How to Choose Your First Stock

Understanding Your Investment Goals

Before jumping into stocks, take time to clarify your investment objectives. Are you chasing quick profits or building wealth gradually? Your timeline - whether months or decades - dramatically impacts which stocks make sense. Clear financial targets like saving for a home, college tuition, or retirement create the framework for smart stock choices. Without defined goals, you're just gambling.

Know your risk comfort zone. Some stocks swing wildly while others move steadily. If market ups and downs keep you awake, established blue-chip companies might suit you better. But if you can stomach volatility, emerging companies offer growth potential (and higher risk). Honest self-assessment prevents panic selling when markets get rough.

Researching Potential Stocks

Dig deep before buying. Focus on industries you actually understand - passion fuels better research. While household names seem safe, don't overlook promising smaller players. Financial statements tell the real story - balance sheets reveal debt levels while income statements show profitability. Study competitors to gauge long-term potential. Industry reports and news provide context, but think critically about analyst opinions.

Track records matter. Look for consistent revenue growth, profit margins, and dividend history (if applicable). Evaluate leadership - experienced management teams often navigate challenges better. Consider innovation pipelines, customer loyalty, and brand strength. Past performance doesn't guarantee future results, but patterns reveal resilience.

Evaluating Financial Performance

Numbers don't lie. Key metrics like EPS (earnings per share) show profitability, while P/E (price-to-earnings) ratios hint at valuation. Debt levels and cash flow expose financial health - too much debt strangles growth during tough times. Always review trends over multiple quarters, not just snapshots. One great quarter might be a fluke; consistent performance builds confidence.

Revenue tells half the story - expense management completes it. Are sales growing while costs stay controlled? Sudden changes in either direction warrant investigation. Financial statements are your X-ray vision - they reveal the bones of a business that glossy ads hide. Learn to read them well.

Considering Your Portfolio Diversification

Don't bet everything on one horse. Even your first stock should fit within a broader diversification plan across sectors. Spreading risk protects against single-company disasters. New investors often benefit from professional advice on balancing their portfolio. Different industries rise and fall at different times - diversification smooths the ride.

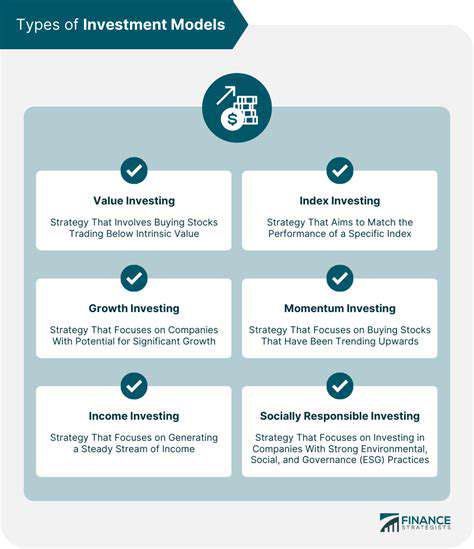

Explore investment philosophies like value hunting (undervalued stocks), growth chasing (rapidly expanding companies), or dividend collecting (steady income payers). Your strategy should match both your goals and sleep-at-night risk level. There's no universal best approach - just what works for your situation.

Identifying Your Investment Goals and Risk Tolerance

Understanding Your Financial Situation

Financial awareness precedes smart investing. Catalog your income, necessary expenses, debts, and existing savings. You can't invest what you don't have - a realistic budget shows how much you can safely allocate to stocks without jeopardizing daily needs. Emergency funds come before brokerage accounts.

Financial clarity prevents desperate moves. Knowing your net worth (assets minus liabilities) and cash flow patterns helps set appropriate investment amounts. This foundation supports all subsequent decisions about risk levels and time horizons.

Defining Your Investment Time Horizon

Money needed soon belongs in safer places. Stocks fluctuate - you don't want to sell during a dip because junior needs tuition next month. Time is your greatest ally or worst enemy. Long-term investors can ride out volatility; short-term needs demand stability.

Match investments to life milestones. Retirement decades away? Growth stocks make sense. House down payment in three years? Safer options protect your principal. Calendar-checking prevents painful mismatches between investment volatility and withdrawal needs.

Identifying Your Risk Tolerance

Be brutally honest about your stomach for losses. Would a 20% portfolio drop make you sell everything? Risk tolerance combines financial capacity and emotional resilience. Young investors can often take more risk (time heals losses), but not if they'll panic-sell.

