How to Save for Retirement While Paying Off Debt

Assessing Your Financial Landscape

Understanding Your Income Sources

A crucial first step in assessing your financial landscape is understanding your income streams. This involves not only your primary salary but also any additional sources, such as investments, side hustles, or rental income. Carefully documenting each income source, including its frequency and predictability, is vital for accurate budgeting and financial planning.

Analyzing your income patterns can help you identify potential gaps or surpluses in your budget. This information is essential for making informed decisions about saving, investing, and spending. Consider how consistent each income source is and the potential for fluctuations, as this can affect your overall financial stability.

Evaluating Your Expenses

Detailed expense tracking is paramount to comprehending your financial situation. This encompasses everything from housing and utilities to groceries, transportation, entertainment, and debt repayments. Categorizing expenses into essential and discretionary categories provides valuable insight into spending habits and potential areas for cost reduction.

Understanding where your money goes is just as important as knowing where it comes from. By meticulously tracking your expenses, you can pinpoint areas where you may be overspending and identify opportunities to save money. Regular review of these expenses is critical for maintaining financial health.

Analyzing Your Debt Situation

Evaluating your debt load is a critical component of assessing your financial landscape. This involves understanding the types of debt you have (e.g., credit card debt, student loans, mortgages) and the interest rates associated with each. Analyzing your debt repayment schedule is vital for creating a realistic debt reduction strategy.

A high level of debt can significantly impact your financial well-being. Understanding the terms of your loans and developing a plan to manage and reduce your debt is essential for achieving financial freedom. A proactive approach to debt management can free up valuable resources for other financial goals.

Assessing Your Savings and Investments

A comprehensive financial assessment must include a thorough review of your savings and investment accounts. This includes examining the amount of money you have saved, the types of savings accounts you have, and the returns you are earning on your investments. This will help you determine if your savings are sufficient for your short-term and long-term financial goals.

Evaluating your investment portfolio is essential for understanding your risk tolerance and potential for returns. This includes the types of investments you have, their potential for growth, and their risk levels. This step is essential for ensuring your investments align with your long-term financial goals.

Evaluating Your Assets

Beyond your savings and investments, your assets encompass tangible items like property, vehicles, and valuable personal possessions. Appraising the value of these assets is important for understanding your overall net worth and potential financial resources.

A thorough understanding of your assets is crucial for planning for future financial needs and opportunities. This knowledge can be used to develop strategies for maximizing the value of these assets and ensuring they contribute to your overall financial well-being. It will also help you determine your future financial security.

Identifying Your Financial Goals

Defining your short-term and long-term financial objectives is a fundamental part of assessing your financial landscape. This involves creating a clear vision of where you want to be financially in the future, considering factors like retirement planning, homeownership, or education funding.

Setting realistic and measurable financial goals is essential for motivation and progress. This helps to create a roadmap for achieving your desired financial outcome. A clearly defined goal gives a sense of direction and purpose in your financial journey.

Understanding Your Risk Tolerance

A critical aspect of assessing your financial landscape is understanding your comfort level with financial risk. This involves honestly evaluating your willingness to take on risk in investments and your ability to withstand potential losses. Assessing your risk tolerance helps you to create a portfolio that aligns with your personality and comfort level.

Recognizing your risk tolerance is essential for making informed investment decisions. A well-defined risk tolerance guides your approach to investing, allowing you to create a portfolio that balances your desire for growth with your aversion to risk. This will ensure your finances are handled in the most appropriate way.

Creating a Realistic Retirement Savings Plan

Understanding Your Retirement Needs

A realistic retirement savings plan starts with a clear understanding of your future needs. This involves more than just estimating how much you'll need to cover your living expenses; it also includes considering potential healthcare costs, inflation, and potential changes in lifestyle. Thorough research and projections are essential to create a plan that aligns with your long-term goals and financial realities. A crucial aspect of this phase is recognizing that retirement isn't a singular event but a period of extended financial responsibility. Therefore, a comprehensive assessment of your current financial situation is paramount before you begin to formulate your savings strategy.

Considering the rising cost of healthcare is essential. Medical expenses can significantly impact your retirement funds. Predicting future healthcare costs and factoring them into your retirement savings plan is crucial to avoid depleting your savings prematurely. This requires careful research and potentially consulting with financial advisors to get a realistic estimate of the potential costs you might face throughout your retirement.

Establishing a Realistic Savings Goal

Once you've assessed your needs, you can set a realistic savings goal. This involves determining the amount of money you need to accumulate to sustain your desired lifestyle during retirement. Consider various scenarios, including potential inflation and unexpected expenses. A crucial aspect of this stage is to avoid getting discouraged by the seemingly large sum needed. Break down the goal into smaller, achievable milestones, and celebrate each accomplishment along the way. This approach fosters a sense of progress and motivation, keeping you on track towards your retirement target.

Don't forget to factor in potential changes in your lifestyle. Your needs may evolve as you age, and your retirement savings plan should accommodate these changes. Consider potential changes in housing arrangements, travel plans, and other lifestyle adjustments that might impact your expenses. A flexible plan allows you to adapt to unforeseen circumstances and remain financially secure in your golden years.

