Best Investment Strategies for Income Focused Investors

Understanding Yield-Oriented Strategies

Investors who prioritize income generation over capital appreciation often turn to yield-oriented strategies. These approaches focus on securities that consistently pay dividends or interest, creating a reliable income stream. This method is particularly appealing to retirees or those who depend on regular payouts rather than waiting for price appreciation. Grasping the relationship between yield and risk is essential for effectively implementing these strategies.

Evaluating Dividend Stocks

When assessing dividend stocks, it's critical to examine the company's financial stability and dividend track record. A steady dividend payout often indicates a robust financial position. However, investors should look beyond the dividend yield alone, considering the company's overall performance, industry trends, and potential risks. A high yield might sometimes signal underlying financial troubles that could threaten future dividend payments.

Bond Investing for Income

Bonds play a vital role in yield-oriented strategies by providing fixed income through regular interest payments. Corporate and government bonds vary in risk and return, making it essential to research credit ratings and maturity dates. This careful analysis helps balance returns with risk mitigation.

Exploring Preferred Stocks

Preferred stocks offer a unique blend of fixed dividends and lower risk compared to common stocks. These securities typically yield higher dividends, but investors must understand how interest rate changes can affect their value. Thorough research into preferred stock valuation is key to making informed decisions.

Analyzing Income Funds and ETFs

Income funds and ETFs simplify diversification by pooling investments into dividend-paying stocks or bonds. These options often reduce transaction costs, but investors should scrutinize historical performance and expense ratios to ensure they align with their goals.

Managing Risk in Yield-Oriented Portfolios

While yield-oriented strategies focus on income, risk management remains crucial. Diversification across asset classes helps cushion against market downturns. Understanding how economic shifts and interest rate changes impact different securities is vital for long-term portfolio resilience.

The Power of Passive Income: Exploring Dividend Stocks and REITs

Understanding Dividend Stocks

Dividend stocks form the backbone of passive income strategies. These companies share profits with shareholders through regular dividends, offering a steady cash flow. Researching a company's financial health and dividend history is essential to ensure sustainable payouts. Investors should also distinguish between regular, special, and variable dividends, as each type affects strategy differently.

The Appeal of Real Estate Investment Trusts (REITs)

REITs provide passive income by investing in income-generating real estate like apartments or malls. By law, REITs must distribute most of their income as dividends, making them attractive for real estate exposure without direct ownership. However, they're sensitive to economic changes, so sector-specific research is crucial.

Analyzing Dividend Growth and Consistency

Companies with a history of increasing dividends often demonstrate financial strength. Tracking dividend growth patterns helps identify reliable income sources, while sudden cuts may signal trouble. This analysis is key to building a sustainable passive income stream.

Evaluating REIT Performance and Sector Diversification

REIT performance varies by sector—residential, commercial, or industrial. Spreading investments across sectors can reduce risk since each reacts differently to economic conditions. Staying informed about market trends helps make better investment choices.

Diversification and Risk Management in Passive Income Strategies

Diversifying across dividend stocks and REITs minimizes reliance on any single investment, creating a more stable income flow. Understanding each asset's unique risks ensures a balanced approach to passive income generation.

Strategic Bond Investing for Steady Income

Understanding the Fundamentals of Bond Investing

Bonds offer predictable income by lending to corporations or governments. Key factors like maturity dates and credit ratings influence risk and returns. High-yield bonds promise greater returns but carry default risks, while government bonds are safer but offer modest yields. Matching bond types to your risk tolerance is essential.

Strategies for Maximizing Income Potential

Building a diversified bond portfolio with varying maturities helps manage interest rate risks. Bond ladders—purchasing bonds with staggered maturity dates—ensure consistent income. Staying updated on market trends allows for timely adjustments to your strategy.

Managing Bond Portfolio Risk and Considerations

Bonds face risks like rising interest rates and inflation. Tax implications vary by bond type, so consulting a financial advisor can optimize tax efficiency. Regular portfolio reviews and rebalancing maintain alignment with long-term goals.

Long-Term Perspective and Portfolio Rebalancing: Ensuring Sustainability

Long-Term Investment Strategies

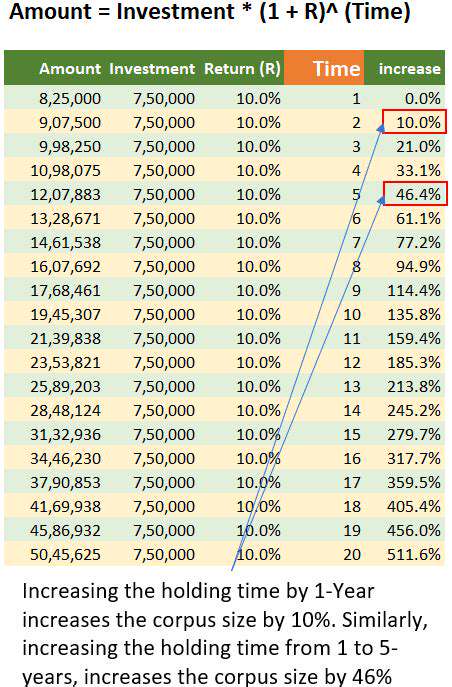

Long-term investing requires patience and a focus on compounding returns. Starting early and staying invested magnifies growth over decades. Avoid reacting to short-term market swings; instead, stick to a diversified plan aligned with your financial objectives.

Portfolio Diversification

Spreading investments across stocks, bonds, and real estate reduces vulnerability to any single asset's performance. Geographic and sector diversification further smooths volatility, creating more stable long-term returns.

Risk Tolerance and Financial Goals

Your comfort with risk should guide asset allocation. Clear financial goals—like retirement or education funding—help shape appropriate investment horizons. Regularly reassessing these goals ensures your strategy remains relevant.

Monitoring and Rebalancing

Periodic portfolio reviews catch drifts from target allocations. Rebalancing restores your desired risk level and keeps goals on track. Professional advice can be valuable when adjusting complex portfolios.

Read more about Best Investment Strategies for Income Focused Investors

![Best Life Insurance Policies [2025 Review]](/static/images/30/2025-05/AssessingPermanentLifeInsuranceOptions.jpg)

![Best Homeowners Insurance Companies [2025 Review]](/static/images/30/2025-05/TopTierHomeownersInsuranceProvidersin2025.jpg)

![Best Tools for Debt Management [2025]](/static/images/30/2025-05/DebtManagementPlans28DMPs293APersonalizedStrategiesforRepayment.jpg)

Hot Recommendations

- Tax Planning Tips for Homeowners [2025]

- How to Get Insurance for a Short Term Rental Property

- Understanding the Benefits of a Roth IRA

- How to Manage Business Debt After a Downturn

- How to Use a Barbell Investment Strategy

- Best Ways to Track Your Progress Towards Financial Freedom

- Tips for Managing Credit Card Rewards While Paying Off Balances

- Tax Planning Tips for Stock Options

- How to Plan for Retirement if You Didn't Save Early

- Guide to Managing Legal Debt