Tips for Paying Off Your Car Loan Faster

Maximize Your Monthly Payments: Going Beyond the Minimum

Understanding Your Payment Structure

A crucial first step in maximizing your monthly payments is understanding the specific structure of your debt. This includes knowing the minimum payment amount, the interest rate, and the total balance. Understanding these components allows you to strategize effectively and avoid falling into a cycle of endless debt. Accurate knowledge of your payment schedule is paramount for making informed decisions about how to manage your finances and work towards paying off your debts efficiently.

Often, the minimum payment is just enough to keep your account active, but it rarely, if ever, addresses the principal balance. This means that most of your payment goes towards interest, which can significantly increase the overall cost of your debt over time. This understanding is essential to move beyond the minimum and start actively reducing the principal balance.

Prioritizing High-Interest Debts

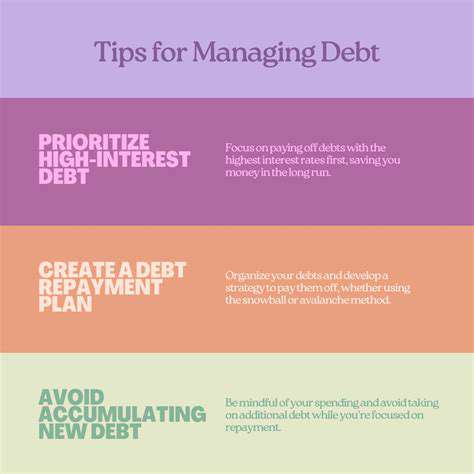

A critical strategy for maximizing your monthly payments involves prioritizing debts with the highest interest rates. By focusing on these debts first, you're significantly reducing the total interest you pay over the life of the loan. This approach is often referred to as the debt snowball or debt avalanche method, and both have proven effective strategies for accelerated debt repayment.

Paying down high-interest debts quickly reduces the overall interest accrued, freeing up more money for other financial goals. This targeted approach is more than just a mathematical exercise; it's a strategic approach to financial freedom.

Creating a Realistic Budget

A well-defined budget is essential for effectively managing your finances and making informed decisions about your payments. Creating a realistic budget involves meticulously tracking your income and expenses, identifying areas where you can cut back, and allocating specific portions of your income to debt repayment. This detailed analysis allows you to make conscious decisions about where your money goes and to prioritize debt reduction effectively.

Exploring Additional Income Streams

Sometimes, the most efficient way to increase monthly payments is to explore opportunities to generate additional income. This could involve taking on a part-time job, freelancing, selling unused items, or investing in income-generating assets. Exploring additional income streams provides extra funds that can be directly applied to your debts, accelerating the repayment process significantly.

Even a small increase in income can have a substantial impact on your ability to pay off debt faster. This proactive approach leverages your financial ingenuity to work towards your financial goals.

Automating Your Payments

Automating your debt payments can eliminate the risk of missed payments and ensures consistent contributions toward your debt reduction goals. Setting up automatic transfers from your checking account to your various debt accounts can contribute to a more disciplined approach to repayment. This automation streamlines the process and promotes consistency, minimizing the likelihood of errors or forgetfulness.

Considering Debt Consolidation or Refinancing

In some cases, consolidating or refinancing your debts might be a viable strategy to potentially reduce your overall interest burden and increase your monthly payments. Debt consolidation involves combining multiple debts into one, while refinancing involves obtaining a new loan with more favorable terms. Both options can lead to lower monthly payments if the new terms are more advantageous. However, carefully evaluating the terms and conditions is critical before making any decisions.

Consider the potential implications of each approach, including any associated fees or changes in interest rates, to make the most informed decision regarding your debt management plan.

The Power of Extra Payments: Strategically Applying Extra Funds

Maximizing Your Savings with Extra Payments

Extra payments aren't just about getting rid of debt faster; they're a powerful tool for building a stronger financial foundation. By consistently allocating extra funds towards your debts or savings, you're effectively accelerating your progress towards your financial goals. This proactive approach not only reduces the total interest paid over the life of a loan but also provides a significant psychological boost, as you witness tangible progress towards financial freedom. Think of it as a mini-celebration every time you make an extra payment, reinforcing positive habits and encouraging further savings.

Prioritizing High-Interest Debts

When you have multiple debts, strategically targeting high-interest debts with extra payments is crucial. This approach minimizes the overall cost of borrowing by focusing on the loans that accrue the most interest. Instead of spreading your extra funds thinly across all debts, concentrate on the ones with the highest interest rates, effectively chipping away at the most expensive portions of your debt burden. This focused strategy significantly reduces the total interest you'll pay over time, saving you substantial money in the long run.

