Guide to Understanding Annuities in Retirement

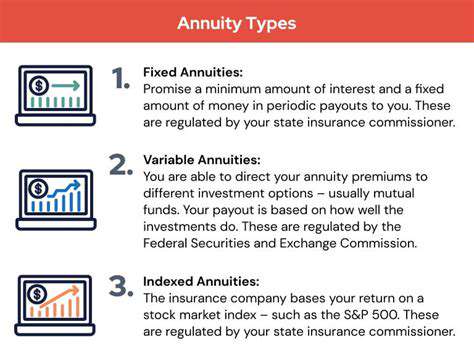

Fixed Annuities

Fixed annuities are a popular type of annuity that offers a guaranteed rate of return. This guaranteed return is typically based on a specific interest rate, often set at the time of purchase. The interest rate can fluctuate, but it's usually capped by the issuer. This predictable return can be attractive to investors seeking stability and a known income stream in retirement. Crucially, the value of your investment is protected from market downturns, providing peace of mind. A fixed annuity can be a good choice for those seeking a consistent income stream in retirement. It's a straightforward way to save and accumulate funds.

A key feature of fixed annuities is the predictable, often guaranteed, rate of return. This predictability makes them suitable for investors who prioritize security and stability. Understanding the specific terms and conditions of a fixed annuity is crucial, as they vary between providers and investment options. This includes any fees or charges associated with the annuity, as well as the interest rate and its potential fluctuation. Comparing different fixed annuity options is essential to finding the best fit for your financial goals.

Variable Annuities

Variable annuities, unlike fixed annuities, offer the potential for higher returns based on the performance of underlying investments, such as stocks or mutual funds. This exposure to market fluctuations also carries the risk of losing principal. Understanding the investment risk involved with these products is crucial before making a decision. Variable annuities often include a range of investment options, allowing investors to tailor their investment strategy. This flexibility can be attractive to those who want to potentially earn higher returns, but it also means more responsibility in managing investment choices.

Diversification and risk tolerance are important considerations when selecting investments within a variable annuity. The choice of investments significantly impacts the potential returns, but also the associated risk. Carefully reviewing the fund options and understanding the associated fees and expenses is essential. It's a key difference from fixed annuities, where returns are generally guaranteed, and it's vital to thoroughly understand the nuances before investing.

Variable annuities are suited for investors who are willing to take on more investment risk in pursuit of potentially higher returns. They might be a good fit for those seeking a higher growth potential or who are comfortable with market fluctuations.

Other Annuity Types

Beyond fixed and variable annuities, other types of annuities exist, often incorporating elements of both. For example, some annuities offer a combination of guaranteed and variable returns, balancing security with the chance of higher growth. These hybrid options aim to provide a blend of stability and potential upside. It's important to carefully review the specific features and components of any annuity to evaluate its suitability for your situation.

Understanding the different types of annuities allows investors to make informed decisions that align with their risk tolerance and financial goals. This is particularly important when considering long-term financial planning, as annuities play a significant role in securing a comfortable retirement. Due diligence and thorough research are necessary to find an annuity that best serves your needs. Annuities are complex financial products, and consulting a financial advisor is highly recommended to discuss the advantages and disadvantages of each type.

Indexed annuities, for example, link returns to specific market indexes. These often offer a measure of protection against market downturns while still allowing for potential participation in market upside. It's essential to thoroughly evaluate the specific provisions of any indexed annuity.

Key Considerations When Choosing an Annuity

Understanding Your Needs

Before diving into the specifics of different options, it's crucial to clearly define your requirements. What are you trying to achieve? Are you looking for a solution that's aesthetically pleasing, highly functional, or perhaps something that balances both? Understanding your specific needs will help you narrow down your choices and avoid purchasing something that doesn't truly meet your expectations. A comprehensive understanding of your needs is the foundation upon which any successful decision is built.

Consider the scale of your project or task. A simple solution might suffice for a small-scale project, while a more complex solution may be necessary for a large-scale endeavor. Thoroughly evaluating your needs will help you avoid overspending on unnecessary features or underestimating the resources required for a successful outcome.

