How to Stick to Your Budget Every Month

Understanding Your Income

Accurately assessing your income is the cornerstone of any successful budget. This goes beyond just your paycheck—it includes bonuses, commissions, side gigs, and any other regular cash inflows. Documenting every source and estimating monthly amounts creates a clear snapshot of your financial capacity. This careful approach builds the framework for a practical budget.

Keep income projections realistic. Avoid overestimating earnings from unpredictable sources—conservative estimates prevent disappointment and help maintain long-term budget stability. Underestimating income, however, can create unnecessary financial pressure when meeting obligations.

Identifying Your Expenses

Categorizing expenses reveals spending patterns. Break down costs into essentials: housing, utilities, groceries, transportation, and debt payments. Detailed tracking helps spot overspending areas for better financial control.

Small purchases add up quickly. Regular reviews of minor expenses uncover hidden spending patterns and potential savings opportunities.

Prioritizing Essential Needs

Distinguishing needs from wants is critical. Focus first on housing, utilities, food, and transportation—these form the foundation of stable living. Properly funding these essentials prevents financial strain.

Evaluate true necessities carefully. While a new phone might seem essential, a refurbished model could meet needs while staying within budget. This discernment keeps spending aligned with priorities.

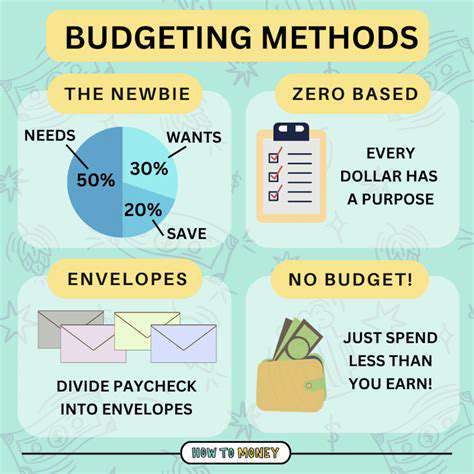

Creating a Realistic Spending Plan

Allocate income across expense categories carefully, avoiding overspending in any area. This requires analyzing income versus expenses to create a detailed yet adaptable plan. The best plans accommodate surprises while maintaining financial structure.

Include savings goals—even small regular contributions grow substantially over time. Budgeting for emergencies, short-term goals, and long-term investments builds financial security.

Tracking and Monitoring Your Progress

Regularly track income and expenses against your budget using spreadsheets or apps. This visibility into spending patterns highlights improvement opportunities.

Review budgets monthly to assess effectiveness and make adjustments. Consistent monitoring and adaptation keep budgets aligned with changing financial goals.

Adjusting and Refining Your Budget

Adapt budgets to life changes—promotions, income reductions, or unexpected costs all require adjustments. Flexibility ensures budgets remain practical through financial challenges.

Continually reassess spending to identify savings opportunities. Redirecting funds from unnecessary expenses to savings or debt repayment keeps budgets effective long-term.

Implementing a System for Monitoring and Adjustment

Defining Key Metrics for Budget Monitoring

Establish specific metrics tied to financial goals—track savings contributions, category spending against allocations, and income versus expenses. Regular reviews reveal trends and adjustment needs.

Establishing Clear Budget Categories

Create detailed spending categories (housing, food, transportation, etc.) with subcategories for granular tracking. This precision enables accurate monitoring and targeted adjustments.

Utilizing Budgeting Tools and Technologies

Leverage finance apps for automated tracking, categorization, and visual spending analysis. These tools simplify monitoring and highlight adjustment opportunities.

Regular Review and Analysis of Spending

Consistent spending reviews (weekly/monthly) identify overspending and savings potential, enabling timely budget corrections.

Implementing Adjustment Strategies

Address problem areas with specific tactics—spending limits, cheaper alternatives, or reduced frequency. Flexible approaches ensure sustainable adjustments.

Tracking Progress and Making Necessary Revisions

Regular progress reviews against goals determine if further adjustments are needed. This data-driven approach maintains budget effectiveness over time.

Custom wooden furniture showcases personal style and highlights exquisite craftsmanship.

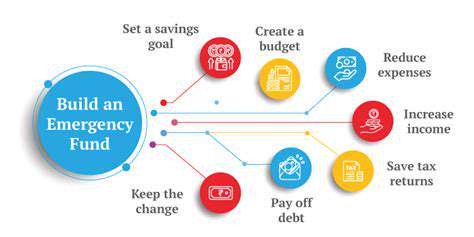

The Power of Automated Savings and Debt Repayment

Automating Savings for a Secure Future

Automated savings transforms financial stability by creating consistent deposits regardless of willpower. This builds substantial emergency funds and investment capital over time.

Simplifying Debt Repayment with Automated Transfers

Automatic debt payments prevent missed deadlines and credit damage while providing clear repayment progress visibility.

Strategic Allocation for Maximum Impact

Prioritize high-interest debts and categorize savings goals (emergency funds, retirement) to align automation with financial objectives.

Leveraging Technology for Effortless Financial Management

Banking apps and financial software automate transfers while providing real-time tracking—streamlining money management for greater efficiency.

Read more about How to Stick to Your Budget Every Month

![How to Build an Emergency Fund [Step by Step]](/static/images/30/2025-04/Step53AReplenishYourEmergencyFundWhenNecessary.jpg)

Hot Recommendations

- Tax Planning Tips for Homeowners [2025]

- How to Get Insurance for a Short Term Rental Property

- Understanding the Benefits of a Roth IRA

- How to Manage Business Debt After a Downturn

- How to Use a Barbell Investment Strategy

- Best Ways to Track Your Progress Towards Financial Freedom

- Tips for Managing Credit Card Rewards While Paying Off Balances

- Tax Planning Tips for Stock Options

- How to Plan for Retirement if You Didn't Save Early

- Guide to Managing Legal Debt