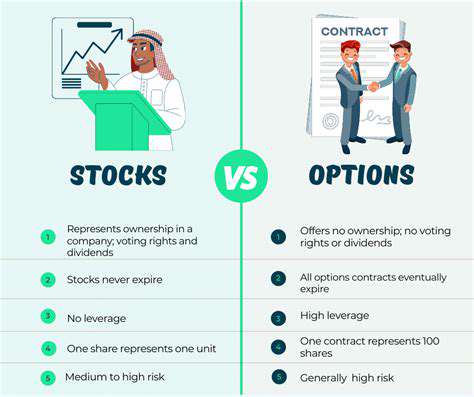

Understanding Options Trading (For Beginners)

Types of Options

Options diversify across underlying assets including stocks, ETFs, futures, and indices. Each asset class carries distinct pricing models and risk profiles. Market dynamics vary significantly between volatile tech stocks and stable blue-chip equities, for instance. Expiration timelines further segment options, ranging from weekly to multi-month durations.

Asset-specific knowledge becomes paramount when trading options. The pricing structure for an option on a cryptocurrency ETF differs radically from one tied to utility stocks, demanding tailored analytical approaches.

Option Pricing and Valuation

Multiple variables influence option pricing: underlying asset price, strike price, time remaining until expiration, and implied volatility - the market's forecast of future price turbulence. These elements interact in complex ways that necessitate thorough examination for strategic trading.

While models like Black-Scholes attempt to quantify these relationships, recognizing their limitations and potential market anomalies proves equally crucial. Effective application requires deep comprehension of both mathematical frameworks and their underlying assumptions.

Option Strategies

The strategic spectrum ranges from basic covered calls to advanced straddle/strangle approaches. Each methodology presents distinct risk-reward profiles requiring meticulous evaluation. Strategic mastery separates successful traders from speculative gamblers in this high-stakes environment.

Risk Management in Options Trading

Options inherently involve risk magnification. Their leveraged nature means minor underlying asset movements can trigger disproportionate gains or losses. Implementing disciplined position sizing and stop-loss protocols becomes essential for capital preservation.

Personal risk tolerance assessment forms the foundation of sustainable trading. This isn't lottery-ticket speculation - it demands patience, systematic planning, and clear loss thresholds aligned with financial objectives.

Leverage and Potential Rewards

Options provide exceptional leverage compared to traditional investments, amplifying both upside potential and downside exposure. This dual-edged characteristic necessitates rigorous risk assessment before position entry. Strategic alignment with personal risk parameters enables reward optimization while containing potential damage.

Leverage mechanics comprehension serves as the compass for navigating options markets successfully. This knowledge facilitates strategy development congruent with individual financial aspirations and risk appetite.

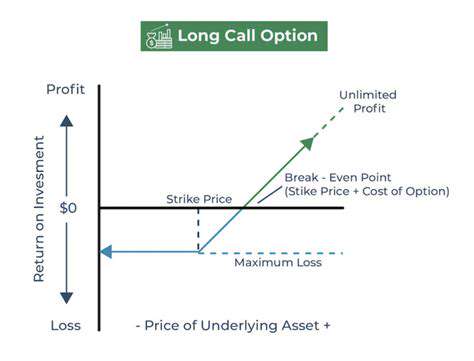

Call Options: Betting on Price Increases

Understanding Call Options

Call options confer purchase rights at predetermined strike prices before expiration dates, effectively positioning for bullish scenarios. The asymmetric risk profile - limited downside (premium) versus unlimited upside - makes calls particularly attractive for confident upside bets.

Strike Price and Expiration Date

Strike price selection should mirror market outlook precision. Anticipating moderate gains suggests near-current strikes, while aggressive forecasts might justify deeper out-of-money positions. Expiration timing balances opportunity windows against time decay - shorter terms suit volatile momentum plays, while longer durations accommodate gradual thesis realization.

Premium and Intrinsic Value

Option premiums reflect complex market consensus incorporating multiple variables. Intrinsic value - the immediate exercisable profit - serves as the bedrock valuation metric when assessing option attractiveness. This tangible value component anchors pricing analysis amidst more speculative time value considerations.

Leverage and Risk Management

Call options magnify capital efficiency dramatically, enabling substantial notional exposure with limited upfront capital. This leverage demands corresponding vigilance - disciplined stop-loss implementation and position sizing prevent manageable losses from becoming catastrophic.

