Dividend Investing Strategy: Generate Passive Income

Identifying Your Desired Investment Timeline

Dividend investing rewards patience. Unlike day trading, this approach thrives on compound growth over years, not weeks. Market ups and downs will test your resolve, which is why defining your time horizon matters. Are you building retirement income or generating supplemental cash flow? Your answer shapes everything from stock selection to risk management. Clear timelines act as anchors during market storms, preventing emotional decisions that derail long-term success.

Determining Your Preferred Dividend Investment Approach

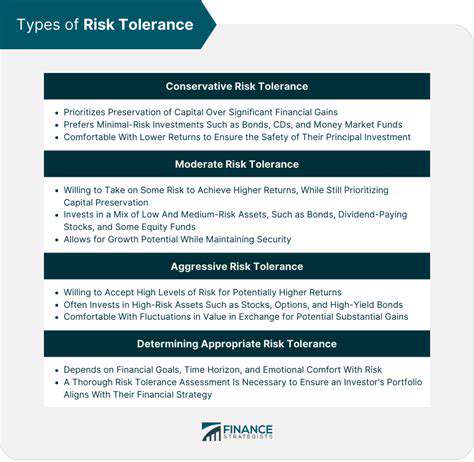

Dividend strategies vary as much as investors themselves. Some prioritize steady growers - companies that increase payouts annually like clockwork. Others seek value plays, hunting undervalued stocks with strong dividend histories. Your choice should reflect both your financial objectives and sleep-at-night comfort level. The best approach isn't what works for others, but what aligns with your personal financial DNA. Taking time to understand these different paths pays dividends in confidence and results.

Analyzing Your Investment Portfolio Diversification

Don't put all your dividend eggs in one basket. Spreading investments across sectors and company sizes creates resilience. A tech dividend stock might falter while healthcare dividends hold steady - that's diversification at work. Regular portfolio checkups help spot overconcentration before it becomes problematic. This disciplined approach smooths out market bumps and provides more consistent income streams, making your dividend journey less stressful and more productive.

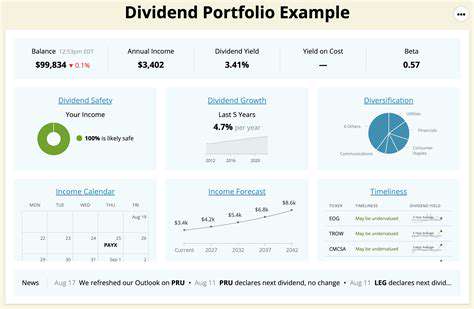

Building a Diversified Dividend Portfolio

Understanding Dividend Investing

At its core, dividend investing focuses on stocks that share profits regularly with shareholders. This strategy appeals to those seeking predictable income and protection against inflation's eroding effects. The magic happens when patience meets compounding - reinvested dividends buying more shares, which generate more dividends, creating a virtuous cycle over time.

Identifying Dividend-Paying Stocks

Quality matters more than quantity when selecting dividend payers. Look beyond the yield percentage to examine financial statements for signs of strength: manageable debt, consistent earnings, and cash flow that comfortably covers dividend obligations. The payout ratio (dividends as a percentage of earnings) acts as a financial health check - ratios above 100% signal potential trouble ahead. Companies that pay dividends like clockwork through economic cycles often make the steadiest long-term holdings.

Assessing Dividend Growth Potential

Dividend growth separates good investments from great ones. Track records matter - companies that consistently raise payouts demonstrate financial discipline and confidence in future earnings. But don't just look backward. Evaluate whether industry trends, competitive advantages, and management strategies support continued growth. A 3% yielder growing at 10% annually soon outpaces a static 5% yield - that's the power of compounding growth.

Portfolio Diversification Strategies

Smart diversification goes beyond owning different stocks. It means balancing across sectors (utilities, healthcare, tech), market caps (large, mid, small), and even geography. This layered approach cushions against sector-specific downturns. Think of your portfolio as a symphony - when some instruments soften, others carry the melody, creating harmonious returns over time.

Managing Dividend Portfolio Risk

Even safe dividend stocks carry risk. Economic shifts can pressure payouts, and company-specific issues can arise unexpectedly. Mitigate these risks through ongoing research, position sizing (avoiding overconcentration in any single holding), and maintaining some liquidity to seize opportunities during market dips. Regular portfolio reviews act like financial check-ups, catching potential problems before they become serious.

Strategies for Long-Term Dividend Growth

Successful dividend investing requires both discipline and flexibility. Stick to your strategy during market swings, but remain open to adjusting holdings as companies or economic conditions change. The most successful dividend investors think like business owners, focusing on underlying company health rather than daily price movements. This long-view approach, combined with reinvestment and patience, builds remarkable wealth over decades.

Nutrition plays an underappreciated role in managing financial stress. Just as a balanced diet supports physical health, proper nourishment aids mental clarity for making sound investment decisions. Certain nutrients help regulate stress hormones, creating a calmer mindset for evaluating opportunities and risks.

Tax Implications and Strategies

Understanding Tax Deductions

Smart investors treat tax deductions as financial tools, not just annual paperwork. From investment expenses to charitable giving, deductions lower taxable income dollar-for-dollar. Organization separates tax-savvy investors from the rest - maintain clear records throughout the year rather than scrambling at tax time. When in doubt, consult a professional; the fee often pays for itself in uncovered deductions and avoided errors.

Strategic Tax Planning for Individuals

Proactive tax planning transforms April from a stressful event into just another month. Timing matters as much as amount - sometimes delaying income or accelerating deductions creates significant savings. Investment choices carry tax consequences that compound over years; understanding these nuances helps keep more money working for you rather than funding government coffers. Major life events - marriages, home purchases, career changes - all present tax planning opportunities for the prepared investor.

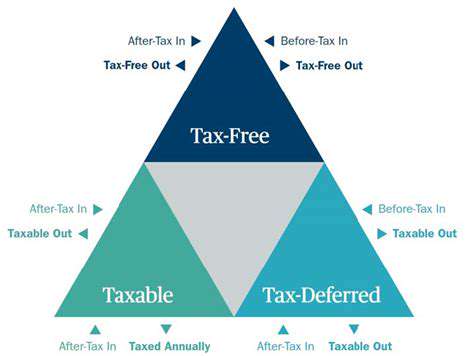

Tax-Efficient Investment Strategies

Location matters in investing - not just geographic, but account type. Tax-advantaged accounts (401(k)s, IRAs) serve as financial greenhouses, sheltering growth from immediate taxation. Asset placement strategy - holding tax-inefficient investments in sheltered accounts - can significantly boost after-tax returns over decades. Understanding capital gains rates and holding periods helps time sales advantageously. Tax-loss harvesting turns market downturns into silver linings by offsetting gains elsewhere. These strategies, woven together, form a tax-efficient tapestry that preserves more wealth over time.

Read more about Dividend Investing Strategy: Generate Passive Income

![Budgeting for College Students [Money Management]](/static/images/30/2025-05/UtilizingBudgetingToolsandApps3AStreamliningYourFinances.jpg)

![Budgeting for a Wedding [Tips & Breakdown]](/static/images/30/2025-06/NegotiatingandSeekingAffordableAlternatives.jpg)