Best Investment Strategies for Short Term Goals

Certificates of Deposit (CDs)

Understanding Certificates of Deposit (CDs)

When it comes to secure savings options, certificates of deposit (CDs) stand out for their reliability. Unlike standard savings accounts, CDs provide higher interest rates in exchange for locking in funds for a predetermined period, typically from a few months to several years. Think of CDs as a formal agreement with your bank, where you commit your money for a set duration in return for guaranteed returns.

The appeal of CDs lies in their predictability, but there's a trade-off. Accessing your money before the term ends usually triggers penalties, which can eat into your earnings. This makes CDs a solid choice for those with clearly defined short- or medium-term financial targets, like saving for a home renovation or a future tuition payment.

Comparing CD Rates and Terms

Not all CDs are created equal. Rates fluctuate based on the bank, deposit amount, and term length. To maximize your returns, it's wise to compare offerings from multiple institutions. Pay close attention to the interest rate, how long your money will be tied up, and any fees for early withdrawals.

Banks often provide tiered rates, meaning larger deposits or longer terms might yield better returns. Taking the time to research can lead to significantly better outcomes for your savings.

Determining Your Short-Term Goals

Before committing to a CD, clarify what you're saving for. Is it a dream vacation next summer or an emergency fund? Your specific goal will dictate whether a 6-month or 3-year CD makes more sense. Aligning the CD term with your financial timeline is crucial to avoid unnecessary penalties or missed opportunities.

Considering the Risk-Return Trade-off

CDs are among the safest investment options, with fixed returns backed by the bank. However, this safety comes at a cost - your money can't chase higher-yielding opportunities during the term. For conservative investors or those nearing a financial milestone, this stability often outweighs the potential for greater returns elsewhere.

CD Flexibility and Liquidity Considerations

While you can select terms that match your needs, CDs aren't designed for frequent access. Early withdrawal penalties can be steep, sometimes wiping out months of interest. If you anticipate needing quick access to your funds, the security of a CD might not justify the restrictions.

Understanding Penalties for Early Withdrawal

The fine print matters with CDs. Penalties for accessing your money early vary widely - some banks charge several months' interest, while others might impose a percentage of the principal. Always review the terms carefully before investing, as these details significantly impact your actual returns.

CD Alternatives and Diversification Strategies

For those who value liquidity, high-yield savings accounts or money market funds might be better options. These allow withdrawals without penalty while still offering competitive rates. A diversified approach - mixing CDs with other short-term instruments - can provide both stability and flexibility in your financial strategy.

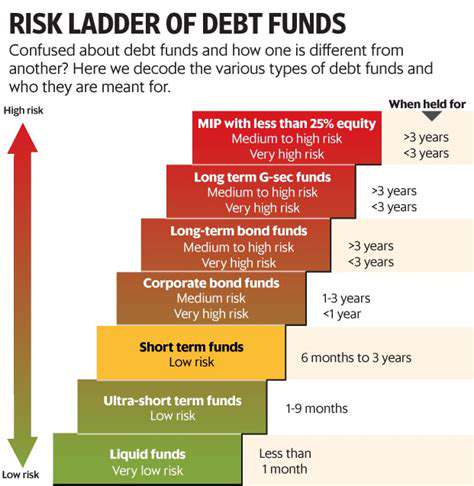

Short-Term Bonds and Bond Funds

Understanding Short-Term Bonds

Short-term bonds represent loans to governments or corporations that mature within one to three years. Their shorter duration makes them less vulnerable to interest rate swings than longer-term bonds, providing a cushion during volatile markets. This stability, combined with regular interest payments, makes them attractive for conservative investors or those with imminent cash needs.

The relative safety and liquidity of short-term bonds have made them a cornerstone of many investment strategies. They serve as parking spots for funds between other investments or as defensive positions in uncertain economic climates.

Bond Fund Basics

Bond funds democratize access to fixed-income markets by pooling investor money to buy diversified bond portfolios. This approach spreads risk across multiple issuers and maturities, something individual investors would struggle to achieve on their own. The professional management of these funds can be particularly valuable during market shifts, though investors should be mindful of management fees.

Interest Rate Sensitivity

The limited duration of short-term bonds acts as a natural hedge against interest rate risk. When rates rise, the impact on short-term bond prices is typically modest compared to their long-term counterparts. This characteristic makes them particularly appealing during periods when rate hikes are anticipated.

Maturity and Liquidity

Short maturities mean these bonds can be quickly converted to cash, either through natural maturation or secondary market sales. This liquidity is invaluable for investors who might need to reallocate funds or respond to unexpected expenses.

Risks Associated with Short-Term Bonds

While safer than many investments, short-term bonds aren't risk-free. Economic crises or issuer defaults can still lead to losses. Scrutinizing credit ratings and financial statements remains essential, especially for corporate bonds where default risk is higher than with government securities.

Tax Implications

The tax treatment of bond income varies by bond type and investor circumstances. Municipal bonds, for instance, often offer tax-free interest at the federal level. Consulting a tax professional can help optimize your after-tax returns based on your specific situation.

Diversification Benefits

Incorporating short-term bonds into a broader portfolio smooths out volatility. When stock markets tumble, bonds often hold their value or even appreciate, providing balance. This stabilizing effect makes them invaluable for long-term wealth preservation, particularly for risk-averse investors or those nearing retirement.

Read more about Best Investment Strategies for Short Term Goals

![Saving Money Tips for Travel [Beyond Flights/Hotels]](/static/images/30/2025-05/MaximizingAccommodationChoices3ABeyondHotelsandResorts.jpg)

![Creating a Zero Based Budget [Beginner's Guide]](/static/images/30/2025-06/MaintainingYourZero-BasedBudget3ATipsforLong-TermSuccess.jpg)

![How to Buy and Sell Stocks [Beginner Steps]](/static/images/30/2025-06/ManagingYourPortfolio3ALong-TermStrategies.jpg)

Hot Recommendations

- How to Budget for Home Renovations

- Understanding Estate Taxes

- How to Dispute Errors on Your Credit Report

- How to Pay Off Credit Card Debt with Zero Interest Offers

- Understanding Algorithmic Trading (Basics)

- How to Save Money on Entertainment

- Understanding the Efficient Frontier in Portfolio Building

- Tips for Improving Your Credit Utilization Ratio

- Guide to Investing in Global Markets

- Saving Money Tips for Paying Off Debt Faster