Guide to Long Term Care Insurance

Geographical cost variations dramatically affect planning. Researching local care facility pricing - from basic assisted living to full nursing care - provides realistic financial benchmarks. These figures help determine necessary coverage amounts while preventing both underinsurance and unnecessary premium expenses.

How Long-Term Care Insurance Works

Policies typically operate through defined benefit structures, paying either daily or monthly amounts toward care costs. Activation usually occurs when policyholders can no longer perform basic daily activities independently or require skilled nursing intervention. The exact triggering mechanisms and benefit periods vary considerably between policies, making thorough policy document review non-negotiable.

Understanding policy mechanics relative to personal circumstances prevents unpleasant surprises. Key elements requiring clarification include elimination periods (waiting times before benefits start), benefit duration caps, and any coverage exclusions for pre-existing conditions or specific treatments.

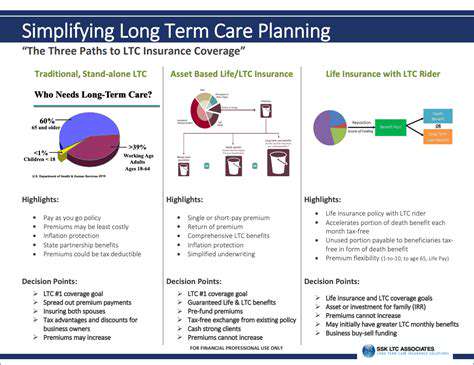

Policy Types and Considerations

The insurance market offers diverse policy structures catering to different needs and budgets. Traditional indemnity policies provide fixed daily amounts, while comprehensive plans might combine multiple coverage types. Comparing policies requires evaluating not just premium costs but also benefit flexibility, inflation protection options, and carrier financial stability.

Personal factors significantly influence policy selection. Age affects premium costs dramatically - purchasing earlier generally secures better rates. Health status at application time impacts both eligibility and pricing. Financial advisors specializing in eldercare can provide invaluable guidance navigating these complex decisions.

The Importance of Early Planning

Proactive planning for potential care needs offers multiple advantages. Early policy acquisition typically means lower premiums and broader coverage options. Delaying this decision often results in either unaffordable premiums or limited coverage due to emerging health issues that might make qualification difficult.

Initiating family discussions about care preferences and financial planning prevents future conflicts during stressful situations. Documenting preferences regarding care settings (home vs facility) and designating decision-makers in advance provides crucial guidance when needed most.

Key Considerations When Choosing a Policy

Choosing the Right Materials

Material selection impacts long-term outcomes across various contexts. Optimal choices balance durability, cost efficiency, and environmental considerations. The most effective materials align precisely with project requirements while accommodating anticipated stress factors and quality standards. This selection process benefits from comparative analysis of material properties and professional consultations.

Material characteristics vary widely - some prioritize structural integrity while others emphasize aesthetic qualities. Recognizing these differences enables informed decisions supporting project objectives. Expert input combined with comprehensive research consistently produces superior results.

Budgetary Constraints and Financial Planning

Financial realities fundamentally shape project execution. Realistic budgeting prevents mid-project financial crises through accurate cost forecasting and contingency planning. Comprehensive cost analysis should encompass materials, labor, permits, and unexpected expenses.

Clear financial understanding enables strategic resource allocation throughout project phases. This disciplined approach minimizes financial strain while maintaining project momentum and quality standards.

Timeline and Project Management

Effective scheduling forms the backbone of successful project completion. Detailed timelines should identify critical milestones, task durations, and dependency relationships. Modern project management emphasizes clear communication protocols, defined responsibilities, and regular progress monitoring.

Consistent team communication and proactive issue resolution prevent most schedule disruptions while maintaining work quality. Digital collaboration tools have revolutionized real-time progress tracking and team coordination.

Risk Assessment and Mitigation Strategies

Comprehensive risk analysis examines both internal and external threat factors. Market volatility, regulatory changes, and supply chain disruptions represent common external risks. Internally, skill gaps, equipment failures, and miscommunications require mitigation planning.

