How to Avoid Taking on More Debt

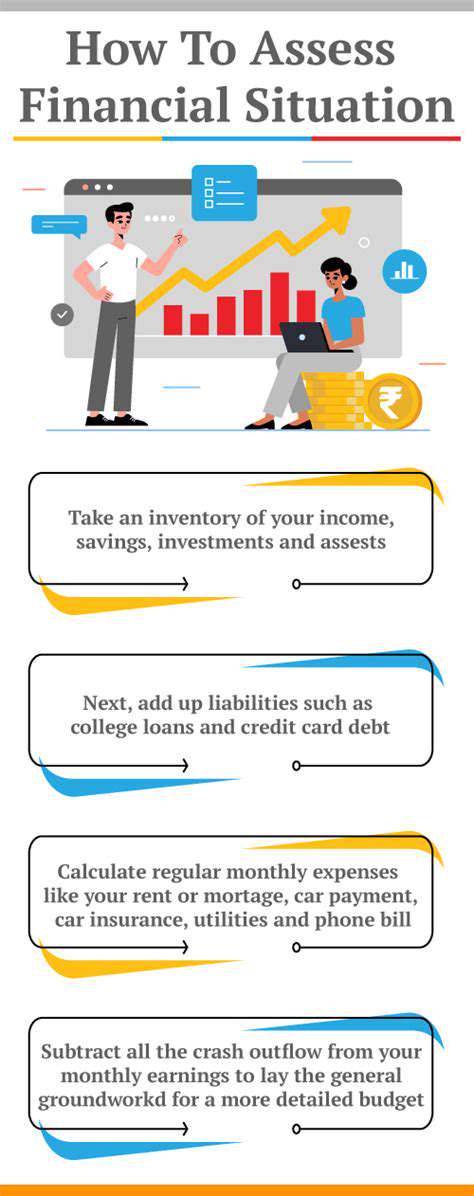

Assess Your Current Financial Situation

Understanding Your Income and Expenses

A crucial first step in assessing your financial situation is to meticulously track your income and expenses. This involves documenting every source of income, whether it's your salary, freelance work, or investments. Detailed records of all your expenses are equally important, encompassing everything from rent or mortgage payments to groceries, utilities, and entertainment. By understanding where your money is coming from and where it's going, you can identify potential areas of improvement and develop a more effective financial plan. This comprehensive understanding is the foundation for making informed financial decisions.

Categorizing your expenses can provide valuable insights. For instance, grouping expenses into essential categories like housing, food, and transportation allows you to quickly identify areas where you might be overspending. Regular review of these categories can reveal spending habits that can be adjusted to better align with your financial goals. This process of tracking and categorizing your finances is vital to gain a clear picture of your current financial health and pinpoint areas that require attention.

Evaluating Your Assets and Liabilities

Beyond income and expenses, a complete financial assessment requires evaluating your assets and liabilities. Assets represent things of value you own, such as cash, savings accounts, investments, and property. Liabilities, on the other hand, represent your outstanding debts, including loans, credit card balances, and other financial obligations. Understanding the balance between your assets and liabilities is crucial for determining your net worth.

Analyzing your assets and liabilities gives you a clearer picture of your financial standing. A detailed breakdown allows you to understand the extent of your financial obligations and how they compare to your financial resources. This evaluation is essential for making informed decisions about saving, investing, and managing debt.

Developing a Budget and Financial Plan

Once you have a clear understanding of your income, expenses, assets, and liabilities, you can start to develop a budget and a comprehensive financial plan. A budget acts as a roadmap, outlining your income and expenses for a specific period. It helps you allocate your resources effectively and ensure that your spending aligns with your financial goals. Crucially, a budget allows you to identify areas where you can cut costs and save more.

Developing a financial plan, building upon the budget, extends beyond simply tracking expenses. It encompasses long-term goals such as saving for retirement, buying a house, or funding your children's education. A well-structured financial plan provides a roadmap for achieving these goals, outlining the necessary steps and strategies to reach them. It's a dynamic document that needs to be reviewed and adjusted regularly as your circumstances change.

