How to Deal with Payday Loan Debt

Negotiating with Your Lender (Where Applicable)

Understanding Lender Priorities

Negotiating with a lender effectively requires a deep understanding of their priorities. Lenders are primarily focused on minimizing risk and maximizing returns on their investment. This means they carefully scrutinize the borrower's financial stability, the value of the collateral, and the projected repayment capacity. Understanding these factors is crucial for crafting a negotiation strategy that addresses their concerns and positions you favorably.

A comprehensive understanding of the lender's perspective is essential for a successful negotiation. This includes considering their potential concerns about the market conditions, recent economic trends, and any specific risks associated with your loan application. Acknowledging and addressing these concerns proactively can significantly improve your chances of reaching a mutually beneficial agreement.

Strategies for Effective Negotiation

Developing a robust negotiation strategy involves preparing comprehensive documentation of your financial situation, including detailed income statements, recent tax returns, and any relevant financial projections. This allows the lender to assess your ability to repay the loan and understand your financial stability in the long term.

Thorough preparation is key to a successful negotiation. This includes knowing your desired terms, understanding the lender's potential counteroffers, and having a backup plan in case negotiations do not progress as anticipated. It also means having a clear understanding of your rights and responsibilities within the loan agreement.

Researching comparable loan terms offered by other lenders can provide valuable leverage during negotiations. Understanding the market rates and terms can help you identify potential areas for improvement in your current loan agreement.

Building a Strong Case for Negotiation

Successfully negotiating with your lender requires building a strong case that demonstrates your commitment to repayment and your understanding of the lender's concerns. Providing evidence of improved financial stability, such as increased income or reduced debt, can significantly strengthen your position and increase your chances of securing favorable terms.

A compelling argument for negotiation involves clearly outlining the reasons why the current terms are not suitable or how the proposed changes will benefit both parties. This could include demonstrating how a modified repayment schedule aligns with your current financial capabilities without jeopardizing the lender's interests.

Demonstrating a genuine understanding of the lender's risks and a proactive approach to mitigating them is crucial. This can include providing detailed financial projections, highlighting the value of the collateral, and outlining strategies to minimize any potential default risks.

Seeking Support and Resources

Understanding the Problem

Facing payday loan debt can be incredibly stressful, impacting various aspects of your life. It's essential to acknowledge the situation and understand the factors that contributed to accumulating this debt. Recognizing the root causes, such as unexpected expenses or insufficient budgeting, is the first step toward creating a sustainable plan for repayment and preventing future issues. Understanding the high-interest rates and short repayment terms associated with payday loans is also crucial, as these factors often exacerbate the problem.

Often, individuals find themselves in a cycle of borrowing, unable to meet the next payday without resorting to another loan. This cycle can become increasingly difficult to break, leading to mounting stress and financial instability. Addressing the underlying financial issues is critical to effectively managing and resolving the debt.

Identifying Available Resources

Fortunately, numerous resources are available to help individuals navigate payday loan debt. Local non-profit organizations often offer free or low-cost counseling and guidance on budgeting, debt management, and financial planning. These organizations can provide valuable support and connect individuals with further resources tailored to their specific needs.

Government agencies and consumer protection groups also provide information and assistance regarding payday loan regulations and consumer rights. Understanding your rights and the potential recourse available to you is an important part of the process. Online resources, financial websites, and community forums can also offer valuable insights and support networks.

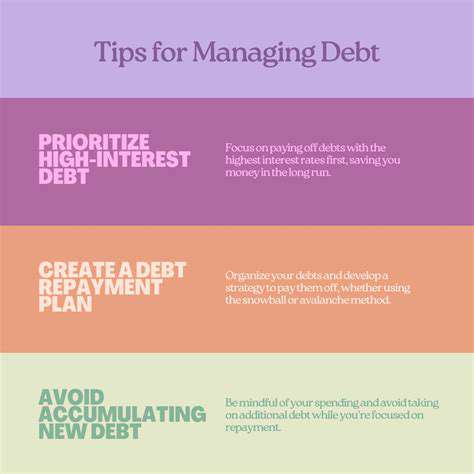

Creating a Repayment Strategy

Developing a realistic repayment plan is vital for managing payday loan debt effectively. This plan should include a detailed budget outlining all income and expenses, prioritizing essential needs and debt repayments. A realistic schedule for reducing the principal balance and paying interest charges should be incorporated.

Consider negotiating with the lender for a more manageable repayment schedule, if possible. Exploring options like debt consolidation or balance transfer programs might offer lower interest rates and a more affordable way to repay the debt. However, be cautious and thoroughly research any such program to avoid compounding the problem.

Seeking Professional Guidance

If the debt is overwhelming or you're struggling to develop a sustainable repayment plan, seeking professional guidance from a certified financial advisor or credit counselor is highly recommended. These professionals can provide personalized advice and develop a tailored strategy to address your specific situation.

They can help you understand your options, negotiate with creditors, and create a plan to resolve the debt while improving your overall financial health. Professional guidance can provide valuable support in navigating the complexities of payday loan debt and developing a sustainable financial future.

Read more about How to Deal with Payday Loan Debt

![Best Budgeting Apps for 2025 [Top Picks]](/static/images/30/2025-05/AdvancedBudgetingAppswithInvestmentTools.jpg)

![Best Investment Platforms for Beginners [2025]](/static/images/30/2025-05/AdditionalTipsforChoosingtheRightPlatform.jpg)

Hot Recommendations

- Understanding Fundamental Analysis in Investing

- Understanding Risk Management in Investing

- Guide to Rebalancing Your Portfolio

- Best Investment Strategies for Beginner Investors

- Best Budgeting Methods Compared

- How to Use Dollar Cost Averaging

- How to Budget When You Hate Budgeting

- Understanding the Efficient Market Hypothesis

- Guide to Retirement Planning for Business Owners

- How to Choose Insurance for a Classic Car