Guide to Understanding Bonds as an Investment

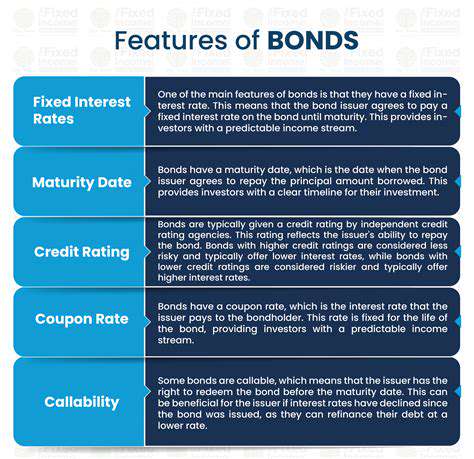

Key Features of Bonds

Several distinctive attributes set bonds apart from equities or other securities. The maturity timeline represents perhaps the most critical consideration, as it directly impacts both risk exposure and liquidity. Independent rating agencies like Moody's or S&P evaluate creditworthiness through letter grades (AAA to D), which savvy investors scrutinize before committing funds. The coupon rate—locked in at issuance—determines the fixed interest percentage paid to bondholders, though market fluctuations later affect the bond's trading price.

The Role of Bonds in the Financial Market

Fixed-income securities serve as the backbone of global capital markets. Governments utilize them to fund infrastructure without raising taxes, while corporations access growth capital beyond bank financing limits. For investors, bonds provide portfolio ballast during stock market turbulence through their inverse price-yield relationship. The $130 trillion global bond market's sheer size means its interest rate movements ripple across mortgages, business loans, and even currency valuations.

Types of Bonds and Their Characteristics

The bond universe contains specialized instruments catering to diverse needs. U.S. Treasuries (T-bills, notes, bonds) form the risk-free benchmark with full government backing. Corporate debt spans investment-grade blue chips to high-yield junk bonds from growth companies. Municipal bonds (munis) offer federal tax exemptions, particularly valuable for high-income investors. Selecting appropriate bond types requires matching an investor's tax bracket, risk appetite, and income needs with instrument specifics, as default rates and tax treatments vary dramatically across categories.

Bond Pricing and Yields

Secondary market pricing follows complex calculus incorporating current interest rates, time remaining until maturity, and perceived issuer stability. When central banks hike rates, existing fixed-coupon bonds immediately lose appeal, depressing their market value. Seasoned investors track yield-to-maturity (YTM) rather than coupon rates, as YTM accounts for both interest payments and any capital gains/losses if holding to maturity. Sophisticated traders also monitor yield curve shapes (normal, flat, inverted) for recession signals.

Types of Bonds: Exploring the Diverse Landscape

Types of Covalent Bonds

At the atomic level, covalent bonding occurs through electron sharing between atoms, enabling both participants to achieve stable electron configurations. This fundamental interaction literally builds our material world, from water molecules to DNA strands. Bond strength depends on shared electron quantity and the electronegativity gap—minor differences create polar bonds (like H₂O), while equal sharing forms nonpolar bonds (like O₂). Single bonds (one shared pair) allow rotation, whereas double/triple bonds create rigid molecular geometries critical for biological functions.

Advanced variations include coordinate covalent bonds where one atom donates both electrons, common in metal complexes. Resonance structures, seen in benzene rings, demonstrate delocalized electrons that enhance stability. These nuances explain why diamonds (strong 3D covalent network) outperform graphite (layered covalent bonds) in hardness, despite both being pure carbon. Biochemists particularly value disulfide covalent bonds between cysteine amino acids that stabilize protein structures.

Ionic Bonds and Metallic Bonds

Ionic compounds form through complete electron transfers, creating charged ions with electrostatic attraction. Table salt (NaCl) exemplifies this—sodium donates an electron to chlorine, generating Na⁺ and Cl⁻ ions that crystallize into a cubic lattice. These bonds dissociate in water, enabling electrolyte functions crucial for nerve signaling and hydration. Lattice energy measurements reveal why magnesium oxide (MgO) withstands higher temperatures than sodium chloride due to stronger ionic attraction.

Metals utilize a unique electron sea model where valence electrons detach from atomic cores, creating a mobile charge cloud. This explains copper's exceptional conductivity—applying voltage sends delocalized electrons flowing instantly. Metallic bonding's flexibility allows gold to be hammered into thin leaf without fracturing, while alloying (mixing metals) can enhance desired properties like steel's strength from iron-carbon mixtures. Shape-memory alloys like Nitinol demonstrate metallic bonding's remarkable capacity for reversible deformation.

Though weaker than covalent/ionic bonds, hydrogen bonds (H-bonding) dictate water's unusual properties—its high boiling point, surface tension, and ice density anomaly all stem from H₂O molecules' ability to form transient bridges via hydrogen atoms. DNA's double helix maintains integrity through H-bonds between base pairs (A-T, C-G), allowing precise replication during cell division.