Early risk identification enables proactive countermeasures that dramatically reduce negative impacts. Effective strategies often combine insurance products, contractual protections, and operational redundancies tailored to specific project vulnerabilities.

Types of Long-Term Care Insurance Policies

Traditional Long-Term Care Insurance

Traditional policies offer the most comprehensive coverage options for extended care needs. Benefits typically pay directly toward nursing home costs, assisted living facilities, or in-home care services, with customizable coverage amounts matching regional care costs. Policyholders can often select benefit periods (2-5 years or lifetime) and daily benefit amounts ($100-$500+), creating flexible solutions for different budgets.

Customization options represent both an advantage and complexity source. While allowing precise coverage tailoring, the numerous choices require careful analysis to avoid coverage gaps or unnecessary premium expenses. Inflation protection riders prove particularly valuable for policies purchased decades before likely need.

Hybrid Long-Term Care Insurance

Hybrid products merge long-term care coverage with life insurance or annuity features. These innovative solutions appeal to those seeking multiple protections within single policies, often with premium guarantees and death benefit components. The combined approach frequently offers more underwriting flexibility than traditional standalone policies.

Some hybrid designs allow unused long-term care benefits to convert to enhanced death benefits. Others incorporate return-of-premium features if care needs never materialize. Policy structures vary widely between carriers, necessitating detailed comparisons.

Medicare and Medicaid as Potential Alternatives

Government programs play complicated roles in long-term care financing. Medicare provides extremely limited coverage - typically just short-term skilled nursing following hospitalizations - while Medicaid requires asset depletion to qualify for comprehensive benefits. Understanding these programs' strict eligibility requirements helps evaluate private insurance needs.

Medicaid planning strategies exist but often require legal assistance to implement properly years before needing care. Consulting elder law attorneys can clarify options while preserving assets through legitimate means. These programs work best as supplements rather than primary solutions for most middle-class families.

Daily joy cultivation transforms ordinary existence when practiced consistently. Modern life's frantic pace often obscures countless micro-moments of beauty and connection. That perfect morning beverage temperature, dappled sunlight patterns, or spontaneous human kindness - these fragments assemble into life's richest tapestry. Conscious attention to present-moment details doesn't just enhance perception - it fundamentally alters experience quality. The mundane becomes magical through deliberate noticing.

Important Factors to Assess for Your Needs

Financial Considerations

Comprehensive financial analysis underpins sound insurance decisions. This extends beyond current assets to include projected retirement income, potential inheritances, and anticipated healthcare costs. Evaluating premium affordability against potential future income reductions ensures policies remain sustainable during retirement years. Policy features like shared care options for couples or inflation protection significantly impact long-term value.

Detailed policy comparisons should examine benefit triggers, elimination periods, and coverage exclusions. Understanding exactly how and when benefits activate prevents unpleasant claim surprises. Premium payment options (single pay, limited pay, or ongoing) offer additional flexibility for different financial situations.

Care Needs and Preferences

Personal care preferences significantly influence policy selection. Some prioritize remaining at home with assistance, while others prefer facility care options. Evaluating potential needs for specialized memory care or rehabilitation services ensures adequate coverage for likely scenarios.

Geographical considerations matter greatly - urban areas typically offer more care options than rural locations, often at higher costs. Documenting specific care preferences in advance guides both policy selection and future care decisions during challenging times. This planning prevents rushed decisions during health crises when emotions run high.

Family support availability dramatically affects care needs. Those with involved family members might require different coverage levels than those without local support networks. Realistically assessing potential caregiver burnout scenarios helps determine necessary professional care coverage.

Future medical advancements could alter care landscapes. While impossible to predict precisely, considering potential treatment innovations for chronic conditions informs flexible policy design. Coverage that adapts to evolving care modalities offers particular value.

Read more about Guide to Long Term Care Insurance

![Best Tools for Debt Management [2025]](/static/images/30/2025-05/DebtManagementPlans28DMPs293APersonalizedStrategiesforRepayment.jpg)

![Best Health Insurance Plans for Families [2025]](/static/images/30/2025-05/EvaluatingCoverageandBenefits.jpg)