How to Create an Asset Allocation Plan

Taking Stock of Your Financial Reality

Mapping Your Income Landscape

When I first started tracking my finances, I discovered three unexpected income streams I'd completely overlooked. Documenting every dollar became my Sunday morning ritual - from my 9-to-5 paycheck to the occasional freelance gig and even garage sale profits. This granular approach revealed surprising patterns, like how my tutoring side hustle actually earned more per hour than my office job. I now keep a dedicated folder for pay stubs and bank statements, which has made tax season significantly less stressful.

The stability factor became crucial during the pandemic. My yoga instructor friend learned this the hard way when studio closures eliminated her primary income overnight. We worked together to diversify her revenue through online classes and YouTube tutorials. Building multiple income streams isn't just about earning more - it's about creating financial resilience.

The Expense Awareness Revolution

My wake-up call came when I realized I was spending $300 monthly on coffee and lunches - enough for a vacation fund! Categorizing expenses revealed these hidden budget leaks. Fixed costs like rent were easy, but the variables - those just this once purchases - added up alarmingly. Using a simple spreadsheet transformed my spending habits more than any app ever did. There's something powerful about manually entering each transaction that makes you think twice.

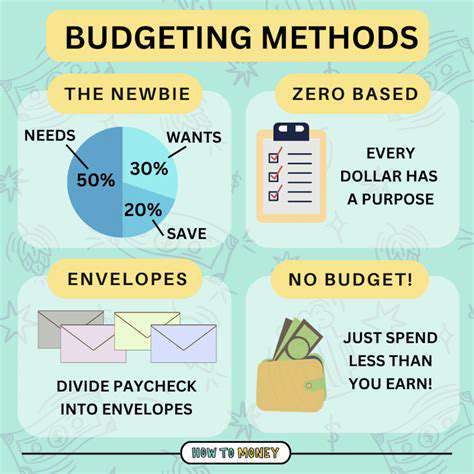

During my debt payoff journey, I discovered the 50/30/20 rule didn't fit my urban reality. My rent alone consumed 45% of my income. This realization led me to creative solutions - negotiating my lease, getting a roommate, and reallocating savings toward income-generating assets instead of just cutting back on lattes.

Conquering the Debt Mountain

Credit card statements used to give me anxiety until I created a debt dashboard. Seeing all balances, interest rates, and minimum payments in one place was terrifying but necessary. I tackled the 24% APR store card first, realizing it was costing me more than my grocery budget. The snowball method worked psychologically, but the avalanche method saved me thousands in interest.

My credit score journey from 580 to 750 taught me that errors are more common than people think. Finding an old medical collection on my report that wasn't mine took months to resolve. Now I check all three bureaus annually - it's like getting a financial physical.

Building Financial Resilience

Creating Your Personal Finance System

My first budget failed because it was too restrictive. The breakthrough came when I designed a system around my actual habits instead of ideal ones. Automating savings was the game-changer - paying myself first made the rest fall into place. I started with just $50 per paycheck, barely noticing the difference, and gradually increased it as raises came in.

The envelope system worked wonders for my discretionary spending. There's something psychological about using cash - watching those bills disappear makes you more mindful than swiping plastic. For bills, I switched to a dedicated checking account with automatic transfers matching my pay schedule.

The Power of Financial Check-Ins

Quarterly financial reviews became my secret weapon. I'd block off a Saturday morning, make coffee, and go through every account. These sessions revealed patterns I'd miss in daily tracking, like seasonal spending spikes or investment opportunities. Tracking net worth became motivating - even small progress felt like winning.

When I started investing, I made the classic mistake of checking my portfolio daily. Now I review investments monthly and rebalance quarterly. This prevents emotional decisions and keeps me focused on long-term goals. The 2008 crash taught my parents this lesson painfully - those who panicked and sold locked in losses, while those who held came out ahead.

When to Bring in the Pros

Navigating Life's Financial Crossroads

I resisted financial advisors until facing a complex decision about exercising stock options. The advisor's fee paid for itself in tax savings alone. Their perspective on estate planning revealed blind spots I didn't know I had. Now I view professional advice not as an expense but as an investment in avoiding costly mistakes.

The right advisor-client relationship makes all the difference. I interviewed three before finding one who spoke plainly without jargon and took time to understand my values, not just my numbers. We meet biannually unless major life events occur - this cadence keeps me accountable without creating dependency.

Continuous Financial Education

I allocate 1% of my income annually to financial education - books, courses, or seminars. This small investment compounds like interest, constantly improving my money management skills. Understanding the why behind financial advice prevents blindly following rules that might not fit my situation.

Joining a local investment club exposed me to perspectives I'd never encounter online. The retired teacher in our group approaches risk completely differently than the tech entrepreneur, and both views have shaped my strategy. Financial literacy isn't one-size-fits-all - it's about finding what works for your unique life circumstances.

Read more about How to Create an Asset Allocation Plan

![Best Health Insurance Plans for Families [2025]](/static/images/30/2025-05/EvaluatingCoverageandBenefits.jpg)

![How to Create a Monthly Budget That Works [2025 Guide]](/static/images/30/2025-05/ReviewingandRevisingYourBudgetRegularlyforLong-TermFinancialStability.jpg)

Hot Recommendations

- Budgeting for Travel: How to Save for Your Next Trip

- Guide to Understanding Retirement Account Rollovers

- Understanding Sector Rotation Strategy

- How to Choose Beneficiaries for Your Assets

- How to Combine Value and Growth Investing Strategies

- How to Use Stop Loss Orders When Investing

- How to Use Day Trading Strategy (High Risk)

- Understanding Investment Diversification

- How to Use a Core Satellite Investment Strategy

- Understanding Preferred Stocks