Bond Yields and Risk: Balancing Reward and Safety

Understanding Bond Yields

Yield analysis separates successful bond investors from casual participants. Current yield (annual interest divided by price) provides a snapshot, while yield-to-maturity (YTM) calculates total projected return including principal repayment. During the 2020 market turmoil, savvy traders identified mispriced corporate bonds with YTMs exceeding 8%—later generating 30%+ returns as markets stabilized. Yield curves convey macroeconomic expectations; an inverted curve (short rates > long rates) famously preceded 7 of the last 8 recessions.

Specialized yields like yield-to-worst (YTW) help assess callable bonds by calculating returns under least favorable call scenarios. Municipal bond investors focus on tax-equivalent yield (TEY) to compare taxable vs. tax-exempt options. For example, a 4% muni yield equals 6.15% taxable yield for someone in the 35% bracket (4%/(1-0.35)). These metrics enable apples-to-apples comparisons across bond types.

Assessing Bond Risk

Interest rate risk manifests through duration—a bond's price sensitivity to rate changes. A 5-year duration means a 1% rate hike could cause a ~5% price drop. In 2022, long-duration Treasuries lost 15%+ as the Fed aggressively raised rates. Credit risk varies exponentially: investment-grade corporates (BBB- or higher) default <0.5% historically, while CCC-rated bonds fail ~15% of the time. The 2008 crisis showed even AAA mortgage-backed securities can collapse when underlying loan quality deteriorates.

Liquidity risk became acute during March 2020's dash for cash when even Treasury markets required Federal Reserve intervention. Emerging market bonds often trade with 2-3% bid-ask spreads versus 0.1% for U.S. Treasuries. Event risk—like LBOs triggering bond downgrades—requires monitoring issuer news. Inflation risk particularly erodes long-term fixed payments; 30-year Treasuries lost 40% real value during 1977-1981's high inflation.

Balancing Reward and Safety

Modern portfolio theory suggests mixing high-yield and government bonds—the former boosts returns while the latter provides crisis protection. During the 2008 meltdown, high-yield spreads over Treasuries peaked at 20%, creating generational buying opportunities. Laddering maturities (equal allocations to bonds maturing 1-10 years out) smooths reinvestment risk. Some investors overweight short-duration bonds when expecting rate hikes, then extend duration during easing cycles.

Active managers analyze covenant quality (bondholder protections), sector trends, and macroeconomic indicators. The 2021 Archegos collapse demonstrated how even safe investment-grade bonds can crash without proper collateral coverage analysis. Defensive strategies include maintaining cash reserves to purchase discounted bonds during market dislocations—Warren Buffett famously did this during the 2008 financial crisis with Goldman Sachs bonds yielding 10%.

Investing in Bonds: Strategies and Considerations

Strategies for Bond Investing

Successful bond investing requires adapting to market phases. In rising rate environments, floating-rate notes (FRNs) and short-duration bonds outperform. When recession looms, high-quality long bonds appreciate as rates fall. Barbell strategies—combining short-term and long-term bonds while avoiding intermediates—capture yield advantages while maintaining flexibility. Contrarian investors sometimes reach for yield in oversold sectors, like energy bonds during 2020's oil price crash that subsequently rebounded 80%.

Sophisticated approaches include yield curve positioning (e.g., riding the curve by buying 5-year notes expected to become 4-years as time passes). Some hedge funds employ capital structure arbitrage—shorting a company's equity while buying its undervalued bonds. Individual investors can replicate some institutional strategies through bond ETFs targeting specific durations, credit qualities, or sectors.

Considerations for Bond Investors

Tax positioning dramatically affects net returns. High-bracket investors in high-tax states might prioritize munis, while retirement accounts better hold taxable corporate bonds. Inflation expectations should guide TIPS allocations—these Treasury securities adjust principal values for CPI changes. Secondary market liquidity varies widely; newly issued on-the-run Treasuries trade actively, while older off-the-run issues may have wider spreads.

Callable bonds require extra scrutiny—issuers often call them when rates fall, forcing reinvestment at lower yields. Sinking fund provisions (required partial redemptions) can disrupt laddering strategies. Currency risk matters for global bonds; a 5% yield vanishes if the foreign currency depreciates 10%. Documentation review is critical—some bonds have unusual features like payment-in-kind (PIK) toggle options.

Execution quality impacts returns—retail investors often overpay in odd-lot markets (<100 bonds). Using limit orders and comparing dealer quotes saves basis points that compound over time. Monitoring Federal Reserve guidance provides clues about future rate paths that affect bond prices. Finally, aligning bond selections with overall asset allocation targets prevents overconcentration in any single risk factor.

Read more about Guide to Understanding Bonds as an Investment

![Best Homeowners Insurance Companies [2025 Review]](/static/images/30/2025-05/TopTierHomeownersInsuranceProvidersin2025.jpg)

![Best Tools for Debt Management [2025]](/static/images/30/2025-05/DebtManagementPlans28DMPs293APersonalizedStrategiesforRepayment.jpg)