Budget Constraints

Financial limitations are often a significant factor in decision-making. Creating a realistic budget is essential to avoid overspending and ensure that you're making financially sound choices. Careful consideration of your budget will ensure you don't compromise your financial stability in the pursuit of a solution. Set a clear budget limit, and stick to it as closely as possible. Explore different options within your budget to find the best possible fit.

Investigating various options and comparing their prices can help you to stay within your budget. Look for solutions that offer value for money. This may involve exploring different pricing tiers or considering alternative solutions that offer similar features at a lower cost.

Time Constraints

Time is a precious commodity, and selecting the right option should consider the time available for implementation. A faster solution might be preferred over a more comprehensive one if time is a critical factor. Understanding the time constraints of your project is vital for selecting an appropriate solution. Consider the time needed to learn the new solution, implement it, and achieve the desired outcome.

Thoroughly evaluating the time commitment associated with different solutions is vital for project success. A suitable solution should not add undue stress to your timeline and should instead contribute to a smooth and efficient workflow.

Functionality and Features

The specific functionalities and features required will significantly influence your decision. Ensure the selected option meets all your functional requirements. Prioritize features that are essential to your workflow and productivity. Consider features that could enhance your existing processes and make them more efficient.

Think about how the chosen solution will integrate with your existing systems and workflows. A smooth integration is crucial for avoiding disruption and ensuring a seamless transition.

Scalability and Flexibility

Consider the potential future growth and changes in your requirements. Choose a solution that can adapt to your evolving needs. A scalable solution will allow you to expand your operations without significant adjustments or complications. A flexible solution can accommodate future changes in your requirements without requiring a complete overhaul.

Evaluate the solution's adaptability to changing circumstances. A solution that can grow with your needs will save you time and resources in the long run.

Reliability and Support

The reliability of the chosen option is paramount. Consider the provider's reputation, support options, and track record of reliability. A reliable solution will minimize disruptions and ensure consistent performance. Look for a solution backed by strong support documentation and responsive customer support teams. This ensures that you have access to help and assistance when needed.

Investigate the support options available for the selected solution. This includes documentation, FAQs, and contact information for customer support. A robust support system will provide assistance when you encounter difficulties, ensuring a smooth user experience.

Annuities and Tax Implications

Understanding Annuity Types and Tax Treatment

Annuities are complex financial products, and understanding their various types is crucial for making informed decisions. Different annuity types, such as immediate annuities, deferred annuities, and variable annuities, have distinct tax implications. Immediate annuities, for example, often have a portion of the payments taxed as ordinary income, while deferred annuities typically defer taxes until withdrawals are made. It's vital to carefully consider the tax ramifications of each type when planning your retirement income strategy.

Variable annuities, in particular, can involve more complex tax situations due to the investment options available. Understanding how investment gains and losses are taxed, along with the potential for capital gains taxes, is essential to accurately project your long-term tax burden. Proper tax planning is a key component of successful annuity management.

Federal Income Tax Implications of Annuity Distributions

Upon distribution, annuity payments are typically taxed. The portion of each payment representing the return of your principal (the amount you paid into the annuity) is typically tax-free. However, any portion exceeding the principal is taxed as ordinary income. This means you'll need to carefully track your contributions and withdrawals to accurately calculate the taxable portion of your annuity distributions.

State Taxes and Annuities

State tax implications for annuities can vary significantly. Some states may impose additional taxes on annuity distributions, while others may not. This variability can significantly affect your overall tax burden. Consulting with a qualified tax advisor is highly recommended to understand the specific tax regulations in your state and how they impact your annuity.

Knowing the state tax laws related to annuities is crucial for accurate financial planning. This knowledge helps you anticipate the total tax burden and adjust your retirement income strategy accordingly.

