Understanding How Investment Fees Eat Your Returns

Beyond the Basic: Exploring Hidden Costs

While brokerage fees grab most investors' attention, savvy market participants know to look deeper. These often-overlooked expenses can quietly chip away at your portfolio's growth year after year. Failing to account for these costs is like driving with your eyes closed - you might stay on the road for a while, but eventually you'll crash. Take platform fees, for instance; what seems like minor charges for inactivity or account maintenance can snowball into substantial sums over decades.

Investment products themselves carry their own cost burdens. Those seemingly efficient ETFs or mutual funds often come with expense ratios that function like termites in your financial foundation, slowly but surely weakening your returns. A comprehensive analysis of these costs should be as routine as checking a stock's P/E ratio before investing.

The Impact of Trading Volume and Frequency

Your trading habits directly affect your bottom line. While active traders might enjoy the thrill of frequent transactions, each trade comes with its own price tag. High-volume traders often discover too late how these nickel-and-dime charges add up to serious money. It's worth asking whether all that activity actually improves returns or just lines your broker's pockets.

Slippage represents another hidden cost many traders underestimate. For those moving large positions, even small price discrepancies can translate to significant dollars left on the table. These execution variances should factor into every serious investor's cost-benefit analysis.

Investment Platform Features and Services

Modern platforms tempt users with shiny tools and services, from advanced analytics to personalized portfolio management. The critical question isn't whether these features are nice to have, but whether they genuinely enhance returns enough to justify their cost. Like a restaurant's wine list, the markup on these services often exceeds their actual value.

Premium research and sophisticated charting tools might look impressive, but investors should approach these add-ons with the same skepticism as a used car salesman's promises. Conducting a thorough cost-benefit analysis of platform features could save thousands over an investment lifetime.

Tax Implications and Reporting

Taxes represent perhaps the most predictable yet overlooked investment cost. While some platforms offer tax assistance, these services frequently come with their own fees. Smart investors treat tax planning not as an annual chore but as a year-round strategy, because every dollar saved in taxes is a dollar that keeps working for you.

Different investments trigger different tax consequences. Consulting a qualified tax professional isn't an expense - it's an investment in avoiding much larger costs down the road. Proper tax management can mean the difference between a comfortable retirement and scrambling to make ends meet.

The Power of Compounding: How Small Fees Multiply Over Time

The Fundamental Concept

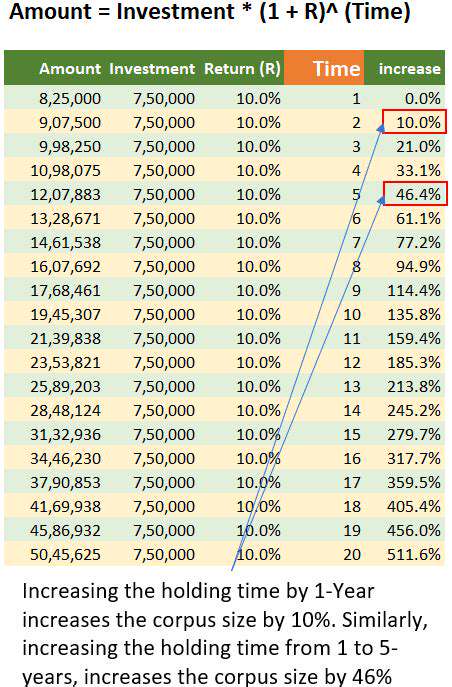

Compounding works like a financial snowball, growing not just from your initial investment but from the accumulated returns themselves. Picture planting an acorn that grows into an oak, which then produces more acorns that become more oaks. This exponential growth transforms modest, regular investments into substantial wealth given enough time and patience. The key lies in starting early and staying consistent, allowing time to work its mathematical magic.

The mechanism is elegantly simple: returns generate more returns, which in turn generate even more. This virtuous cycle demonstrates why time in the market consistently beats timing the market. Those who understand and harness this principle gain a powerful advantage in wealth building.

The Time Value of Money

Money today holds more potential than money tomorrow because of its earning capacity. This fundamental truth explains why financial advisors stress early investing - the additional years allow compounding to work its full magic. The difference between starting at 25 versus 35 could mean hundreds of thousands of dollars by retirement.

Strategies for Maximizing Compounding

Consistency proves more powerful than amount when harnessing compounding. Regular investments, even small ones, create a rhythm that builds wealth almost imperceptibly at first, then dramatically over decades. Starting young provides the greatest advantage, giving investments maximum time to grow.

