulously tracking every source of income, from your salary to any side hustles or investment earnings. Detailed records of your income provide a clear picture of your financial capacity. Simultaneously, meticulously document all your expenses, categorizing them into essential (housing, utilities, food) and discretionary (entertainment, dining out) expenditures. This comprehensive analysis forms the bedrock for establishing a realistic and achievable budget.

Analyzing income and expenses reveals spending patterns and areas where adjustments can be made. Identifying unnecessary expenses, like frequent takeout or subscriptions you rarely use, allows you to allocate those funds more strategically. This awareness empowers you to make informed decisions about your money and prioritize your financial well-being.

Setting Realistic Financial Goals

Defining your financial goals is paramount to effective budgeting. Whether it's saving for a down payment on a house, paying off debt, or building an emergency fund, establishing clear targets provides direction and motivation. These goals should be specific, measurable, achievable, relevant, and time-bound (SMART). For example, save $5,000 for a down payment by the end of the year is a more effective goal than simply save more money.

Realistic goals are attainable and aligned with your current financial situation. Setting ambitious but achievable goals fosters a sense of accomplishment and encourages consistent progress toward your financial aspirations. This process of establishing and pursuing goals is integral to achieving financial stability and security.

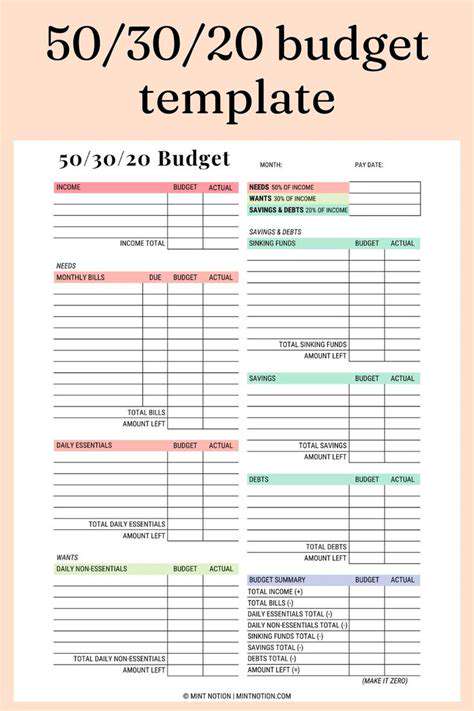

Creating a Detailed Budget

A detailed budget is a roadmap for your finances, outlining how much money you'll allocate to different categories. This plan should be flexible enough to accommodate unexpected expenses but rigid enough to keep you on track with your financial goals. Categorize your expenses into essential (housing, utilities, food) and discretionary (entertainment, dining out) to gain a comprehensive overview of your spending habits.

Using budgeting apps or spreadsheets can help you track your progress and stay organized. Regular review and adjustments are key to maintaining a budget that aligns with your evolving needs and circumstances.

Tracking Your Spending and Making Adjustments

Regularly tracking your spending is essential to stay informed about your financial health. This process allows you to identify areas where you might be overspending and make necessary adjustments. Comparing your actual spending to your budget reveals discrepancies and highlights areas requiring attention. Using budgeting apps or spreadsheets, or even a simple notebook and pen, can help you monitor your spending effectively.

Building an Emergency Fund

Establishing an emergency fund is crucial for financial stability. This fund acts as a safety net to protect you from unexpected expenses, like medical emergencies or job loss. Aim to save enough to cover three to six months of living expenses. The more you can save, the more prepared you'll be to handle unforeseen circumstances.

Utilizing Resources for Financial Guidance

Seeking financial guidance from experts or utilizing resources like budgeting apps and online tools can significantly aid in creating and maintaining a successful budget. These resources can offer valuable insights into managing your finances effectively. Financial advisors, workshops, and online communities can provide support and guidance to navigate budgeting complexities.

Avoiding Payday Loans and High-Interest Debt

Budgeting plays a vital role in avoiding payday loans and high-interest debt. By creating a comprehensive budget, you gain a clearer understanding of your income and expenses, allowing you to anticipate and manage your financial needs proactively. Knowing your financial limitations prevents you from resorting to costly short-term solutions, such as payday loans, which often come with exorbitant interest rates and can quickly spiral into debt.

