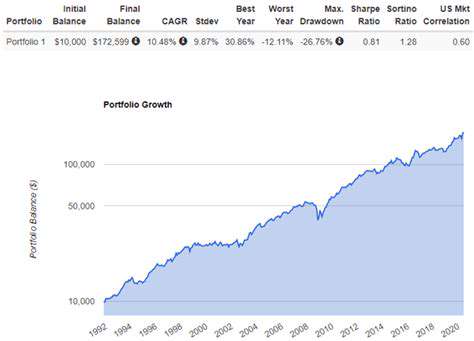

Understanding Risk Parity in Portfolio Management

Advantages of Risk Parity

Improved Portfolio Diversification

Risk parity, by its very nature, encourages a more diversified portfolio allocation. Instead of focusing on maximizing returns from individual asset classes, it aims for a balanced representation of risk across those classes. This approach reduces the concentration of risk in any single asset or sector, leading to a more resilient portfolio. This diversification mitigates the impact of poor performance in one segment, as the overall portfolio is less susceptible to large swings in value due to the balanced risk profile.

A diversified portfolio, built on the principles of risk parity, is less likely to experience significant losses during market downturns. This is because the reduced exposure to any single risk factor results in a portfolio that is more stable and less volatile in the face of uncertainty. The reduced correlation between asset classes further enhances this diversification effect, leading to greater overall portfolio stability.

Enhanced Portfolio Return Potential

While risk parity prioritizes risk balancing, it doesn't necessarily sacrifice potential returns. By carefully calculating the appropriate allocations based on the individual risk characteristics of each asset class, risk parity can actually optimize the portfolio's return potential. This means that while the portfolio is spread across different asset classes, the overall return can still be substantial and competitive with other investment strategies.

Optimized Risk-Adjusted Returns

A key advantage of risk parity is its ability to optimize risk-adjusted returns. Risk parity explicitly considers the risk characteristics of various asset classes, unlike traditional approaches that often overlook this critical aspect. This focus on risk-adjusted returns ensures that the portfolio's return is commensurate with the level of risk undertaken. This is a crucial aspect of portfolio management, as investors seek to maximize returns while minimizing the potential for losses.

By effectively managing the risk-return trade-off, risk parity can lead to portfolios that deliver superior risk-adjusted returns compared to portfolios created through other methods. This optimization is achieved through the precise allocation of capital across different asset classes, ensuring a balance between risk and reward.

Reduced Volatility and Increased Portfolio Stability

Risk parity aims for a significant reduction in portfolio volatility. By distributing risk evenly across various asset classes, the overall portfolio becomes less sensitive to market fluctuations. This stability is crucial for investors who prioritize preserving capital and minimizing the impact of market downturns on their investment returns. The focus on diversification, inherent in risk parity, leads to a portfolio that is more resilient to unexpected market shocks, thereby safeguarding the principal amount.

Reduced volatility translates directly into increased portfolio stability. This means less frequent and less severe fluctuations in the portfolio's value. This stability is particularly important for long-term investors, as it reduces the anxiety associated with significant market swings and enhances the likelihood of achieving long-term investment goals.

Limitations and Considerations

Understanding Diversification Limitations

Diversification, a cornerstone of risk parity, aims to reduce portfolio volatility by allocating capital across different asset classes. However, complete diversification is often unattainable. Correlation between asset classes can still exist, leading to situations where a downturn in one sector impacts others, mitigating the intended benefit of diversification. This inherent limitation necessitates careful consideration of correlation matrices and historical performance data to optimize diversification strategies.

Furthermore, the assumption that all assets will react identically to market events is a simplification. Economic shocks and geopolitical events can introduce unforeseen correlations, further complicating the effectiveness of diversified strategies. A risk parity portfolio, while striving for broad diversification, isn't immune to these systemic risks. Effective managers must continuously monitor and adapt their strategies to changing market conditions.

Assessing Market Volatility

Risk parity strategies heavily depend on accurate assessments of market volatility. Fluctuations in market sentiment, economic indicators, and geopolitical events can cause unpredictable swings in asset prices. An overestimation or underestimation of volatility can lead to misallocation of capital and negatively impact portfolio performance. Therefore, consistent and reliable volatility analysis is crucial for the success of a risk parity strategy.

The historical volatility of asset classes can be a useful metric, but it doesn't always predict future behavior. External factors can dramatically alter market dynamics, rendering historical data less reliable for future forecasting. Active monitoring and updating of volatility models are essential for optimizing the strategy and mitigating potential losses.

Evaluating Transaction Costs

While risk parity aims for optimal portfolio construction, the practical implementation involves transactions. Buying and selling assets incurs transaction costs, which can erode potential returns. High-frequency trading or rapidly changing market conditions can exacerbate these costs, making it challenging to maintain the intended risk parity allocation.

These costs need to be carefully factored into the strategy's design. Choosing suitable investment vehicles, understanding brokerage commissions, and utilizing appropriate trading platforms are key to minimizing the impact of transaction costs on portfolio performance. A robust risk parity strategy should account for these costs to ensure that the theoretical benefits outweigh the practical expenses.

Impact of Asset Liquidity

The liquidity of assets plays a significant role in the execution of risk parity strategies. Illiquid assets, characterized by difficulty in quick and efficient trading, can pose significant challenges. Trying to rebalance a portfolio with illiquid assets can be particularly problematic, demanding more complex strategies and potentially higher transaction costs. Furthermore, the value of illiquid assets may be harder to accurately ascertain, which can impact the accuracy of risk assessment in a risk parity portfolio.

Data Dependency and Model Accuracy

Risk parity relies heavily on data and models for asset allocation and risk assessment. The quality, accuracy, and timeliness of this data are critical to the success of the strategy. Inaccurate data or outdated models can lead to misallocation of capital and negatively impact portfolio returns.

The models used to calculate risk and return need to be regularly validated and updated to ensure their continued relevance. Data collection practices and model sophistication are crucial to minimizing potential inaccuracies and maximizing the strategy's effectiveness. In a dynamic market, adaptation and refinement of both data input and modeling techniques are essential to managing risk.

Managerial Expertise and Active Monitoring

A risk parity strategy, despite its mathematical underpinnings, requires significant managerial expertise. Interpreting market trends, adjusting to changing conditions, and overseeing the portfolio's performance are critical responsibilities. Effective managers must possess a deep understanding of financial markets, asset classes, and the strategy's limitations.

Active monitoring and adjustments are essential. Regular portfolio rebalancing, market research, and adaptation to unforeseen events are crucial to the strategy's success. The manager must continuously evaluate and refine the strategy to ensure it remains aligned with the investor's goals and risk tolerance in a constantly evolving market.

Read more about Understanding Risk Parity in Portfolio Management

Hot Recommendations

- Tax Planning Tips for Homeowners [2025]

- How to Get Insurance for a Short Term Rental Property

- Understanding the Benefits of a Roth IRA

- How to Manage Business Debt After a Downturn

- How to Use a Barbell Investment Strategy

- Best Ways to Track Your Progress Towards Financial Freedom

- Tips for Managing Credit Card Rewards While Paying Off Balances

- Tax Planning Tips for Stock Options

- How to Plan for Retirement if You Didn't Save Early

- Guide to Managing Legal Debt