How to Stop Overspending and Start Saving

Organize expenses into clear buckets (housing, food, transportation) to spot trends. Are certain categories consistently over budget? Do impulse buys or unused subscriptions quietly drain your resources? This financial x-ray forms the bedrock of intelligent money management.

Crafting a Budget That Works

With spending patterns revealed, design a budget that breathes with your life. Think of it as a financial GPS rather than handcuffs - it should guide while allowing for detours. Include all income streams and categorize expenses realistically, remembering that perfect budgets often fail first.

Account for both predictable costs (rent) and flexible ones (entertainment). Base allocations on your actual spending history, not wishful thinking. The most effective budget is one you'll actually follow, not just admire.

Trimming Financial Fat

Examine your budget with surgical precision. That gym membership collecting dust? The daily takeout habit? These financial vampires might be bleeding your savings dry. Small cuts across multiple areas can yield surprisingly large savings.

Scrutinize recurring charges - are all those streaming services essential? Could generic brands satisfy as well as name brands? Financial freedom often lives in these small, consistent decisions.

Building Your Savings Muscle

Create a savings blueprint matching your ambitions. Whether it's a safety net, dream vacation, or home down payment, define what success looks like. Start with what you can manage, even if it's modest - consistency trumps amount.

Sequence your goals wisely. An emergency fund comes first - it's your financial seatbelt. Then tackle other aspirations, breaking them into bite-sized milestones to maintain momentum.

Conquering Debt Strategically

Attack high-interest debt first - credit cards are public enemy number one. Consider proven methods like the debt snowball (small wins first) or avalanche (save on interest) approaches to gain traction.

Explore debt consolidation carefully. While lower interest rates help, watch for hidden fees. The right debt strategy feels like getting a raise without changing jobs.

Financial Check-Ups

Schedule regular money reviews. Life evolves, and so should your budget. Treat adjustments as course corrections, not failures - flexibility is the hallmark of lasting financial health.

When goals feel distant, diagnose why. Maybe your budget needs tweaking or spending habits need refining. Financial success isn't about perfection, but persistent progress.

Emotional well-being represents our capacity to navigate life's emotional currents, managing thoughts and feelings while maintaining equilibrium during challenges.

Embracing a Minimalist Mindset

Decoding Spending Motivations

Overspending often masks deeper needs - emotional voids, social pressures, or self-esteem gaps. Recognizing these root causes transforms money management from punishment to self-care. This awareness allows customized strategies addressing your unique spending triggers.

When the shopping urge strikes, pause. Is this purchase filling an emotional tank or an actual need? Understanding this difference can reroute spending impulses toward healthier outlets.

Mapping Your Spending Triggers

Identify your financial pressure points with journal-like precision. Does stress open your wallet? Does social media create artificial needs? Tracking spending alongside emotions reveals powerful patterns.

These insights become your financial playbook. Knowing your triggers lets you design preemptive strategies, like a 24-hour cooling period for non-essential purchases.

Budgeting for Freedom

A thoughtful budget isn't a cage - it's the framework for financial liberation. It ensures money flows toward what truly matters to you. The best budgets have breathing room for life's pleasures while securing tomorrow.

Build flexibility into your plan. Life changes, and so should your budget - it's a living document, not carved in stone.

The Art of Consistent Saving

Saving is less about amounts and more about rhythm. Automate small, regular transfers to make saving painless. Watch how out of sight, out of mind grows your safety net effortlessly.

Small amounts accumulate surprisingly fast - the real magic lies in starting, not the initial sum.

Conscious Spending

Before purchasing, ask: Does this align with my bigger financial picture? This moment of reflection can prevent countless impulse buys. It's not about deprivation, but about ensuring each dollar reflects your priorities.

Mindful spending creates financial clarity. When you spend with intention, you naturally spend less on what doesn't matter.

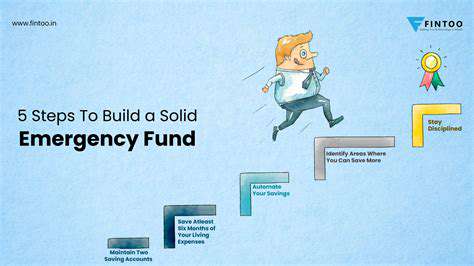

Building an Emergency Fund

Why Emergency Funds Matter

An emergency fund is financial armor, protecting against life's surprises - job transitions, medical bills, or urgent repairs. Without it, these events can trigger debt spirals. This fund keeps surprises from becoming crises.

This preparation brings peace of mind. Knowing you're covered allows clearer thinking during challenges, preventing rash financial decisions.

Setting Your Savings Target

Calculate your safety net based on actual living expenses, not arbitrary numbers. Typically, three to six months' coverage provides solid protection. Adjust based on job stability and obligations.

Start where you are. Even $500 creates breathing room. The key is beginning, then building gradually.

Budgeting for Protection

Your budget should spotlight emergency savings as a non-negotiable, like rent. Tracking progress creates motivation - watching the fund grow reinforces the habit.

Regular budget reviews help identify new saving opportunities, keeping your emergency fund growing steadily.

Smart Saving Tactics

Automate transfers to make saving effortless. Start small if needed - consistency matters more than initial amounts. As raises come, increase contributions proportionally.

Consider parking funds in high-yield accounts to combat inflation while keeping money accessible.

Making Savings Priority One

Treat emergency savings like a bill that must be paid - to yourself. This mindset shift transforms saving from optional to essential. Postpone non-essentials until your safety net is secure.

View every dollar saved as buying future peace of mind - the ultimate luxury purchase.

Maintaining Your Financial Buffer

Once established, review your fund annually. Life changes may require adjustments. Consider laddering CDs or other low-risk options for portions of larger funds to earn better returns while maintaining liquidity.

Remember, this fund isn't static - it should evolve as your life and responsibilities do.

Read more about How to Stop Overspending and Start Saving

![Best Life Insurance Policies [2025 Review]](/static/images/30/2025-05/AssessingPermanentLifeInsuranceOptions.jpg)

![Best Homeowners Insurance Companies [2025 Review]](/static/images/30/2025-05/TopTierHomeownersInsuranceProvidersin2025.jpg)

![Best Renters Insurance Companies [2025 Review]](/static/images/30/2025-05/CompanyB3AExcellentCustomerService26ClaimsHandling.jpg)

![Best Budgeting Software for Families [2025]](/static/images/30/2025-05/EvaluatingPopularBudgetingSoftwareOptionsforFamilies.jpg)