Building a Financial Safety Net: Emergency Fund Essentials

Understanding Your Financial Needs

Assessing your current financial situation is crucial for building a robust safety net. This involves meticulously evaluating your income, expenses, and existing assets. Understanding your monthly income and all your expenses, including fixed costs like rent or mortgage and variable costs like groceries and entertainment, is essential to identifying potential vulnerabilities. Accurate budgeting is the cornerstone of a strong financial foundation.

Identifying your short-term and long-term financial goals is also key. What are your immediate needs? What are your future aspirations? Planning for unexpected events like job loss, medical emergencies, or home repairs is vital. These factors will help you determine how much financial cushioning you need to create.

Creating a Budget and Tracking Expenses

A well-structured budget is the bedrock of any successful financial plan. It should detail your income sources, categorize your expenses, and allocate funds for various needs. Regularly reviewing and adjusting your budget is essential to maintain its effectiveness. Be sure to account for all potential expenditures, both recurring and one-time, to ensure you have a realistic picture of your financial health.

Implementing a system for tracking your expenses is also vital. This can be as simple as using a spreadsheet or a dedicated budgeting app. The key is to monitor your spending habits and identify areas where you can potentially cut back. By understanding where your money is going, you can make informed decisions about saving and investing.

Building an Emergency Fund

An emergency fund is a crucial component of any financial safety net. It acts as a buffer against unexpected financial hardships. Aim for a minimum of three to six months' worth of living expenses in your emergency fund. This crucial financial cushion will provide you with the peace of mind needed to face unforeseen circumstances without jeopardizing your long-term financial stability. Having an emergency fund can significantly reduce stress and anxiety during difficult times.

Contributing consistently to your emergency fund is important. Even small, regular contributions can add up over time. Consider automating these contributions to ensure they are consistently met. This ensures that you're consistently building your financial safety net.

Investing and Diversifying Your Assets

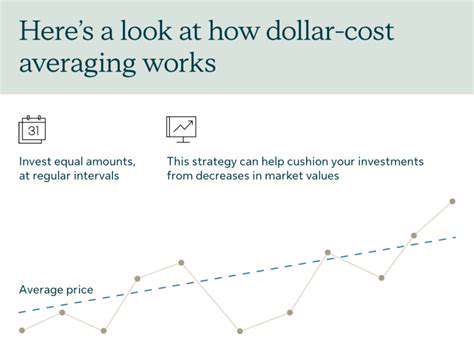

Investing and diversifying your assets is a long-term strategy for building wealth and securing your financial future. Exploring various investment options, like stocks, bonds, or mutual funds, can help you grow your money over time. Diversification across different asset classes can help mitigate risk and potentially enhance returns. This long-term approach is essential for financial security and growth.

Seeking professional financial advice can be beneficial in navigating the complexities of investing. A financial advisor can help you develop a personalized investment strategy that aligns with your financial goals and risk tolerance. They can also guide you through the process of diversifying your assets across different investment avenues.

Read more about Tips for Avoiding Payday Loan Traps

![How to Build an Emergency Fund [Step by Step]](/static/images/30/2025-04/Step53AReplenishYourEmergencyFundWhenNecessary.jpg)

![Best Budgeting Software for Families [2025]](/static/images/30/2025-05/EvaluatingPopularBudgetingSoftwareOptionsforFamilies.jpg)

Hot Recommendations

- Tax Planning Tips for Homeowners [2025]

- How to Get Insurance for a Short Term Rental Property

- Understanding the Benefits of a Roth IRA

- How to Manage Business Debt After a Downturn

- How to Use a Barbell Investment Strategy

- Best Ways to Track Your Progress Towards Financial Freedom

- Tips for Managing Credit Card Rewards While Paying Off Balances

- Tax Planning Tips for Stock Options

- How to Plan for Retirement if You Didn't Save Early

- Guide to Managing Legal Debt