Best Life Insurance Policies [2025 Review]

Types of Life Insurance Policies Available

Term Life Insurance

When considering life insurance options, term life insurance stands out for its straightforward approach. These policies provide coverage for a predetermined timeframe, usually between 10 and 30 years. What makes term life particularly appealing is its affordability, especially for younger individuals in good health. The guaranteed death benefit during the active term offers peace of mind, ensuring financial security for beneficiaries should the unexpected occur.

One crucial detail often overlooked involves the premium structure. While initial costs are attractive, policyholders should anticipate potential increases as they age or when renewing coverage. This aspect underscores why thorough evaluation of future financial commitments is essential before committing to a term life policy. Budget-conscious individuals must weigh these factors carefully against their long-term financial plans.

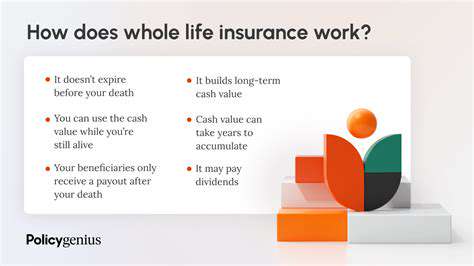

Whole Life Insurance

For those seeking lifelong protection, whole life insurance serves as a permanent solution. The defining characteristic is its guaranteed coverage that remains active throughout the insured's lifetime, coupled with a death benefit that never expires. Beyond basic protection, these policies develop a cash value component that grows steadily over time.

This cash accumulation functions similarly to a savings vehicle, with growth influenced by the insurer's investment strategies. Policyholders gain access to potential tax advantages and the flexibility to borrow against this accumulated value when needed. However, these benefits come at a cost, with premium payments typically exceeding those of term policies and maintaining consistency throughout the policy duration.

Universal Life Insurance

Universal life insurance introduces valuable flexibility into permanent coverage. Policyholders enjoy adjustable premium payments and death benefit amounts that can adapt to changing financial situations. This dynamic feature proves particularly useful during periods of income fluctuation or shifting financial priorities. The cash value component offers investment opportunities, potentially yielding greater returns than traditional whole life policies.

However, the investment aspect carries inherent variability that requires careful consideration. Since returns aren't guaranteed, policyholders must maintain realistic expectations and understand the potential for fluctuation in their policy's performance.

Variable Life Insurance

Variable life insurance merges permanent coverage with investment opportunities. The standout feature involves directing the cash value into various market-based investment options, creating potential for significant growth. This approach differs markedly from traditional whole life policies with their more conservative investment strategies.

With greater potential rewards comes increased risk exposure. Policyholders must acknowledge the possibility of investment losses that could diminish the policy's overall value. Thorough understanding of the available investment options and their associated risks becomes crucial before selecting this type of coverage.

Variable Universal Life Insurance

Combining the best features of variable and universal policies, variable universal life insurance offers comprehensive flexibility. Policyholders benefit from adjustable premiums and death benefits while accessing market-linked investment options for their cash value. This combination provides unparalleled control over the policy's financial aspects, allowing for strategic adjustments as circumstances change.

The investment component, while offering growth potential, requires careful management. Prospective buyers should thoroughly evaluate their risk tolerance and investment knowledge before committing to this sophisticated financial product.

Read more about Best Life Insurance Policies [2025 Review]

Hot Recommendations

- Tax Planning Tips for Homeowners [2025]

- How to Get Insurance for a Short Term Rental Property

- Understanding the Benefits of a Roth IRA

- How to Manage Business Debt After a Downturn

- How to Use a Barbell Investment Strategy

- Best Ways to Track Your Progress Towards Financial Freedom

- Tips for Managing Credit Card Rewards While Paying Off Balances

- Tax Planning Tips for Stock Options

- How to Plan for Retirement if You Didn't Save Early

- Guide to Managing Legal Debt