Diversification serves as compounding's perfect partner, spreading risk while allowing multiple investments to grow simultaneously. A balanced portfolio across asset classes provides stability while still capturing growth opportunities. The combination of diversification and compounding creates a resilient wealth-building strategy.

Long-Term Benefits and Implications

The long game reveals compounding's true power. What seems insignificant in year five becomes transformative by year twenty-five. This patient approach can fund education, retirement, or generational wealth, providing options and security unavailable to those seeking quick returns.

Understanding compounding changes one's entire financial perspective. It transforms saving from deprivation to empowerment, where each dollar becomes a worker building future freedom. This mindset shift may be compounding's most valuable benefit of all.

Strategies to Minimize Fee Erosion: Active Management vs. Passive Investing

Active Management Strategies for Fee Erosion Mitigation

Active managers promise outperformance but deliver higher fees with no guarantees. Investors considering this route should examine track records with a forensic accountant's scrutiny. Past performance offers clues, but the harsh reality is that most active managers fail to consistently beat their benchmarks after fees. Those who choose active management should view it as paying for potential, not performance.

Alignment between investment goals and manager strategy proves crucial. Even the most skilled active manager becomes a poor fit if their approach contradicts your risk tolerance or objectives. Periodic performance reviews help determine whether the premium paid for active management continues to justify itself.

Passive Investing and Fee Erosion Control

Passive strategies shine in their simplicity and cost-efficiency. By mirroring market indexes, they eliminate the guessing game of stock picking while keeping fees minimal. This straightforward approach removes multiple layers of costs that typically erode returns in active strategies. For most investors, passive investing represents the most reliable path to capturing market returns.

The predictability of passive investments allows for clearer long-term planning. Without the volatility of manager decisions or style drift, investors can focus on asset allocation rather than fund selection. This consistency proves particularly valuable during market turbulence when emotional decisions often prove costly.

Comparing Active and Passive Management Fees

The fee comparison between active and passive strategies often reveals startling differences. While active funds might charge 1% or more, quality index funds frequently cost less than 0.10%. This 0.90% difference compounds into massive sums over an investing lifetime. Investors should ask what exceptional value active managers provide to justify this premium.

Historical data consistently shows passive strategies outperforming most active ones over the long term, especially after fees. This evidence challenges the traditional assumption that higher fees buy better performance. In investing as in life, you don't always get what you pay for.

Diversification and Fee Erosion

Proper diversification acts as a natural fee mitigator. By spreading investments across asset classes, sectors, and geographies, investors reduce reliance on any single expensive strategy. This approach creates a natural balance where low-cost investments can offset the impact of higher-cost ones, resulting in an efficient overall portfolio.

Monitoring and Adjusting Investment Strategies

Regular portfolio reviews serve as preventive medicine against fee creep. As investment needs evolve, previously suitable products may become unnecessarily expensive. An annual fee audit helps identify and eliminate redundant or underperforming expensive holdings. This maintenance keeps your portfolio running efficiently.

Rebalancing provides another opportunity to evaluate costs. As market movements alter allocations, the rebalancing process allows for cost optimization alongside risk management. This dual benefit makes regular portfolio reviews essential for fee-conscious investors.

Long-Term Perspective and Fee Erosion

Viewing fees through a long-term lens reveals their true impact. What seems negligible annually becomes substantial over decades. Adopting a marathon mentality helps investors see fee reduction not as penny-pinching but as compound interest working in reverse. Each dollar saved in fees remains invested, continuing to grow.

This long view also puts short-term performance in proper perspective. Market fluctuations matter less than consistent, low-cost participation in market growth. By focusing on the horizon rather than the waves, investors position themselves for sustainable success.

Read more about Understanding How Investment Fees Eat Your Returns

![How to Build an Emergency Fund [Step by Step]](/static/images/30/2025-04/Step53AReplenishYourEmergencyFundWhenNecessary.jpg)

![Best Homeowners Insurance Companies [2025 Review]](/static/images/30/2025-05/TopTierHomeownersInsuranceProvidersin2025.jpg)

![Best Tools for Debt Management [2025]](/static/images/30/2025-05/DebtManagementPlans28DMPs293APersonalizedStrategiesforRepayment.jpg)

Hot Recommendations

- Tax Planning Tips for Homeowners [2025]

- How to Get Insurance for a Short Term Rental Property

- Understanding the Benefits of a Roth IRA

- How to Manage Business Debt After a Downturn

- How to Use a Barbell Investment Strategy

- Best Ways to Track Your Progress Towards Financial Freedom

- Tips for Managing Credit Card Rewards While Paying Off Balances

- Tax Planning Tips for Stock Options

- How to Plan for Retirement if You Didn't Save Early

- Guide to Managing Legal Debt