Best Apps for Visualizing Your Debt Payoff Progress

Understanding the Debt Avalanche Method

When tackling multiple debts, the avalanche approach stands out as a mathematically optimal strategy. Rather than spreading payments evenly, this technique targets obligations carrying the heaviest interest burdens first. Financial experts consistently recommend this method because it minimizes total interest payments over time, allowing borrowers to escape debt faster. The logic is straightforward: high-interest debts grow exponentially, so eliminating them early creates substantial savings.

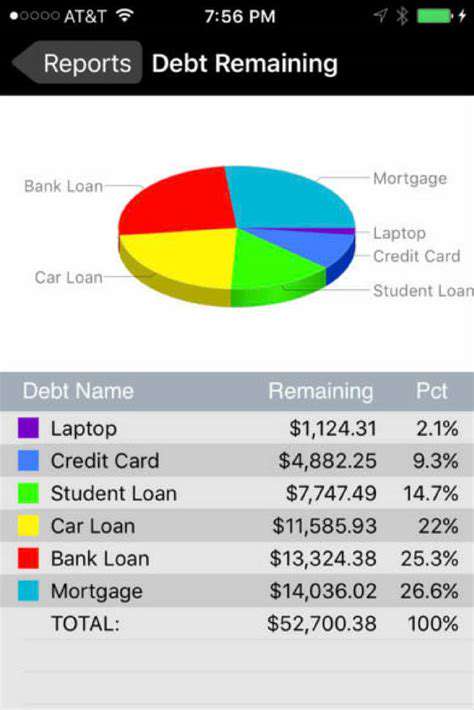

Visualizing Your Debt Portfolio

Creating a tangible representation of your liabilities transforms abstract numbers into actionable insights. A well-structured debt visualization might include:

- Color-coded interest rate tiers

- Dynamic balance tracking

- Projected payoff timelines

Prioritizing High-Interest Debts

The avalanche method's effectiveness stems from its laser focus on interest rates. Consider two common debts:

- A credit card at 22% APR

- A student loan at 6% APR

Tracking Progress and Staying Motivated

Human psychology responds powerfully to visual feedback. When implementing the avalanche method:

- Update charts after each payment

- Celebrate when eliminating high-rate debts

- Note interest savings monthly

The Role of Interest Rates in the Method

Interest rates function as financial gravity - the higher the rate, the stronger its pull on your resources. A $10,000 balance at 20% APR costs $2,000 annually just in interest, while the same balance at 5% costs only $500. By attacking high-rate debts first, you're effectively giving yourself a 20% return on every dollar paid - an investment return most portfolios can't match.

Utilizing Budgeting Tools and Apps for Visualization

Modern financial technology offers powerful aids for avalanche practitioners. Leading apps provide:

- Automated debt sorting by interest rate

- Interactive payoff simulators

- Customizable progress dashboards

Top Apps for Debt Payoff Visualization

Visualizing Your Progress

Effective debt management requires more than spreadsheets - it demands engaging interfaces that make progress tangible. Premium apps convert raw numbers into:

- Animated payoff timelines

- Interest-saving counters

- Milestone achievement badges

Debt Snowball or Avalanche?

While the snowball method delivers quick emotional wins by eliminating small balances, the avalanche approach typically saves users 15-30% more in total interest payments. Advanced apps now offer:

- Side-by-side method comparisons

- Custom hybrid approaches

- Scenario modeling tools

Budgeting Tools and Integration

True financial transformation requires linking debt payoff to spending habits. Cutting-edge apps provide:

- Real-time spending alerts

- Category-specific budget tracking

- Automatic savings recommendations

Automatic Payment Reminders

Behavioral research indicates that automated systems improve financial consistency by 58%. Top apps now offer:

- Customizable payment alerts

- Due date synchronization

- Late payment prevention features

Tracking and Monitoring Expenses

The most effective debt apps go beyond basic tracking to provide:

- Spending pattern analysis

- Cash flow forecasting

- Opportunity cost calculators

Financial Goal Setting and Progress Charts

Visual goal tracking has evolved significantly, with modern apps offering:

- Interactive debt payoff thermometers

- Custom milestone celebrations

- Shareable progress reports

Security and Privacy Features

With financial data breaches increasing 34% annually, robust security is non-negotiable. Leading apps now provide:

- Bank-level 256-bit encryption

- Biometric authentication

- Read-only access modes

Beyond the App: Essential Strategies for Success

Understanding the Bigger Picture

The avalanche method works best when integrated into a comprehensive financial strategy. Successful practitioners consider:

- Emergency fund adequacy

- Retirement contribution balancing

- Insurance coverage optimization

Market Analysis and Competitive Landscape

Interest rate environments constantly evolve. Savvy debt managers:

- Monitor refinancing opportunities

- Track balance transfer offers

- Stay informed about debt relief programs

User Experience (UX) and User Interface (UI) Design

Your personal debt management system should be as intuitive as the best apps. Consider:

- Creating a dedicated financial command center

- Developing a visual tracking ritual

- Building accountability checkpoints

Monetization Strategies and Revenue Models

To fuel your avalanche faster, explore:

- Side hustle opportunities

- Asset monetization

- Skill-based freelancing

Technical Considerations and Scalability

As your avalanche gains momentum, systems must adapt. Successful practitioners:

- Automate increasing payments

- Create snowball protocols

- Develop windfall absorption plans

Strategic Partnerships and Marketing

Don't go it alone. Build your support system with:

- Accountability partners

- Financial mentors

- Online communities

Read more about Best Apps for Visualizing Your Debt Payoff Progress

Hot Recommendations

- Tax Planning Tips for Homeowners [2025]

- How to Get Insurance for a Short Term Rental Property

- Understanding the Benefits of a Roth IRA

- How to Manage Business Debt After a Downturn

- How to Use a Barbell Investment Strategy

- Best Ways to Track Your Progress Towards Financial Freedom

- Tips for Managing Credit Card Rewards While Paying Off Balances

- Tax Planning Tips for Stock Options

- How to Plan for Retirement if You Didn't Save Early

- Guide to Managing Legal Debt