Profit and Loss Potential

Theoretical profit ceilings remain unlimited as underlying assets could appreciate indefinitely. This potential must be balanced against the reality that most options expire worthless, making selective, high-conviction positions preferable to speculative scattering.

Trading Strategies and Considerations

From conservative covered calls to aggressive naked positions, strategy selection should align with both market outlook and personal risk tolerance. Successful implementation requires moving beyond theoretical understanding to practical execution nuances - fill dynamics, liquidity considerations, and position monitoring protocols.

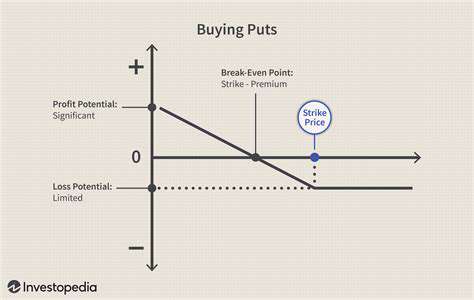

Put Options: Betting on Price Decreases

Understanding Put Options

Put options provide strategic downside exposure, allowing asset sales at predetermined prices regardless of market declines. This bearish positioning tool proves invaluable during market corrections or company-specific challenges.

Identifying Potential Price Declines

Effective put trading begins with rigorous fundamental and technical analysis. Catalyst identification - earnings reports, macroeconomic shifts, or sector rotations - separates informed bets from blind speculation. This analytical groundwork informs strike and expiration selection.

Determining the Strike Price

Strike positioning balances probability and payoff. Moderate bearishness might suggest slightly out-of-money strikes, while strongly negative outlooks could justify deeper in-the-money positions despite higher premiums.

Assessing Expiration Dates

Time horizon selection reflects expected catalyst timing. Event-driven trades demand precise expiration alignment, while macroeconomic positions benefit from longer timeframes accommodating gradual thesis development.

Calculating Potential Profit and Loss

Maximum profit occurs if the underlying asset becomes worthless - an extreme scenario. More realistically, profit potential caps at strike price minus market price at exercise. The premium paid represents the maximum possible loss, creating defined-risk scenarios.

Managing Risk in Put Option Strategies

While risk is theoretically limited, practical portfolio management remains essential. Position concentration limits and ongoing thesis validation prevent overexposure to single ideas. Regular position review ensures alignment with evolving market conditions.

Comparing Put Options to Other Investment Strategies

Relative to short selling, puts offer cleaner risk profiles without margin calls or unlimited loss potential. This structural advantage makes puts preferable for most retail investors implementing bearish strategies, despite premium costs.

Authentic rustic design captures organic warmth through natural wood imperfections that evoke wilderness retreats and artisanal craftsmanship. True character emerges in unforced textures - grain variations become art, tool marks whisper of human touch. The interplay of light across these surfaces creates dynamic spaces that evolve throughout the day.

Key Concepts in Options Trading

Intrinsic Value

Intrinsic value represents an option's tangible worth, calculated as the differential between underlying asset price and strike price. This concrete metric anchors valuation analysis. Options with substantial intrinsic value behave more like their underlying assets, while those relying on time value exhibit different characteristics.

Time Value

This premium component reflects the potential for future intrinsic value growth. Time decay accelerates as expiration approaches, creating non-linear erosion patterns that strategic traders exploit. Mastering theta dynamics enables premium harvesting strategies while avoiding value traps.

Volatility

As the market's uncertainty gauge, volatility dramatically impacts option pricing. Historical volatility measures past fluctuations, while implied volatility reflects future expectations. Skilled traders recognize when implied volatility diverges from likely outcomes, creating mispricing opportunities.

Read more about Understanding Options Trading (For Beginners)

![Best Life Insurance Policies [2025 Review]](/static/images/30/2025-05/AssessingPermanentLifeInsuranceOptions.jpg)

![Best Car Insurance Companies in 2025 [Review]](/static/images/30/2025-05/CustomerServiceandClaimsHandling3AACrucialAspect.jpg)

![Creating a Zero Based Budget [Beginner's Guide]](/static/images/30/2025-06/MaintainingYourZero-BasedBudget3ATipsforLong-TermSuccess.jpg)