How to Understand Your Homeowners Insurance Deductible

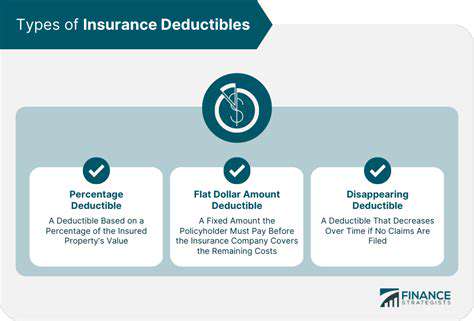

Different Types of Deductibles

Deductibles in Health Insurance

Health insurance deductibles are a crucial aspect of understanding your coverage. They represent the amount you're responsible for paying out-of-pocket before your insurance company starts covering medical expenses. Understanding your deductible is essential for budgeting and planning your healthcare costs. This amount varies significantly depending on the specific plan and the insurer.

Choosing a health insurance plan with a lower deductible can seem appealing, but it often comes with higher monthly premiums. Conversely, a higher deductible might mean lower monthly premiums but increased out-of-pocket expenses when you need medical care. It's vital to consider your individual health needs and financial situation when making this decision.

High-Deductible Health Plans (HDHPs)

High-deductible health plans (HDHPs) are designed to offer lower monthly premiums in exchange for a higher deductible. HDHPs often pair with health savings accounts (HSAs), which can help you save money on qualified medical expenses. This combination can be a financially attractive option for those who anticipate infrequent medical needs.

HDHPs are often a good choice for individuals who are generally healthy and have access to other resources for medical care.

Catastrophic Health Plans

Catastrophic health plans are designed for individuals who anticipate a high probability of needing significant medical care. These plans typically have very high deductibles, but they provide comprehensive coverage once the deductible is met. A catastrophic plan can be a good option for people with pre-existing conditions or a family history of significant health issues, ensuring they have access to necessary care even with higher upfront costs.

Preferred Provider Organizations (PPOs)

Preferred provider organizations (PPOs) often have lower deductibles compared to other plans, but they have a network of preferred providers. This means that if you utilize in-network providers, you'll often pay less out-of-pocket for care. This can be a beneficial aspect for those who prefer a wider range of providers. However, care from out-of-network providers will likely come with higher costs.

PPOs usually offer more flexibility in choosing providers, but the coverage and cost vary depending on the specific plan and provider network.

Exclusive Provider Organizations (EPOs)

Exclusive provider organizations (EPOs) have a more limited network of providers than PPOs. This limited network often translates to lower monthly premiums and lower deductibles. However, the strict adherence to the provider network may be a drawback for some individuals.

Individuals considering an EPO need to carefully examine the provider network to ensure it aligns with their healthcare needs and preferences. Care outside the network typically is not covered.

Flexible Spending Accounts (FSAs)

Flexible spending accounts (FSAs) can be used to set aside pre-tax dollars to pay for qualified medical expenses. This can significantly reduce your overall tax burden and help manage healthcare costs. FSAs are often a helpful tool for those who anticipate incurring substantial medical expenses and want to minimize their tax liability.

Other Types of Deductibles

Beyond health insurance, other types of insurance policies, such as disability or life insurance, may also have deductibles. These deductibles represent the amount you must pay out-of-pocket before the insurance company begins to cover the claim. Understanding these deductibles is crucial for managing your financial resources and ensuring preparedness for unexpected events.

Understanding the various types and nuances of deductibles is essential for making informed decisions about insurance coverage and managing your healthcare expenses. Careful consideration of your individual needs and financial situation is crucial when selecting a plan.

Finding Your Deductible in Your Policy

Understanding Your Deductible

Your deductible is the amount you must pay out-of-pocket for covered medical expenses before your health insurance plan starts to pay. It's a crucial component of your health insurance policy, and understanding it is essential for effective budgeting and managing your healthcare costs. Knowing your deductible allows you to anticipate expenses and plan accordingly, preventing surprises when medical bills arrive. This upfront cost helps control healthcare costs and ensures you're financially prepared for unexpected illnesses or injuries.

Effectively managing your health insurance deductible involves careful planning. You should understand the specific dollar amount associated with your plan and how it applies to various medical services. This proactive approach will help you avoid unnecessary stress and financial strain when seeking healthcare.

Types of Deductibles

Different health insurance plans can have various deductible structures. Some plans have a single, overall deductible, while others might have separate deductibles for specific services, like preventive care or specialist visits. Understanding the specifics of your plan is key to avoiding misunderstandings and financial issues later on. It's crucial to review your policy documents thoroughly to identify the precise structure of your deductible.

It's also important to note that some plans may have a separate deductible for each family member. This means that each individual on your policy may have to meet a specific threshold before the insurance company begins to contribute towards their healthcare costs.

How Deductibles Work

Once you've met your deductible, your health insurance plan typically starts paying a portion of your covered medical expenses. This percentage varies depending on the plan and the type of service. Understanding how your deductible interacts with your plan's co-pays and coinsurance is crucial for accurate cost estimations. This knowledge helps you anticipate your total out-of-pocket expenses.

The process of meeting your deductible can be tracked using various resources, such as online portals or your insurance company's customer service. This tracking helps maintain accurate records of your expenses and ensures that you're informed about your progress towards meeting the deductible threshold.

Finding Your Deductible Information

Your deductible information is typically found in your health insurance policy documents. These documents outline the details of your plan, including the specific amount of your deductible, any applicable co-pays or coinsurance, and the specific services covered. Reviewing these documents carefully is critical for ensuring you have a thorough understanding of your coverage. Refer to your summary of benefits or your policy booklet for accurate figures.

If you are unsure where to find this information, contact your insurance provider directly. They can provide detailed information about your deductible and answer any questions you may have.

Important Considerations

When considering your deductible, factor in potential future healthcare needs and anticipated expenses. Consider whether your current health insurance policy adequately covers your anticipated medical expenses. This proactive approach will help you avoid surprises and ensure financial preparedness. The importance of understanding your health insurance deductible cannot be overstated. Planning for these costs is crucial for managing your finances and avoiding unexpected financial burdens.

Understanding your deductible empowers you to make informed decisions about your healthcare choices. This awareness allows you to prioritize preventative care and other cost-effective strategies to maintain your health.

Read more about How to Understand Your Homeowners Insurance Deductible

![Guide to Investing During Inflation [Strategies]](/static/images/30/2025-05/AdaptingYourInvestmentStrategyOverTime.jpg)

![Best Investment Platforms for Beginners [2025]](/static/images/30/2025-05/AdditionalTipsforChoosingtheRightPlatform.jpg)

![Tax Implications of Selling Cryptocurrency [2025]](/static/images/30/2025-07/BeyondtheBasics3AConsiderationsforSpecificCryptocurrencies.jpg)

![Tax Planning Tips for Homeowners [2025]](/static/images/30/2025-07/PropertyTaxDeductionsandStrategies.jpg)

Hot Recommendations

- Tax Planning Tips for Homeowners [2025]

- How to Get Insurance for a Short Term Rental Property

- Understanding the Benefits of a Roth IRA

- How to Manage Business Debt After a Downturn

- How to Use a Barbell Investment Strategy

- Best Ways to Track Your Progress Towards Financial Freedom

- Tips for Managing Credit Card Rewards While Paying Off Balances

- Tax Planning Tips for Stock Options

- How to Plan for Retirement if You Didn't Save Early

- Guide to Managing Legal Debt