Beginner's Guide to Life Insurance

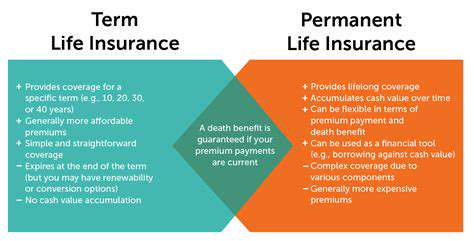

Understanding Term Life Insurance

When considering life insurance options, term life insurance stands out for its straightforward approach. It offers protection for a predetermined span, usually between 10 and 30 years. The policy only disburses benefits if the policyholder passes away within this timeframe. For families with growing children or homeowners paying off mortgages, this often proves to be the most budget-friendly solution. While initial premiums are typically lower, they may rise as the policy nears its end date.

What makes term life particularly appealing is its adaptability. Consumers can select various coverage lengths and benefit amounts, allowing them to modify protection as their life circumstances evolve. This characteristic makes it an ideal choice for those whose financial obligations change over time.

Exploring Permanent Life Insurance

Unlike its term counterpart, permanent life insurance guarantees lifelong protection provided premiums continue to be paid. While the monthly costs are generally steeper, these policies include a unique advantage: a cash value component that accumulates over the years. Policyholders can tap into this growing fund through loans or withdrawals when needed.

The permanent life category includes whole life and universal life variants, each with distinct characteristics. For individuals focused on legacy planning or long-term wealth preservation, these policies serve as powerful financial instruments. The choice between them depends largely on personal financial objectives and situations.

Comparing Coverage Amounts

Determining appropriate coverage levels requires careful analysis of current and anticipated financial responsibilities. Outstanding loans, childcare expenses, and future educational costs should all factor into this calculation. A thorough assessment of one's financial landscape is indispensable when selecting coverage limits.

Those with significant financial commitments like home loans or college-bound children typically need more extensive coverage. Conversely, individuals with stable finances and fewer dependents might opt for more modest protection levels.

Evaluating Policy Costs and Benefits

Premium affordability remains a primary consideration for most buyers. While comparing prices across providers, ensure the coverage meets your essential needs. Opting for the cheapest option might leave critical gaps in protection.

Examine each policy's supplementary features thoroughly. Additional protections like accidental death coverage or disability riders can significantly enhance a policy's value. For permanent life products, pay special attention to cash value growth potential and possible tax benefits.

Employee engagement transcends corporate jargon; it fundamentally impacts organizational performance. Committed employees demonstrate higher productivity and quality output, directly benefiting company results.

Choosing the Right Policy: Factors to Consider

Understanding Your Needs

Policy selection begins with comprehensive self-assessment. Evaluate your complete financial picture, including earnings, expenditures, and existing liabilities. This groundwork helps identify policies that align with both current realities and future aspirations.

Lifestyle factors and genetic predispositions also warrant consideration. High-risk occupations or family medical histories can substantially influence both coverage requirements and premium calculations.

Evaluating Different Policy Types

The insurance market offers diverse products addressing specific protection needs. While health insurance manages medical costs, life insurance provides family security. Grasping each policy type's distinctive features enables smarter purchasing decisions.

Property coverage safeguards physical assets against various threats, while liability protection shields against third-party claims resulting from accidents or injuries.

Assessing Coverage Options

Scrutinize the breadth of coverage across different providers. Significant variations exist between basic and comprehensive plans, making thorough comparisons essential. Pay particular attention to policy fine print detailing specific protections and limitations.

Never overlook coverage exclusions, as these often represent critical gaps that could prove costly when claims arise.

Analyzing Premium Costs

Premium comparisons between carriers help identify optimal value propositions. Balance affordability with adequate protection, considering how age, health status, and coverage levels affect pricing structures.

Considering Policy Length and Renewability

Temporal factors significantly impact policy suitability. Short-term solutions differ substantially from lifelong protections. Understanding renewal terms and long-term cost implications informs better financial planning. Weigh the advantages of each approach against your anticipated needs.

Seeking Professional Guidance

Insurance complexities often warrant expert consultation. Licensed agents can decode policy jargon and identify suitable options based on your unique profile. Their insights prove invaluable for uncovering hidden costs and comparing subtle differences between similar products.

Considering Future Needs

View insurance purchases as evolving components of your financial strategy. Regular policy reviews ensure continued alignment with changing life circumstances and financial goals. This proactive approach maintains appropriate protection levels throughout different life stages.

Read more about Beginner's Guide to Life Insurance

![Best Tools for Debt Management [2025]](/static/images/30/2025-05/DebtManagementPlans28DMPs293APersonalizedStrategiesforRepayment.jpg)

![How to Pay Off Credit Card Debt Fast [Proven Strategies]](/static/images/30/2025-05/StayMotivatedandConsistent3AKeytoLong-TermSuccess.jpg)

Hot Recommendations

- Tax Planning Tips for Homeowners [2025]

- How to Get Insurance for a Short Term Rental Property

- Understanding the Benefits of a Roth IRA

- How to Manage Business Debt After a Downturn

- How to Use a Barbell Investment Strategy

- Best Ways to Track Your Progress Towards Financial Freedom

- Tips for Managing Credit Card Rewards While Paying Off Balances

- Tax Planning Tips for Stock Options

- How to Plan for Retirement if You Didn't Save Early

- Guide to Managing Legal Debt