Your risk profile should reflect both numbers and nerves. High-risk investments promise higher potential returns but guarantee sleepless nights during downturns. There's no shame in preferring steady growth over rollercoaster rides.

Establishing Your Financial Goals

Vague aspirations produce weak results. Instead of save more, try accumulate $15,000 for a car down payment in 18 months. Specific targets create accountability and measurable progress. Each goal deserves its own investment strategy based on amount, urgency, and importance.

Written goals transform daydreams into plans. Post them visibly - they'll motivate you to skip impulse buys and stay invested during market dips. Connect each investment to a concrete purpose.

Considering Your Investment Objectives

Objectives bridge goals and actions. Preserve capital leads to different choices than maximize growth. Your objectives should reflect both your targets and your timeline. Retirement accounts might emphasize growth early on, shifting toward income as retirement nears.

Clear objectives prevent contradictory moves. Chasing hot stocks while claiming to want stability reveals misalignment. Regular reviews ensure your portfolio still matches your stated purposes.

Evaluating Investment Options

With goals set, explore tools to achieve them. Stocks offer growth potential, bonds provide stability, real estate delivers diversification. Each asset class serves different purposes - your mix should reflect your unique situation.

Diversification isn't just about different stocks - it's about different types of investments responding differently to economic conditions. A well-built portfolio weathers storms that sink single-asset strategies.

Understanding headache triggers enables better management. Common culprits include stress-induced muscle tension and poor posture habits. Chronic issues warrant medical attention, but many cases improve with lifestyle adjustments. Awareness is the first step toward relief.

Evaluating Financial Metrics: Key Indicators for Success

Understanding Key Financial Metrics

Financial metrics function like a business dashboard. They reveal operational efficiency, profitability, and warning signs. Ignoring these numbers is like driving blindfolded - you might move forward, but disaster likely awaits. Regular review spots trends before they become crises.

Different metrics illuminate different aspects. Profitability ratios show earning power, liquidity ratios measure bill-paying ability, efficiency ratios expose operational strengths/weaknesses. Holistic analysis prevents overfocusing on one area while others deteriorate. Benchmark against industry standards for context.

Profitability Ratios: Measuring Your Bottom Line

Gross margin reflects production efficiency - how much markup exists after direct costs. Shrinking margins signal pricing pressure or cost creep. Net profit margin tells the ultimate truth - after ALL expenses, what percentage remains? Single-digit margins leave little room for error.

Margin trends matter more than single readings. Seasonal businesses expect fluctuations, but consistent erosion demands action. Compare your metrics to competitors' - significant gaps indicate strategic advantages or vulnerabilities.

Liquidity Ratios: Assessing Your Short-Term Financial Health

The current ratio tests survival ability - could you cover next year's bills with existing assets? Too low risks insolvency; too high suggests idle resources. The quick ratio (excluding inventory) matters most for businesses with slow-moving stock.

Liquidity management balances safety and growth. Excess cash could earn returns elsewhere, while insufficient reserves invite disaster. Economic uncertainty warrants higher liquidity buffers.

Efficiency Ratios: Optimizing Resource Utilization

Inventory turnover measures how quickly products sell. High turnover suggests strong demand or lean operations; low turnover indicates overstocking or weak sales. Accounts receivable days reveal customer payment speed - lengthening periods may signal financial stress among buyers.

Efficiency gains directly boost profitability. Reducing inventory holding costs or accelerating collections improves cash flow without requiring more sales. These metrics spotlight operational improvement opportunities.

Read more about How to Choose Your First Stock

![Best Tools for Debt Management [2025]](/static/images/30/2025-05/DebtManagementPlans28DMPs293APersonalizedStrategiesforRepayment.jpg)

Hot Recommendations

- Tax Planning Tips for Homeowners [2025]

- How to Get Insurance for a Short Term Rental Property

- Understanding the Benefits of a Roth IRA

- How to Manage Business Debt After a Downturn

- How to Use a Barbell Investment Strategy

- Best Ways to Track Your Progress Towards Financial Freedom

- Tips for Managing Credit Card Rewards While Paying Off Balances

- Tax Planning Tips for Stock Options

- How to Plan for Retirement if You Didn't Save Early

- Guide to Managing Legal Debt