How to Manage Business Debt After a Downturn

Developing a Realistic Repayment Plan: Prioritizing and Strategizing

Understanding Your Financial Situation

A crucial first step in developing a realistic repayment plan is a thorough understanding of your current financial situation. This involves analyzing all sources of income, including salary, side hustles, and any other potential revenue streams. Accurately documenting all recurring and one-time expenses is equally important. This includes housing costs, utilities, transportation, food, entertainment, and any other debts or obligations. Understanding your current cash flow and identifying areas where you can cut back or increase income will be instrumental in creating a sustainable repayment plan.

Detailed budgeting is essential. Categorize your expenses to pinpoint areas where you can potentially reduce spending. Tracking your spending for a month or two will provide valuable insights into your spending habits and identify potential areas for improvement. This knowledge empowers you to make informed decisions about allocating your resources for debt repayment.

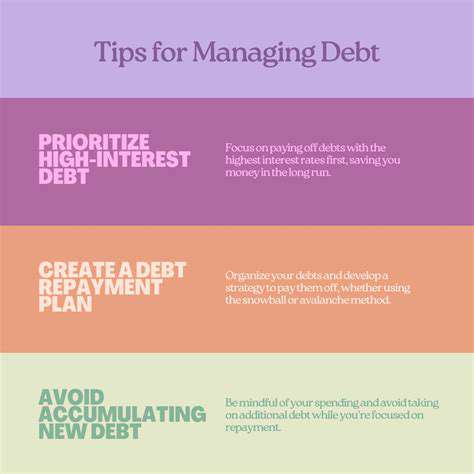

Prioritizing Your Debts

Not all debts are created equal. Some carry higher interest rates than others, and some debts have stricter repayment terms. Prioritizing debts based on interest rates, minimum payments, and potential penalties for late payments is crucial. Tackling high-interest debts first can significantly reduce the overall cost of borrowing over time. This often involves a combination of identifying the highest interest rate debts and those with the shortest repayment terms to maximize your savings.

Creating a Realistic Budget

After understanding your income and expenses, creating a realistic budget is paramount. This budget should incorporate your debt repayment plan and ensure that you're still able to meet your basic living expenses. It's crucial to allocate a specific portion of your income towards debt repayment, and this allocation should be sustainable and not jeopardize your ability to cover essential needs. This could involve allocating a certain percentage of your income to debt repayment or setting aside a specific amount each month.

Setting Realistic Repayment Goals

Establishing achievable repayment goals is vital for maintaining motivation and preventing feelings of overwhelm. Breaking down large debts into smaller, more manageable chunks can make the process less daunting. Consider setting short-term goals, like reducing a specific debt by a certain amount within a set timeframe. These short-term goals contribute to overall progress and provide a sense of accomplishment, driving you forward in your debt repayment journey.

Exploring Debt Consolidation Options

Exploring debt consolidation options can streamline your repayment process. Consolidating multiple debts into a single loan with a potentially lower interest rate can simplify payments and reduce the overall cost of borrowing. However, it's crucial to carefully compare different consolidation options to ensure you're choosing the most advantageous one for your financial situation. Thorough research and comparing interest rates, fees, and repayment terms are essential before making a decision.

Developing a Sustainable Payment Strategy

A sustainable payment strategy is crucial for long-term success in debt repayment. This strategy should involve finding ways to increase income or reduce expenses to allocate more funds towards debt repayment. Exploring ways to improve income, such as taking on a part-time job, freelancing, or selling unused items, can significantly accelerate the repayment process. In addition, identifying and eliminating unnecessary expenses can free up funds for debt reduction, making the repayment plan more effective.

Monitoring and Adjusting Your Plan

Regular monitoring and adjustments to your repayment plan are essential for staying on track. Periodically reviewing your progress, assessing your financial situation, and making necessary adjustments based on changing circumstances is crucial. This might involve increasing your repayment amounts if your income improves, or adjusting your spending habits if unexpected expenses arise. Flexibility and adaptability are key to a successful and sustainable debt repayment plan.

Read more about How to Manage Business Debt After a Downturn

![Best Budgeting Apps for 2025 [Top Picks]](/static/images/30/2025-05/AdvancedBudgetingAppswithInvestmentTools.jpg)

Hot Recommendations

- Tax Planning Tips for Homeowners [2025]

- How to Get Insurance for a Short Term Rental Property

- Understanding the Benefits of a Roth IRA

- How to Manage Business Debt After a Downturn

- How to Use a Barbell Investment Strategy

- Best Ways to Track Your Progress Towards Financial Freedom

- Tips for Managing Credit Card Rewards While Paying Off Balances

- Tax Planning Tips for Stock Options

- How to Plan for Retirement if You Didn't Save Early

- Guide to Managing Legal Debt