Budgeting for Couples: Tips for Managing Money Together

Developing a Realistic Savings Plan and Managing Debt

Understanding Your Financial Situation

Before crafting a savings strategy, take time to thoroughly assess your current financial standing. Tracking every dollar coming in and going out over a full month reveals spending patterns you might not notice otherwise. This financial snapshot exposes potential leaks in your budget - those recurring subscriptions you never use or that daily coffee habit that adds up faster than you'd think.

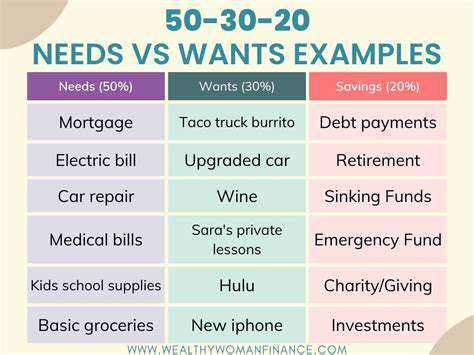

Divide expenditures into two clear buckets: necessities (like rent and groceries) and discretionary spending (such as entertainment). This simple sorting exercise often shocks couples when they see how much small purchases accumulate over time. The clarity gained here becomes the foundation for meaningful financial changes.

Creating a Joint Budget

Money conversations can feel uncomfortable, but developing a shared financial plan transforms anxiety into teamwork. When partners combine their financial perspectives, they create something greater than individual efforts - a unified approach to building security. The process itself strengthens relationships through honest dialogue about values and priorities.

Schedule regular money dates to review your joint budget. These check-ins prevent small misunderstandings from becoming major conflicts. Pro tip: Always begin these conversations by reaffirming shared goals - it keeps discussions solution-focused rather than confrontational.

Setting Realistic Savings Goals

Financial progress happens in increments, not overnight. Rather than drastic cuts that never stick, try the 5% rule - reduce one budget category by just 5% each month. This gentle approach builds lasting habits without deprivation. Celebrate small victories - that first $500 saved or a paid-off credit card - to maintain motivation.

Consider implementing the 24-hour rule for non-essential purchases. Waiting a day before buying often reveals whether an item is truly important or just an impulse. This simple pause can save hundreds monthly.

Prioritizing Debt Repayment

High-interest debt acts like financial quicksand - the harder you struggle, the deeper it pulls you down. The avalanche method delivers the fastest results: list debts by interest rate and attack the highest first while making minimum payments on others. Watching that top debt disappear creates powerful momentum.

For visual learners, create a debt thermometer chart. Coloring in each percentage paid off provides satisfying, visible progress that spreadsheets can't match. This psychological boost helps maintain repayment discipline during challenging months.

Utilizing Budgeting Tools and Resources

Modern budgeting apps offer features our grandparents never imagined - automatic categorization, spending alerts, and even predictive analysis. But don't let technology overwhelm you. The most effective tool is the one you'll actually use consistently, whether that's a sophisticated app or a simple notebook.

When selecting financial tools, prioritize those offering joint access for couples. Shared visibility prevents financial infidelity - those small, secret purchases that can erode trust. Transparency builds stronger relationships along with healthier bank balances.

For complex situations, a certified financial planner provides more than advice - they offer accountability. Their neutral perspective often spots opportunities and risks that emotionally involved partners might miss. Think of them as financial translators helping couples speak the same money language.

Read more about Budgeting for Couples: Tips for Managing Money Together

![Best Debt Management Plans [2025 Review]](/static/images/30/2025-05/NavigatingtheApplicationProcessandOngoingManagement.jpg)

![Best Renters Insurance Companies [2025 Review]](/static/images/30/2025-05/CompanyB3AExcellentCustomerService26ClaimsHandling.jpg)

Hot Recommendations

- Tax Planning Tips for Homeowners [2025]

- How to Get Insurance for a Short Term Rental Property

- Understanding the Benefits of a Roth IRA

- How to Manage Business Debt After a Downturn

- How to Use a Barbell Investment Strategy

- Best Ways to Track Your Progress Towards Financial Freedom

- Tips for Managing Credit Card Rewards While Paying Off Balances

- Tax Planning Tips for Stock Options

- How to Plan for Retirement if You Didn't Save Early

- Guide to Managing Legal Debt