Understanding Commercial Property Insurance

Key Components of a Commercial Property Policy

Insuring Your Building

A commercial property policy, crucial for businesses owning or leasing property, provides financial protection against unforeseen events. This coverage extends beyond just the physical structure to include essential components like fixtures, equipment, and even the land itself. Understanding the specific coverage levels and exclusions is paramount to ensure your business is adequately protected against potential losses. The policy should clearly define what is considered part of the insured property and outline the responsibilities of both the business owner and the insurance provider in the event of a claim.

Careful consideration of the building's specific features and potential vulnerabilities is essential. Factors like the building's age, construction materials, and location can significantly impact the risk assessment and premium calculation. For instance, a historic building with unique architectural elements might require specialized insurance coverage to account for potential restoration costs or damage to irreplaceable features.

Protecting Your Contents

Beyond the building itself, a comprehensive commercial property policy often covers the contents within. This includes everything from office furniture and equipment to inventory, machinery, and valuable assets. Understanding the specific limits of coverage for these contents is vital. Policyholders should carefully review the policy's definitions of 'contents' and ensure that all essential items are properly listed and valued to prevent gaps in coverage.

The policy should also address potential risks associated with the contents, such as theft, vandalism, or damage from natural disasters. It's critical to have accurate appraisals of your valuable assets to ensure adequate coverage and to avoid underinsurance issues in case of a claim.

Liability Protection

While primarily focused on property damage, a robust commercial property policy often includes liability coverage. This aspect protects the business from claims arising from injuries or damages to others that occur on the property. This coverage can include incidents involving customers, employees, or even the general public. A clear understanding of the liability limits within the policy is essential to avoid financial exposure in such situations.

Understanding the extent of liability coverage is crucial, as it can protect the business from significant financial burdens in the event of a lawsuit. The policy should outline the procedures for reporting incidents and initiating claims, ensuring swift and efficient handling of any potential legal proceedings.

Understanding Coverage Limits and Exclusions

A critical component of any insurance policy is understanding the coverage limits and exclusions. Commercial property policies often have specific limits on the amount of coverage provided for various perils. These limits should be carefully reviewed to ensure that they adequately protect the business's assets and financial interests. Failure to understand these limits can result in insufficient coverage in the event of a significant loss.

Knowing the policy's exclusions is equally important. Exclusions define situations or events not covered by the policy. This could include pre-existing damage, certain types of environmental contamination, or losses caused by specific events like war or nuclear incidents. The policy document should be reviewed thoroughly to identify any potential gaps in coverage and to address any concerns with the exclusions.

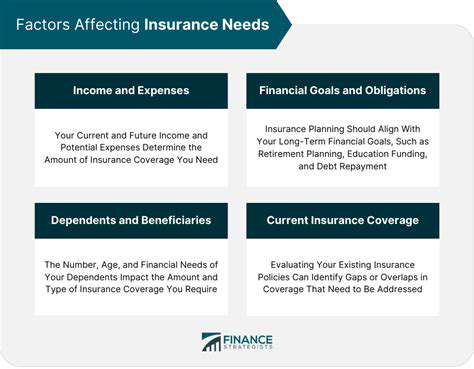

Factors Influencing Your Insurance Needs

Factors Influencing Your Insurance Premiums

Insurance premiums are influenced by a multitude of factors, creating a complex interplay that affects the cost of your policy. Understanding these factors is crucial for making informed decisions about your coverage and potentially reducing your premiums. Premiums are not static and can fluctuate based on these influences.

Your Health History

Your medical history plays a significant role in determining your insurance premiums. Pre-existing conditions, such as a history of heart disease or diabetes, can lead to higher premiums. This is because insurers assess the risk of future claims based on your past health status. Policies often adjust premiums based on the severity and frequency of past health issues.

A clean bill of health, on the other hand, usually translates to a lower premium, reflecting the lower likelihood of future claims.

Your Location

Geographical location is another key factor. Areas prone to natural disasters, such as hurricanes or earthquakes, typically have higher insurance premiums. This is a direct reflection of the increased risk of damage to property and the need for insurers to account for larger potential payouts. The risk of claims due to specific weather patterns is often factored into your local premium.

Your Driving Record

If your insurance policy covers vehicles, your driving record significantly impacts your premiums. A history of accidents or traffic violations raises your risk profile, resulting in higher premiums. Insurance companies use this information to gauge the probability of future accidents and the associated costs. A clean driving record, however, is often associated with lower premiums.

