Best Travel Insurance Policies [2025 Review]

Understanding Your Needs

Selecting travel insurance isn't just about ticking boxes - it's about crafting a safety net tailored to your journey's unique contours. Your destination's healthcare costs, local crime rates, and even weather patterns should directly influence your coverage choices. I've learned through experience that skimping on medical coverage for a hiking trip in the Andes can lead to six-figure emergency evacuation bills.

Seasoned travelers develop a sixth sense for risk assessment. That time my connecting flight got canceled in Frankfurt taught me the real value of trip interruption coverage. Always scrutinize the fine print for covered reasons - most policies won't pay out if you simply change your mind. The devil's in the details when it comes to pre-existing condition clauses too.

Evaluating Different Policy Types

Travel insurance isn't one-size-fits-all. The backpacker hopping between hostels needs vastly different coverage than the retiree on a Mediterranean cruise. Adventure sports riders can make or break a policy - my friend's rock climbing accident in Thailand wasn't covered under his basic plan.

Annual multi-trip policies shine for frequent flyers, but watch the duration limits per trip. That business traveler making twelve international trips yearly could save hundreds compared to buying separate policies. Conversely, cruise enthusiasts should prioritize cancel for any reason upgrades - ships don't wait for late arrivals.

Comparing Costs and Coverage

The cheapest premium often becomes the most expensive mistake when claims get denied. I always cross-reference coverage limits with my destination's realities - $50,000 medical coverage means little in U.S. hospitals where a broken leg can cost $30,000.

Deductibles work differently in travel insurance than auto policies. That $250 deductible might apply per incident rather than per trip, turning multiple small claims into financial drains. Savvy travelers balance premiums with realistic risk assessments - sometimes paying slightly more upfront prevents massive out-of-pocket costs later.

Coverage Areas: Essential Protections for Every Traveler

Comprehensive Medical Coverage

International hospitals don't bill your domestic insurance. Quality medical coverage should mirror your destination's healthcare costs - $100,000 minimum for the U.S., less for countries with socialized medicine. Emergency dental coverage saved me $3,000 when a crown failed in Barcelona.

Emergency Assistance and Support

When my wallet got stolen in Rome, the insurance company's 24/7 helpline arranged emergency cash and guided me to the right police station. This service becomes priceless when language barriers or unfamiliar legal systems complicate crises. They even helped replace my prescription glasses within hours.

Trip Interruption and Cancellation Protection

That non-refundable $5,000 safari? Hurricane season makes cancellation coverage essential. Pro tip: Policies with cancel for any reason (CFAR) upgrades typically refund 75% and provide peace of mind for unpredictable life events. Just remember to purchase within 10-21 days of your first trip payment.

Lost Luggage and Baggage Coverage

Airlines frequently lose bags on complex itineraries - my three-baggage-delay claims last year proved the value of this coverage. Smart travelers photograph their packed bags and keep receipts for high-value items to streamline claims. The $100/day for essentials softens the blow when your luggage tours Europe without you.

Liability Protection and Legal Expenses

When a rental scooter incident in Bali left a local injured, my policy's liability coverage handled the $15,000 in medical bills. This often-overlooked protection becomes critical in litigious countries or when engaging in risky activities. Always verify coverage amounts meet local legal requirements.

Comparing Policies: Evaluating Benefits and Costs

Policy Comparison Strategies

Effective comparison requires creating a spreadsheet tracking: medical limits, evacuation costs, pre-existing condition clauses, and adventure activity inclusions. I weight each category based on trip specifics - medical gets 40% for U.S. trips but only 20% for EU travels with reciprocal healthcare.

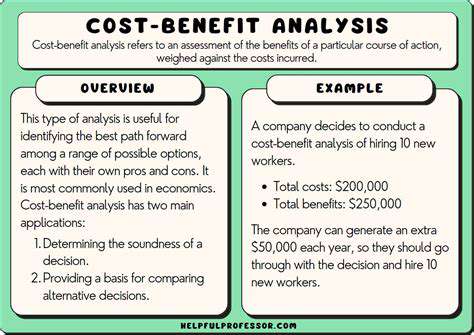

Cost-Benefit Analysis

That $200 premium might seem steep until you calculate potential losses: $3,000 non-refundable tour + $1,500 flights + $800 hotels. My rule: Premium shouldn't exceed 10% of non-refundable trip costs unless traveling to high-risk areas. For risky destinations, I'll pay up to 15% for superior coverage.

Provider Reliability Assessment

Online reviews reveal claim payment patterns - some insurers fight every claim while others process smoothly. I prioritize companies with 24/7 direct contact options after being stranded overnight with a defunct 800 number. AM Best ratings below A- get automatically disqualified from my comparisons.

Mindfulness techniques prove invaluable when travel stress mounts. Deep breathing during flight delays and conscious observation during chaotic border crossings have saved my sanity countless times.

Crucial Considerations: Trip Type and Destination Impact

Destination-Specific Risks

Political instability in some regions necessitates evacuation coverage, while remote locations demand higher medical limits. My Antarctica expedition required $500,000 emergency evacuation coverage - standard $100,000 policies became useless. Always research destination-specific risks through government travel advisories.

Activity-Based Coverage Needs

That free snorkeling excursion? Most basic policies exclude it. I now pay extra for hazardous sports riders after a parasailing incident in Mexico nearly bankrupted me. Even zip-lining and hot air ballooning often require special endorsements.

Duration and Frequency Factors

Month-long trips face different risks than weekend getaways. My 60-day Asian journey needed special long-stay coverage as most policies cap at 30-45 days. Frequent travelers should compare annual plans - mine saved $1,200 last year over buying individual policies.

Read more about Best Travel Insurance Policies [2025 Review]

![Best Life Insurance Policies [2025 Review]](/static/images/30/2025-05/AssessingPermanentLifeInsuranceOptions.jpg)

![Best Health Insurance Plans for Families [2025]](/static/images/30/2025-05/EvaluatingCoverageandBenefits.jpg)

Hot Recommendations

- Tax Planning Tips for Homeowners [2025]

- How to Get Insurance for a Short Term Rental Property

- Understanding the Benefits of a Roth IRA

- How to Manage Business Debt After a Downturn

- How to Use a Barbell Investment Strategy

- Best Ways to Track Your Progress Towards Financial Freedom

- Tips for Managing Credit Card Rewards While Paying Off Balances

- Tax Planning Tips for Stock Options

- How to Plan for Retirement if You Didn't Save Early

- Guide to Managing Legal Debt