Budgeting for Living Alone

Managing Unexpected Expenses and Building an Emergency Fund

Budgeting for the Unexpected

Creating a robust budget is crucial for managing unexpected expenses. A well-defined budget allows you to anticipate potential financial shocks and allocate funds for unforeseen circumstances, such as car repairs, medical bills, or appliance malfunctions. This proactive approach minimizes the impact of these unexpected costs on your overall financial stability.

Regularly reviewing and adjusting your budget based on your income and expenses is essential. This process allows you to identify potential financial gaps and make necessary adjustments before an unexpected expense arises.

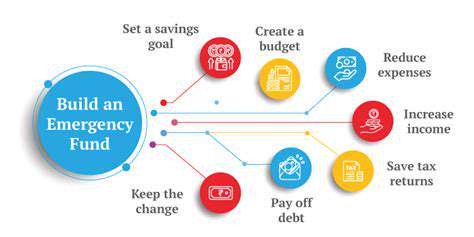

Emergency Fund Essentials

Establishing an emergency fund is paramount to handling unexpected financial burdens. This fund acts as a safety net, providing a buffer against unforeseen events and preventing you from accumulating debt or relying on high-interest loans. An emergency fund should ideally cover three to six months of living expenses.

Regular contributions to this fund, even small amounts, can significantly contribute to its growth and provide peace of mind during difficult times.

Insurance Coverage Options

Comprehensive insurance coverage is vital for safeguarding against substantial unexpected expenses. Health insurance, auto insurance, and home insurance protect you from significant financial losses associated with accidents, illnesses, and property damage. Review your current insurance policies to ensure they adequately cover your needs and consider adding additional coverage as necessary.

Utilizing Credit Wisely

Understanding and utilizing credit responsibly is important when managing unexpected expenses. Knowing your credit limits and interest rates will allow you to make sound financial decisions. Credit cards can be useful tools for managing short-term financial needs, but using them wisely and paying off balances promptly is essential to avoid accumulating high-interest debt.

Seeking Financial Guidance

Don't hesitate to reach out to financial advisors or counselors for guidance. They can provide valuable insights and strategies to help you navigate unexpected financial situations effectively. Professional guidance can offer tailored advice based on your specific circumstances and help you develop a comprehensive financial plan.

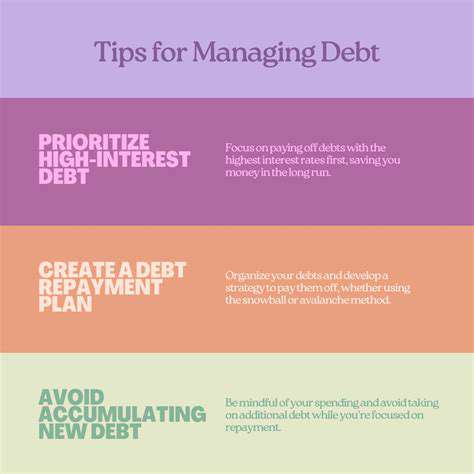

Debt Management Strategies

Developing effective debt management strategies is essential for dealing with unexpected expenses. If you're facing mounting debt, exploring options like debt consolidation or balance transfers can help you manage your financial obligations more effectively. These strategies can help you reduce your monthly payments and potentially lower interest rates.

Negotiating with Providers

Sometimes, negotiating with service providers can significantly reduce the cost of unexpected expenses. Before resorting to high-interest loans or credit cards, consider contacting providers to see if they offer payment plans or discounts. This proactive approach can sometimes lead to substantial cost savings, allowing you to manage unexpected expenses more effectively.

Tracking Your Progress and Making Adjustments

Understanding Your Expenses

Living independently often means a shift in expenses. Careful tracking of your daily spending, from groceries and utilities to entertainment and transportation, is crucial for budgeting. This initial understanding of where your money goes is the first step in making informed decisions about your financial future. It's not just about the big ticket items; even seemingly small purchases can add up quickly, impacting your overall budget if not monitored closely. Regularly reviewing your spending patterns provides valuable insights into areas where you might be able to cut back or adjust your spending habits.

Analyzing your income and expenses will allow you to identify areas where you can save money and make informed decisions about your financial well-being. This step is vital for creating a sustainable budget that supports your lifestyle while considering future financial goals.

Defining Your Needs and Wants

Differentiating between essential expenses (rent, utilities, groceries) and discretionary spending (dining out, entertainment) is key to effective budgeting. Understanding your needs and wants will help you prioritize your spending and avoid unnecessary expenses that can quickly erode your savings. This distinction allows you to allocate funds strategically and make informed choices about where to spend your money, ensuring that your budget aligns with your priorities.

Creating a Realistic Budget

A budget that's too restrictive can lead to feelings of deprivation, making it harder to stick to. Conversely, one that's too lenient might not effectively manage your finances. Aim for a realistic budget that accounts for your income and all your essential expenses. This means accurately calculating your monthly income and realistically assessing your expenses, including unexpected costs. Remember to factor in savings goals and any potential debts.

Setting Realistic Savings Goals

Saving for emergencies, future investments, or even just a fun vacation is an important part of living independently. Setting realistic savings goals will help you visualize your financial future. Start small, and gradually increase your savings as your income and expenses stabilize. By setting achievable goals, you can stay motivated and committed to your financial plan. This will build a solid foundation for future financial security.

Monitoring and Adjusting Your Budget

Budgeting is not a one-time action; it's an ongoing process. Regularly review your budget to track your progress and identify areas where you can make adjustments. Unexpected expenses may arise, and you might find your spending habits change over time. Staying flexible and adaptable to these changes is crucial for maintaining a healthy financial life.

Using Budgeting Tools and Resources

Numerous budgeting apps and tools can help you track your expenses, monitor your progress, and stay on top of your financial goals. Explore these resources to find one that suits your needs and preferences. Utilize these tools to visualize your spending patterns and identify areas for improvement. Learning to use budgeting tools effectively can empower you to take control of your finances and make informed choices.

Seeking Professional Advice When Needed

If you're struggling to create or maintain a budget, don't hesitate to seek professional financial advice. A financial advisor can provide personalized guidance and support, helping you develop a budget that aligns with your specific circumstances and goals. They can help you navigate complex financial situations and ensure your financial well-being is managed effectively.

Read more about Budgeting for Living Alone

![How to Build an Emergency Fund [Step by Step]](/static/images/30/2025-04/Step53AReplenishYourEmergencyFundWhenNecessary.jpg)

![Best Tools for Debt Management [2025]](/static/images/30/2025-05/DebtManagementPlans28DMPs293APersonalizedStrategiesforRepayment.jpg)

Hot Recommendations

- Tax Planning Tips for Homeowners [2025]

- How to Get Insurance for a Short Term Rental Property

- Understanding the Benefits of a Roth IRA

- How to Manage Business Debt After a Downturn

- How to Use a Barbell Investment Strategy

- Best Ways to Track Your Progress Towards Financial Freedom

- Tips for Managing Credit Card Rewards While Paying Off Balances

- Tax Planning Tips for Stock Options

- How to Plan for Retirement if You Didn't Save Early

- Guide to Managing Legal Debt