Choosing the Right Investment Strategies

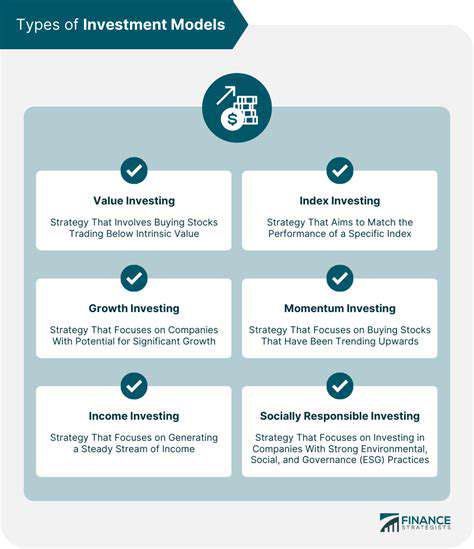

Selecting appropriate investment strategies is crucial for maximizing your retirement savings. Diversification across various investment vehicles is key to mitigate risk and potentially increase returns. Understanding different investment options, such as stocks, bonds, mutual funds, and real estate, is essential to make informed decisions. Researching and understanding the potential risks and rewards associated with each investment type will help you construct a portfolio that aligns with your risk tolerance and financial objectives. It is important to remember that past performance is not indicative of future results.

Seek professional financial advice when necessary. A qualified financial advisor can provide personalized guidance on investment strategies tailored to your individual circumstances and risk tolerance. Their expertise can help you navigate the complexities of the investment world and make sound financial decisions to optimize your retirement savings. This is particularly important in complex situations or when you require personalized advice.

Implementing and Monitoring Your Plan

Developing a savings plan is only the first step. Implementing and consistently monitoring your plan is crucial for achieving your retirement goals. Regular contributions, even small ones, consistently added to your savings, can make a significant difference in the long run. Set up automatic transfers from your checking account to your retirement savings account to ensure you stay on track. This automatic system helps maintain discipline and consistency in your savings routine.

Regular reviews and adjustments are essential to ensure your plan remains aligned with your evolving circumstances. Periodically review your investments, recalculate your savings goals, and consider making adjustments to your strategy as needed. This proactive approach helps you stay on track and adapt to any changes in your financial situation or life goals. Monitoring your progress and making necessary adjustments ensures your retirement savings plan remains effective and meets your needs.

Seeking Professional Guidance

Understanding Your Financial Landscape

Before embarking on a retirement savings journey while simultaneously tackling debt, it's crucial to have a clear understanding of your current financial situation. This involves meticulously analyzing your income, expenses, and existing debt obligations. Detailed budgeting is paramount, identifying areas where you can potentially cut back on unnecessary spending and allocate more funds towards both debt reduction and retirement savings. This initial assessment will provide a solid foundation for developing a personalized financial plan.

A crucial step is to categorize your expenses. Are there areas where you can realistically reduce spending without sacrificing essential needs? Understanding your spending habits is key to identifying potential savings opportunities. This self-assessment will equip you with a clear picture of your financial standing and the potential for future savings.

Prioritizing Debt Repayment

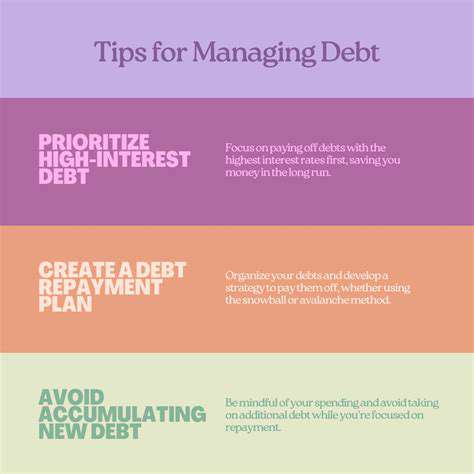

Aggressive debt repayment strategies are essential for freeing up funds for retirement savings. A well-structured debt repayment plan, often involving the debt snowball or avalanche methods, can accelerate the process of eliminating high-interest debt. Prioritizing high-interest debts will save you money in interest payments in the long run and free up funds for other financial goals.

Developing a Realistic Retirement Savings Plan

Retirement savings plans require careful consideration of your future needs and anticipated retirement lifestyle. This involves estimating the amount of money you will need to comfortably support yourself in retirement. Factors like inflation, expected lifespan, and desired living standards play a crucial role in determining the appropriate retirement savings target.

Consider different savings vehicles, such as 401(k)s, IRAs, or Roth IRAs, each with its own set of advantages and disadvantages. Researching these options and understanding their tax implications is essential for maximizing your savings potential. A qualified financial advisor can provide personalized guidance on selecting the most suitable options for your circumstances.

Creating a Balanced Budget

A balanced budget is the cornerstone of both debt reduction and retirement planning. It involves meticulous tracking of income and expenses, ensuring that your spending aligns with your income. Identifying and eliminating unnecessary expenses is crucial for freeing up funds for both debt repayment and retirement savings. Regular review and adjustments to your budget are vital for maintaining financial stability and achieving your financial goals.

Seeking Professional Advice

Navigating the complexities of debt repayment and retirement planning can be challenging. Seeking professional guidance from a qualified financial advisor can provide valuable insights and personalized strategies. A financial advisor can help you develop a comprehensive financial plan that takes into account your specific circumstances and goals. They can also provide guidance on investment strategies and asset allocation for your retirement savings.

Don't underestimate the value of professional advice. A financial advisor can offer invaluable support in making informed decisions about your finances, ensuring that you are on the right path to achieving your long-term financial goals.

Read more about How to Save for Retirement While Paying Off Debt

![How to Build an Emergency Fund [Step by Step]](/static/images/30/2025-04/Step53AReplenishYourEmergencyFundWhenNecessary.jpg)

Hot Recommendations

- Tax Planning Tips for Homeowners [2025]

- How to Get Insurance for a Short Term Rental Property

- Understanding the Benefits of a Roth IRA

- How to Manage Business Debt After a Downturn

- How to Use a Barbell Investment Strategy

- Best Ways to Track Your Progress Towards Financial Freedom

- Tips for Managing Credit Card Rewards While Paying Off Balances

- Tax Planning Tips for Stock Options

- How to Plan for Retirement if You Didn't Save Early

- Guide to Managing Legal Debt