Impact of Annuity Choice on Retirement Income

The choice of annuity significantly impacts your retirement income stream. An immediate annuity provides a fixed income stream right away, while a deferred annuity allows for potentially higher returns over time. Understanding the trade-offs between immediate and deferred annuities is crucial for aligning your annuity choice with your specific retirement income needs.

Potential Tax Deductions and Credits Related to Annuities

In some cases, contributions to certain annuity types may qualify for tax deductions or credits. This can result in a reduction in your taxable income. However, the specific requirements for these deductions and credits vary by annuity type and individual circumstances. Careful consideration of these potential tax benefits is important, but it's crucial to consult with a qualified financial advisor to determine if you qualify for specific deductions or credits.

Long-Term Tax Planning with Annuities

Long-term tax planning is essential when considering annuities. Understanding how annuity payments will be taxed over your entire retirement period is vital for effective financial management. This involves projecting future tax rates and considering potential changes in tax laws that could impact your annuity income. Thorough long-term planning is critical to ensure your retirement income aligns with your financial goals and tax obligations.

Annuities vs. Other Retirement Options

Understanding Annuities

Annuities are a type of contract offered by insurance companies that provide a stream of payments over time. They function as a way to convert a lump sum of money into a regular income stream, often used in retirement planning. A key feature of annuities is the potential for guaranteed income for life, offering a degree of financial security in retirement.

Annuities can be a valuable tool for retirees seeking predictable income streams. They generally provide a consistent payout, helping to offset potential market fluctuations. This stability can be particularly appealing to those who prefer a predictable income stream in retirement.

Exploring Alternative Retirement Options

There are various approaches to retirement planning beyond annuities. Individual Retirement Accounts (IRAs) and 401(k) plans are popular options that allow individuals to save and invest for retirement. These accounts often offer tax advantages, helping to maximize retirement savings.

Investment portfolios, constructed carefully and with professional guidance, can also be effective retirement strategies. They allow for diversification and the potential for higher returns, but carry a higher level of risk compared to annuities.

Annuities and Tax Implications

The tax implications of annuities can vary depending on the specific type of annuity and the payout schedule. Understanding how these taxes impact your income stream is crucial in your financial planning.

Depending on the type of annuity, there might be tax advantages or disadvantages. It's essential to consult with a financial advisor to understand the specific tax implications of different annuity options.

Comparing Annuity Types

Various types of annuities exist, each with its own characteristics and features. Understanding these differences is vital for choosing the right annuity that aligns with your individual retirement needs. Different annuity types include fixed, variable, and indexed annuities.

Each type has its own set of advantages and disadvantages, and it's crucial to carefully analyze these before making a decision. The choice of annuity type will depend on your investment goals, risk tolerance, and desired income stream.

Risk Assessment in Retirement Planning

Retirement planning involves assessing risk tolerance. Different investment strategies carry varying degrees of risk. Annuities, for example, often offer a more secure income stream, but potentially lower growth potential compared to other investment options.

Understanding your risk tolerance is crucial in selecting the appropriate retirement plan. It is essential to consider your individual circumstances and financial objectives when making such a decision.

Seeking Professional Financial Advice

Navigating the complexities of retirement planning, including the comparison of annuities with other options, can be challenging. Seeking professional financial advice is highly recommended.

A qualified financial advisor can provide personalized guidance, helping you make informed decisions about your retirement savings and investments. They can help you weigh the pros and cons of annuities versus other retirement options, ultimately tailoring a strategy that aligns with your specific needs and goals.

Read more about Guide to Understanding Annuities in Retirement

Hot Recommendations

- Tax Planning Tips for Homeowners [2025]

- How to Get Insurance for a Short Term Rental Property

- Understanding the Benefits of a Roth IRA

- How to Manage Business Debt After a Downturn

- How to Use a Barbell Investment Strategy

- Best Ways to Track Your Progress Towards Financial Freedom

- Tips for Managing Credit Card Rewards While Paying Off Balances

- Tax Planning Tips for Stock Options

- How to Plan for Retirement if You Didn't Save Early

- Guide to Managing Legal Debt