A clear understanding of which debts have the highest interest rates is paramount to successful debt management. This knowledge allows you to strategically allocate your extra funds for maximum impact.

Establishing a Consistent Payment Schedule

Integrating extra payments into your regular budget is key to long-term success. This doesn't mean you need to drastically alter your spending habits; rather, it involves identifying small, consistent adjustments to your budget. This could involve setting aside a fixed amount each week or month, even if it's just a few dollars. Regular contributions to your debt repayment efforts cultivate a powerful momentum, building upon each extra payment and leading to faster debt reduction.

Understanding the Impact on Loan Terms

Making extra payments often results in a quicker payoff of your loan, thereby reducing the overall time you spend repaying it. This can significantly impact your loan terms, reducing the total interest you accrue over time. It's essential to understand how your lender will calculate the payoff based on the extra payments made. This knowledge helps you manage expectations and track the progress you're making toward debt elimination.

Adapting to Changing Financial Circumstances

Financial circumstances can change, and it's important to adapt your strategy accordingly. If income fluctuates or unexpected expenses arise, be prepared to adjust your extra payment amounts. Flexibility is key to maintaining a sustainable plan for managing debt. This proactive approach prevents derailment from your financial goals and allows you to navigate potential obstacles with a well-defined plan. It's about building a financial strategy that adapts to life's inevitable changes.

Bridge, that classic trick-taking card game played by four people, stands out for its deep strategy and intricate player interactions. What sets it apart from simpler card games is how players must constantly assess not just their own cards, but also anticipate their partners' and opponents' moves. This multi-layered analysis forms the core of developing winning approaches.

Embrace the Power of Refinancing: A Potential Game Changer

Understanding the Refinancing Process

Refinancing is essentially taking out a new loan to pay off an existing one, typically a mortgage or a personal loan. It's a strategic move that can significantly impact your financial situation, and it's crucial to understand the entire process before jumping in. This involves comparing interest rates, fees, and terms offered by different lenders to find the most advantageous deal. Thorough research and careful consideration are key to making an informed decision. Understanding the potential benefits and drawbacks is essential to maximizing the potential of refinancing.

A critical aspect of the refinancing process is evaluating your current financial situation. Factors such as your credit score, the remaining balance on your existing loan, and your income play a substantial role in determining your eligibility and the terms offered. A strong credit score generally leads to more favorable interest rates, while a larger outstanding balance might influence the total cost of the new loan. A thorough review of your financial profile is essential to ensure that refinancing aligns with your long-term financial goals and minimizes potential risks.

Potential Benefits and Drawbacks of Refinancing

Refinancing can offer substantial benefits, such as lower monthly payments, reduced interest costs over the life of the loan, and potentially a shorter loan term. This can lead to significant savings in the long run, freeing up more of your budget for other financial priorities. However, it's important to be aware of the potential drawbacks, such as closing costs associated with the new loan and any penalties for early repayment of the original loan. These costs can sometimes offset the benefits, so a careful cost-benefit analysis is vital before making a decision.

Another important consideration is the impact on your credit score. While refinancing itself can positively impact your financial situation, a new loan application can potentially affect your credit score, especially if not handled correctly. It's crucial to understand how different lenders assess your creditworthiness and to make the application process as smooth as possible. A thorough understanding of the potential effects on your credit score is essential for a sound financial strategy.

Moreover, refinancing can help consolidate debt, which can simplify your financial management. It can lower your overall interest burden and allow for more focused budgeting. However, it's essential to weigh the potential benefits against the costs and ensure that the new loan terms are truly advantageous. This includes evaluating the overall financial picture and identifying any potential downsides before making a significant financial commitment.

Read more about Tips for Paying Off Your Car Loan Faster

![Best Life Insurance Policies [2025 Review]](/static/images/30/2025-05/AssessingPermanentLifeInsuranceOptions.jpg)

![Best Debt Management Plans [2025 Review]](/static/images/30/2025-05/NavigatingtheApplicationProcessandOngoingManagement.jpg)

![Best Health Insurance Plans for Families [2025]](/static/images/30/2025-05/EvaluatingCoverageandBenefits.jpg)

Hot Recommendations

- Tax Planning Tips for Homeowners [2025]

- How to Get Insurance for a Short Term Rental Property

- Understanding the Benefits of a Roth IRA

- How to Manage Business Debt After a Downturn

- How to Use a Barbell Investment Strategy

- Best Ways to Track Your Progress Towards Financial Freedom

- Tips for Managing Credit Card Rewards While Paying Off Balances

- Tax Planning Tips for Stock Options

- How to Plan for Retirement if You Didn't Save Early

- Guide to Managing Legal Debt