Your Coverage Choices

The specific coverage you choose also impacts your premiums. Higher coverage limits and broader coverage options often result in higher premiums. Insurance companies must factor in the potential for larger payouts if you opt for extensive coverage. By carefully considering your needs and budgeting, you can select a policy that offers adequate protection without unnecessary costs.

Your Age and Gender

Age and gender can also influence insurance premiums. Generally, younger individuals and males are often assigned higher premiums compared to older individuals and females. This is due to statistical data showing that certain demographics have a higher propensity for accidents or claims. These factors are used to calculate the average risk profile for different demographic groups. This does not mean that every individual within a demographic group will have the same risk profile.

Different Types of Commercial Property Insurance

Building Coverage

Building coverage is a fundamental aspect of commercial property insurance, safeguarding the physical structure of your business premises. This coverage typically extends to the building itself, including the roof, walls, foundation, and other structural components. It protects against a wide range of perils such as fire, windstorm, hail, vandalism, and even acts of nature. Crucially, this coverage often includes protection against business interruption, meaning you're covered for lost income if the building is damaged and you can't operate.

Understanding the specific limitations of your building coverage is critical. Ensure you understand the policy's definitions of covered perils and the deductibles involved. This will prevent costly surprises if a claim arises, and will ensure you are adequately protected against the risks you face.

Contents Coverage

Commercial property insurance also covers the contents within your building. This can include furniture, equipment, inventory, and other valuable items. The coverage amount is typically expressed as a percentage of the building's coverage, or as a separate, specified amount. Understanding the full extent of your contents coverage is crucial to ensuring that all your business assets are protected, and that you are appropriately insured for the value of those assets. A thorough inventory, and regular assessments of the value of your assets can ensure appropriate coverage and help avoid under-insurance.

Liability Coverage

Liability insurance is a critical component of any commercial property insurance policy, as it protects your business from potential lawsuits arising from incidents that occur on your property. This includes claims from customers, employees, or even the general public. Liability coverage can help mitigate the financial impact of lawsuits arising from accidents, injuries, or property damage. It's vital to understand the limits of your liability coverage and ensure it adequately addresses the potential risks associated with your business operations.

Business Interruption Coverage

Business interruption insurance is designed to compensate for lost income and expenses when your business operations are disrupted due to a covered event. This coverage can help you cover costs such as salaries, rent, utilities, and other ongoing expenses while you are unable to operate. The coverage can also include lost profits, a crucial aspect for businesses heavily reliant on uninterrupted operations. Having a clear understanding of your business interruption coverage is critical to ensuring your business can weather financial storms.

Equipment Breakdown Coverage

Certain commercial property policies may include coverage for the breakdown or failure of essential equipment. This is particularly important for businesses that rely heavily on specialized machinery or technology. The coverage often covers costs associated with repair or replacement. This type of coverage can be tailored to the specific needs of your business and the value of your equipment. Understanding the limitations and exclusions within this coverage is vital to avoid unexpected costs.

Additional Living Expenses (ALE) Coverage

In the event of a covered loss that renders your business premises uninhabitable, ALE coverage can provide financial assistance for temporary living expenses. This might include hotels, temporary rental costs, and other expenses associated with finding temporary accommodation while repairs are underway. This coverage is especially beneficial in situations where the damage is substantial and prevents you from operating from your usual location. Understanding the limits and conditions of ALE coverage is essential for ensuring you are adequately prepared for a disruption to your normal operations.

Read more about Understanding Commercial Property Insurance

![Best Retirement Income Strategies [Generating Cash Flow]](/static/images/30/2025-07/RealEstateInvestmentTrusts28REITs29forPassiveIncomeandGrowth.jpg)

Hot Recommendations

- Tax Planning Tips for Homeowners [2025]

- How to Get Insurance for a Short Term Rental Property

- Understanding the Benefits of a Roth IRA

- How to Manage Business Debt After a Downturn

- How to Use a Barbell Investment Strategy

- Best Ways to Track Your Progress Towards Financial Freedom

- Tips for Managing Credit Card Rewards While Paying Off Balances

- Tax Planning Tips for Stock Options

- How to Plan for Retirement if You Didn't Save Early

- Guide to Managing Legal Debt