Prioritize Debt Repayment and Avoid New Borrowing

Prioritizing Existing Debt

A crucial step in avoiding further debt accumulation is prioritizing the repayment of existing debts. This involves analyzing your current financial situation, identifying all outstanding loans, credit cards, and other forms of debt. Categorize these debts by interest rates, minimum payments, and the potential impact on your financial health if not addressed promptly. Prioritizing high-interest debts, such as credit cards with variable interest rates, is often a good starting point, as these can quickly snowball into significant financial burdens if left unchecked. Establishing a repayment plan that takes into account your budget and financial goals is essential for effective debt management.

Once you've identified your debts, create a detailed repayment plan. This should include specific targets for each debt, including when you aim to pay off each one. Consistency in making payments, even if they are minimal at first, is key to demonstrating your commitment to reducing your debt burden. Remember, even small, consistent payments contribute to your overall progress and demonstrate fiscal responsibility to lenders and creditors.

Understanding Your Budget and Spending Habits

Effective debt management hinges on a thorough understanding of your income and expenses. A detailed budget is a vital tool in this process. Track your income sources and all your expenses, meticulously noting every detail, from daily necessities to discretionary spending. This allows you to identify areas where you might be overspending and pinpoint opportunities to cut back on unnecessary expenses. Identifying areas where you can reduce spending will help free up funds for debt repayment.

Regularly reviewing your budget is critical to ensure its effectiveness. Changes in income or spending patterns often necessitate adjustments to your budget. Be prepared to make modifications as needed to stay on track with your debt repayment goals and achieve financial stability.

Avoiding New Debt

A critical aspect of avoiding further debt is actively avoiding new borrowing. This means carefully considering any new loan or credit card applications. Before applying for any new credit, assess your current financial situation and determine if you truly need the additional borrowing. This proactive approach prevents unnecessary debt from accumulating and allows you to focus on paying off your existing debts. A clear understanding of your financial situation will help you avoid impulsive decisions that could lead to further debt.

Be wary of high-interest loans or credit cards, as these can quickly increase your overall debt burden. Evaluate the terms and conditions of any new borrowing opportunity carefully, considering interest rates, fees, and repayment schedules. This meticulous assessment will help you determine if the loan or credit card is truly beneficial or if it will contribute to further financial strain.

Evaluating Credit Card Usage

Credit card debt often poses a significant challenge in managing personal finances. To minimize the risk of accumulating further credit card debt, carefully monitor your spending and ensure your spending aligns with your budget. Establish strict limits on credit card usage, ensuring you only spend what you can comfortably afford to repay. Understanding your credit card spending habits is key to avoiding overspending and subsequent debt accumulation.

Regularly review your credit card statements to identify any unauthorized charges or errors. Promptly report any discrepancies to the credit card issuer to prevent further financial issues. This proactive approach to monitoring your credit card usage will help prevent unexpected debt and maintain financial stability.

Creating a Realistic Repayment Strategy

Developing a realistic repayment strategy is essential for effectively managing your debts and avoiding further borrowing. This strategy should consider your current financial situation, including your income, expenses, and existing debts. It's crucial to avoid setting unrealistic repayment goals that could lead to stress and financial instability. A gradual, manageable repayment plan is key to long-term financial success.

Consider seeking professional financial advice if needed. A financial advisor can provide personalized guidance and help you create a tailored repayment strategy that aligns with your specific circumstances and financial goals. Remember, financial stability is a journey, not a destination, and building a sustainable plan is key to achieving your long-term financial aspirations.

Read more about How to Avoid Taking on More Debt

![Best Homeowners Insurance Companies [2025 Review]](/static/images/30/2025-05/TopTierHomeownersInsuranceProvidersin2025.jpg)

![How to Pay Off Credit Card Debt Fast [Proven Strategies]](/static/images/30/2025-05/StayMotivatedandConsistent3AKeytoLong-TermSuccess.jpg)

Hot Recommendations

- Tax Planning Tips for Homeowners [2025]

- How to Get Insurance for a Short Term Rental Property

- Understanding the Benefits of a Roth IRA

- How to Manage Business Debt After a Downturn

- How to Use a Barbell Investment Strategy

- Best Ways to Track Your Progress Towards Financial Freedom

- Tips for Managing Credit Card Rewards While Paying Off Balances

- Tax Planning Tips for Stock Options

- How to Plan for Retirement if You Didn't Save Early

- Guide to Managing Legal Debt