Best Budgeting Advice for Beginners

The Foundation: Why Tracking Matters

Consistent monitoring of cash flow forms the bedrock of sound financial health. Like a doctor checking vital signs, tracking reveals the pulse of your finances - showing exactly where money comes from and where it disappears. This visibility separates those who control their money from those controlled by it. Without this clarity, financial decisions become guesses rather than strategic moves.

Imagine trying to navigate a new city without a map. That's exactly what managing money without tracking feels like. Each recorded transaction acts as a landmark, helping you:

- Spot spending leaks (those daily coffees add up fast)

- Identify saving opportunities (hello, unused subscriptions)

- Prepare for seasonal expenses (holiday gifts, annual insurance)

Finding Your Tracking Style

Just as people have different learning styles, financial tracking methods vary. The key? Choosing what you'll actually use consistently. Your best option blends convenience with enough detail to be useful. Consider these approaches:

| Method | Best For | Considerations |

|---|---|---|

| Pen & Paper | Tech-averse users | Portable but lacks automation |

| Spreadsheets | Customization lovers | Steeper learning curve |

| Budgeting Apps | Automation seekers | Requires linking accounts |

I've seen clients succeed with all three - what matters most is finding your personal just right solution.

The Power of Categories

Grouping expenses transforms random numbers into actionable insights. Think of categories like financial folders - they help you:

- Spot patterns (I spend how much on takeout?)

- Compare months (Utilities were higher in January)

- Set realistic targets (Maybe $200 for dining out, not $50)

The magic happens when you review these categories quarterly. That's when most people discover their budget blindspots - expenses they didn't realize were draining their funds.

From Tracking to Action

Data alone doesn't change behavior - implementation does. Here's how to turn numbers into results:

Pro Tip: Start with one low-hanging fruit category each month. Cutting $50 from dining out feels easier than overhauling your entire budget at once.

Remember, financial progress resembles fitness - small, consistent changes create lasting results. What gets measured gets managed, and what gets managed improves over time.

Budgeting Without Burnout: Sustainable Strategies

Income Reality Check

Before planning expenses, understand your true income. Many people budget based on gross pay, then wonder why they're constantly short. Net income (after taxes/deductions) is your real spending power. For variable incomes:

- Calculate a 6-month average

- Budget based on the lowest recent month

- Save surplus months as a buffer

This conservative approach prevents the feast-or-famine cycle many freelancers experience.

Expense Hierarchy

Not all expenses deserve equal priority. Use this framework:

- Essentials: Housing, utilities, groceries

- Commitments: Loans, insurance

- Quality of Life: Entertainment, dining

- Future You: Savings, investments

This method ensures basics are covered before discretionary spending. Many find they actually have more flexibility than they realized when viewing expenses through this lens.

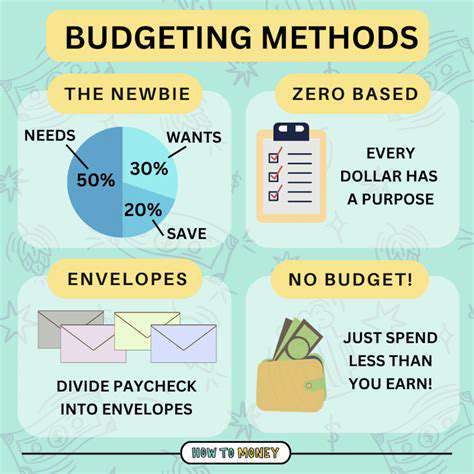

The 50/30/20 Alternative

For those overwhelmed by detailed tracking, consider this simplified approach:

| 50% Needs | Housing, utilities, transportation |

| 30% Wants | Dining out, entertainment |

| 20% Future | Savings, debt repayment |

While not perfect for everyone, this framework provides guardrails without micromanagement.

Goal Setting That Works

Effective financial goals share these characteristics:

- Visible: Written down where you'll see them

- Incremental: Broken into monthly targets

- Flexible: Adjustable as life changes

For example: Save $3,000 emergency fund in 12 months becomes $250/month. Miss a month? Spread the difference over remaining months.

Just as understanding pet behavior leads to better care, financial awareness enables better money decisions. Both require observation and adjustment.

The Living Budget: Making Adjustments Work For You

The Review Rhythm

Financial check-ins work best when they become habits. Try these approaches:

- Weekly: 5-minute transaction review

- Monthly: Category spending analysis

- Quarterly: Goal progress assessment

Consistency trumps perfection. Even imperfect tracking provides more insight than none at all.

Handling Financial Surprises

Unexpected expenses fall into two categories:

| Type | Examples | Strategy |

|---|---|---|

| Predictable Irregulars | Car maintenance, medical deductibles | Monthly sinking funds |

| True Emergencies | Job loss, major repairs | Dedicated emergency fund |

This distinction prevents surprises from derailing your budget. Most unexpected expenses are actually predictable with proper planning.

Income Variability Management

For those with fluctuating income, try the bucket system:

- Calculate baseline monthly needs

- Direct all income to a holding account

- Pay yourself the baseline amount weekly

- Distribute surplus to goals/savings monthly

This creates stability regardless of income timing.

The Flexibility Mindset

View your budget as a living document. Regular adjustments aren't failures - they're evidence you're paying attention. Common reasons to adjust:

- Life changes (new job, relocation)

- Goal progress (debt paid off)

- Spending habit shifts (less commuting)

Remember: A budget that doesn't adapt becomes obsolete. Your financial plan should evolve as you do.

Read more about Best Budgeting Advice for Beginners

![Best Debt Management Plans [2025 Review]](/static/images/30/2025-05/NavigatingtheApplicationProcessandOngoingManagement.jpg)

![Best Renters Insurance Companies [2025 Review]](/static/images/30/2025-05/CompanyB3AExcellentCustomerService26ClaimsHandling.jpg)

![Best Budgeting Software for Families [2025]](/static/images/30/2025-05/EvaluatingPopularBudgetingSoftwareOptionsforFamilies.jpg)

Hot Recommendations

- Tax Planning Tips for Homeowners [2025]

- How to Get Insurance for a Short Term Rental Property

- Understanding the Benefits of a Roth IRA

- How to Manage Business Debt After a Downturn

- How to Use a Barbell Investment Strategy

- Best Ways to Track Your Progress Towards Financial Freedom

- Tips for Managing Credit Card Rewards While Paying Off Balances

- Tax Planning Tips for Stock Options

- How to Plan for Retirement if You Didn't Save Early

- Guide to Managing Legal Debt