Tips for Improving Your Credit Utilization Ratio

Interpreting the Results

That 30% mark is like a financial finish line you want to stay behind. Cross it, and you might start seeing your credit score drop. Stay under it, and you're showing lenders you know how to handle credit responsibly.

Strategies for Reducing Utilization

If your ratio is too high, you've got options: pay down balances, spend less, or sometimes even close unused accounts (carefully). These moves are like financial push-ups that strengthen your credit health over time.

The Impact on Your Credit Score

A low CUR whispers to lenders that you're trustworthy with credit, which can mean better rates on everything from car loans to mortgages. A high ratio shouts that you might be stretching yourself too thin, potentially costing you thousands in higher interest over time.

Strategies for Lowering Your Credit Utilization Ratio

Understanding Credit Utilization

Your CUR is like a financial thermostat - set it too high and things get uncomfortable fast. Lenders use this number to gauge how risky it would be to lend you money. Keeping it at a comfortable level means you'll have more options when you need credit.

Monitoring Your Credit Card Balances

Watching your credit card balances is like keeping an eye on your speedometer - it helps you avoid going too fast (spending too much) and getting a ticket (hurting your credit score). Setting spending limits and sticking to them is the financial equivalent of cruise control.

Strategic Payment Strategies

Paying off high-interest debt first is like putting out the biggest fires before they spread. It saves you money on interest while also helping your CUR. Think of it as financial triage for your credit health.

Optimizing Spending Habits

Tracking where your money goes is like having GPS for your finances - it shows you where you might be taking wrong turns with your spending. A good budget is the roadmap that keeps you on the path to lower credit utilization.

Utilizing Credit Card Rewards Wisely

Credit card rewards can be tempting, but they're only helpful if they don't lead to higher balances. Using rewards to offset purchases you'd make anyway, then paying the balance in full, is like having your cake and eating it too - without the financial guilt.

Building an Emergency Fund

An emergency fund is like a financial airbag - it cushions the blow when unexpected expenses hit, so you don't have to rely on credit cards. Aim to save enough to cover several months of bills, and you'll protect both your CUR and your peace of mind.

Seeking Professional Guidance

Sometimes you need a financial coach - someone who can look at your unique situation and suggest personalized plays to improve your credit game. A good advisor can help you develop strategies that fit your life and goals.

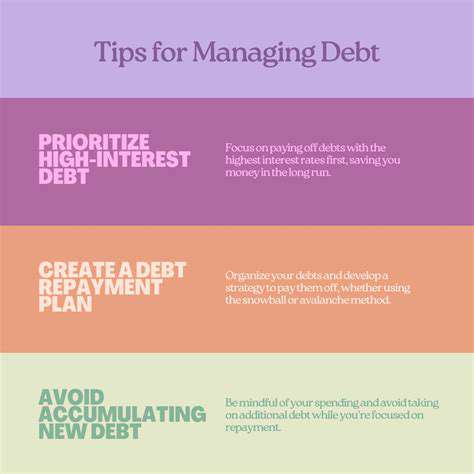

Pay Down Existing Debt Aggressively

Understanding the Impact of High Debt

Mounting debt doesn't just strain your budget - it weighs down your CUR like an anchor. High-interest debt in particular can grow faster than you can pay it off, creating a cycle that's hard to escape. Understanding this connection is the first step toward breaking free.

Strategies for Aggressive Debt Reduction

Attacking debt requires more than minimum payments - it needs a plan. Whether you choose to pay off small balances first (snowball method) or high-interest debts first (avalanche method), the key is consistency. Think of it like training for a marathon - small, regular efforts lead to big results over time.

Exploring Debt Consolidation and Balance Transfers

Combining debts or moving them to lower-interest cards can be smart moves, but they're not magic wands. You still need discipline to pay down the balance. These strategies are like financial pit stops - they can help you refuel and get back on track, but you still have to drive the car.

Creating a Sustainable Debt Repayment Plan

A good repayment plan isn't just about today's debt - it's about building habits that prevent future debt. This means creating a budget that works for your life, setting realistic goals, and tracking your progress. It's financial fitness for the long haul.

Increase Your Credit Limit

Understanding Credit Limits

Your credit limit is like a financial trust meter - the higher it goes, the more lenders believe in your ability to handle credit responsibly. But with great power comes great responsibility - a higher limit only helps if you don't use it as an excuse to spend more.

Strategies for Increasing Your Credit Limit

Proving you're creditworthy takes time and consistency. Paying on time, keeping balances low, and using credit regularly (but responsibly) shows lenders you're ready for more. Sometimes all it takes is asking - many card issuers will consider increases if you've been a good customer.

Credit Building Activities

Building credit is like building muscle - it takes the right kind of exercise. Using different types of credit responsibly, keeping old accounts open, and checking your credit report for errors are all ways to strengthen your credit profile over time.

The Importance of Responsible Credit Use

A higher credit limit only helps your CUR if you don't fill it up. It's like having a bigger gas tank - it gives you more range, but you still need to watch your fuel gauge (spending) to avoid running out of money before payday.

Manage Your Spending Habits

Understanding Your Spending Habits

Tracking where your money goes is like financial mindfulness - it makes you aware of patterns you might not notice otherwise. Small daily expenses can add up to big credit card balances, so knowing where your money disappears to is half the battle.

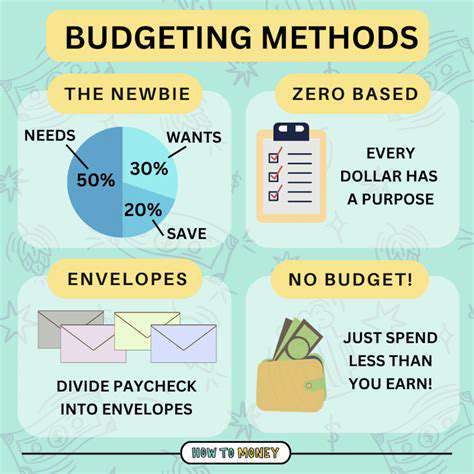

Setting Realistic Budget Goals

A good budget isn't about deprivation - it's about making sure your money goes where it matters most to you. Start with small changes that don't feel painful, and build from there. Financial success is more marathon than sprint.

Utilizing Budgeting Tools and Apps

Modern budgeting tools are like having a financial assistant in your pocket. They can categorize spending, spot trends, and even nudge you when you're overspending. The right tool can turn budgeting from a chore into something almost... enjoyable?

Prioritizing Needs Over Wants

Separating needs from wants is like financial triage - it ensures the most important things get taken care of first. This doesn't mean never spending on fun things, just being intentional about when and how you do.

Creating a Debt Repayment Plan

High credit card balances don't just hurt your CUR - they cost you money in interest. A solid repayment plan turns those interest payments into savings, giving you more money to put toward your goals instead of your creditors.

Tracking and Reviewing Your Progress

Regular financial check-ups are like stepping on the scale when you're trying to lose weight - they keep you honest and motivated. Celebrate small wins (like paying off a card) to stay encouraged on the journey to better credit health.

Read more about Tips for Improving Your Credit Utilization Ratio

![Best Tools for Debt Management [2025]](/static/images/30/2025-05/DebtManagementPlans28DMPs293APersonalizedStrategiesforRepayment.jpg)

![How to Pay Off Credit Card Debt Fast [Proven Strategies]](/static/images/30/2025-05/StayMotivatedandConsistent3AKeytoLong-TermSuccess.jpg)

![How to Create a Monthly Budget That Works [2025 Guide]](/static/images/30/2025-05/ReviewingandRevisingYourBudgetRegularlyforLong-TermFinancialStability.jpg)