How to Pay Off Debt When You Have Savings

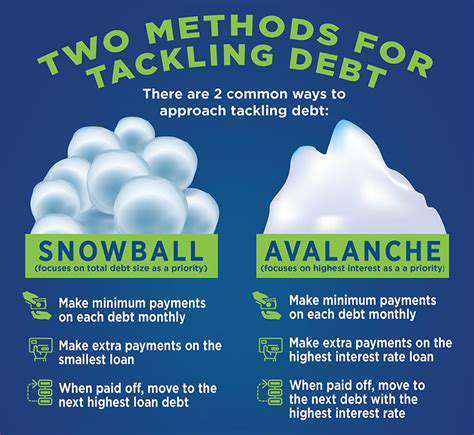

Understanding the Snowball Method

When facing multiple debts, many financial advisors recommend starting with the smallest balances first. This debt repayment approach, known as the Snowball method, creates quick wins that boost morale. There's something deeply satisfying about crossing a debt completely off your list, even if it's not the one with the highest interest rate. This psychological boost often proves more valuable than the mathematical optimization of paying highest-interest debts first.

The human brain responds better to visible progress than abstract calculations. By focusing on eliminating smaller debts first, you create tangible evidence of your financial discipline. Each paid-off account serves as motivation to tackle the next one, building momentum like a snowball rolling downhill.

Creating a List of Debts

Begin by gathering all your financial statements in one place. You'll want to document every outstanding obligation - credit cards, personal loans, medical bills - along with their current balances, minimum payments, and interest rates. Some people find color-coding their debt list helps visualize priorities.

Seeing your complete financial picture written down often reveals patterns you might miss otherwise. You might notice, for example, that three small debts could be cleared with what you're currently spending on takeout coffee. This concrete awareness makes difficult financial decisions easier to implement.

Prioritizing by Size, Not Interest Rate

Traditional financial wisdom suggests attacking high-interest debts first. However, human psychology doesn't always follow mathematical logic. The Snowball method acknowledges that motivation comes from achievement, not just interest rate calculations.

Quick wins create lasting behavioral change more effectively than perfect mathematical strategies. When you pay off that $500 medical bill, the psychological reward fuels your determination to tackle the $2,000 credit card balance next. This emotional momentum often leads to better long-term results than purely rational approaches.

Minimum Payments and Extra Payments

While focusing on your smallest debt, never neglect minimum payments on other accounts. Late payments damage credit scores and often trigger penalty rates. Think of minimum payments as the cost of maintaining good financial standing while you execute your payoff strategy.

Every extra dollar directed toward your target debt creates compound benefits. That $20 you would have spent on lunch out? Applied to your smallest debt, it becomes both a financial and psychological investment in your future. This focused approach turns small sacrifices into meaningful progress.

Tracking Progress and Staying Motivated

Financial transformation happens one payment at a time. Create a visual tracker - a chart on your fridge or an app on your phone - to mark each payment and debt elimination. Watching those numbers change makes abstract progress concrete.

Small celebrations reinforce positive financial behaviors. When you pay off that first debt, acknowledge the achievement in some meaningful way (that doesn't involve spending money). This positive reinforcement wires your brain to associate debt reduction with satisfaction rather than deprivation.

Adapting the Snowball Method

Life rarely follows a straight path, and neither should your debt repayment strategy. If an unexpected expense arises or income changes, adjust your approach without abandoning it completely. Maybe you temporarily reduce extra payments but maintain minimums.

Flexibility prevents all-or-nothing thinking that derails financial progress. The best debt strategy is the one you can sustain through life's ups and downs. Periodic reassessment ensures your method continues serving your current situation.

Combining with Other Strategies

The Snowball method works beautifully alongside other financial improvements. Maybe you use it while building an emergency fund or increasing income through side gigs. Each positive financial change amplifies the others.

Holistic financial health comes from multiple small improvements working together. As you gain control over debts, you'll naturally find more ways to optimize your finances. This snowball effect extends beyond debt into overall financial wellbeing.

Regular vet check-ups are essential for early health issue detection.

Creating a Realistic Budget and Sticking to It

Understanding Your Financial Situation

Financial clarity begins with honest assessment. For one month, track every dollar earned and spent - yes, even that $3 coffee. This exercise often reveals surprising spending patterns and opportunities. Categorize expenses to see exactly where your money goes each month.

Simultaneously, compile a complete debt inventory including balances, interest rates, and minimum payments. Seeing everything in black and white transforms abstract worries into actionable plans. This comprehensive financial snapshot becomes the foundation for meaningful change.

Developing a Realistic Budget

Effective budgets reflect reality, not wishful thinking. Start by allocating funds to necessities: housing, utilities, groceries, transportation. Then assign reasonable amounts to discretionary categories based on actual past spending (not idealized versions).

A budget you'll actually follow beats a theoretically perfect one you abandon in two weeks. Include line items for occasional expenses like car maintenance and holiday gifts. These predictable surprises derail budgets when forgotten. Building in buffers creates resilience against life's uncertainties.

Sticking to Your Budget and Making Adjustments

Treat your budget as a living document, not carved in stone. Weekly check-ins help catch overspending early, when course corrections are easier. If you consistently overspend in one category, adjust either the budget or your behavior - but be honest about which needs changing.

Financial progress comes from consistent small choices, not occasional grand gestures. Use technology to your advantage: automated savings transfers and spending alerts keep goals front-of-mind. When unexpected windfalls occur, have a plan ready (like allocating 50% to debt and 50% to savings) to prevent impulsive decisions.

Read more about How to Pay Off Debt When You Have Savings

![How to Build an Emergency Fund [Step by Step]](/static/images/30/2025-04/Step53AReplenishYourEmergencyFundWhenNecessary.jpg)

![Best Investing Books for Absolute Beginners [2025]](/static/images/30/2025-05/PracticalApplication3ABuildingYourInvestmentPlan.jpg)

![Best Car Insurance Companies in 2025 [Review]](/static/images/30/2025-05/CustomerServiceandClaimsHandling3AACrucialAspect.jpg)

Hot Recommendations

- Tax Planning Tips for Homeowners [2025]

- How to Get Insurance for a Short Term Rental Property

- Understanding the Benefits of a Roth IRA

- How to Manage Business Debt After a Downturn

- How to Use a Barbell Investment Strategy

- Best Ways to Track Your Progress Towards Financial Freedom

- Tips for Managing Credit Card Rewards While Paying Off Balances

- Tax Planning Tips for Stock Options

- How to Plan for Retirement if You Didn't Save Early

- Guide to Managing Legal Debt