Guide to Understanding Retirement Account Rollovers

Important Considerations Before Initiating a Rollover

Planning for the Transition

When considering a retirement account rollover, smart investors know preparation is key. Starting the planning process several months before the actual transfer date can make all the difference. You'll want to thoroughly examine the new plan's investment choices, comparing fees and performance history. Don't forget to review your complete financial picture - current savings, debts, and expected retirement needs. This comprehensive approach helps avoid surprises down the road.

Each retirement plan comes with its own set of rules that can trip up the unwary. Missing important deadlines or paperwork requirements might lead to unnecessary penalties. That's why consulting with a financial professional who specializes in retirement accounts makes good sense. Their guidance can help navigate the regulatory maze smoothly.

Understanding Tax Implications

While rollovers typically defer taxes, the details matter tremendously. The tax treatment can vary significantly depending on whether you're moving between similar accounts or converting to a different type. For instance, shifting funds from a traditional IRA to a Roth IRA creates immediate tax obligations, unlike transfers between like accounts. These nuances underscore why tax planning should be part of your rollover strategy.

Tax professionals emphasize that one-size-fits-all advice doesn't apply to retirement account transfers. Your specific tax bracket, future income expectations, and state tax laws all play important roles. Getting personalized tax advice helps ensure you don't face unexpected bills come tax season.

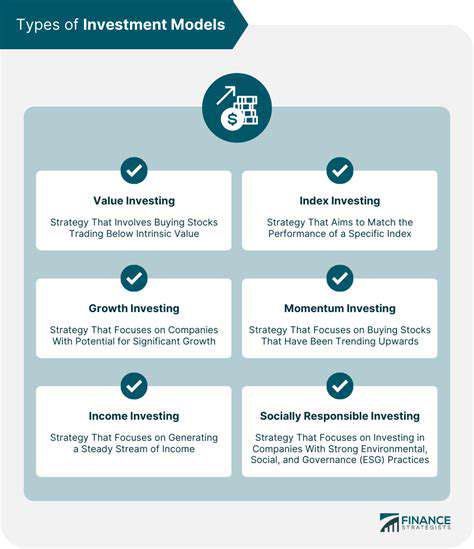

Evaluating Investment Options

The investment menu in your new plan deserves careful scrutiny. Compare not just the obvious factors like historical returns, but also the less visible costs - expense ratios, transaction fees, and account maintenance charges. Even small differences in fees can compound into significant sums over decades of retirement saving. Make sure the available options match your risk tolerance and time horizon.

Assessing Current Financial Situation

Before pulling the trigger on a rollover, take stock of your complete financial landscape. This means looking beyond just retirement accounts to consider debts, emergency funds, and other assets. Many financial advisors recommend having three to six months of living expenses set aside before making major retirement account changes. This buffer helps avoid the need for early withdrawals if unexpected expenses arise.

Your current income stability also factors into the decision. Those in transition between jobs or with irregular income might want to delay rollovers until their situation stabilizes. The dividend investing approach some retirees use illustrates how different financial strategies suit different life stages.

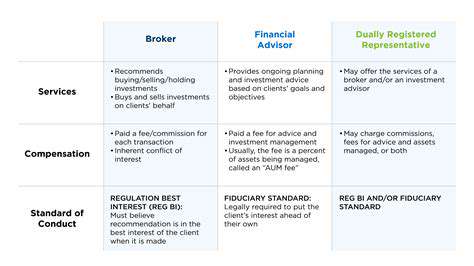

Considering Professional Guidance

While it's possible to handle a rollover independently, the complexity often justifies professional help. A good financial advisor does more than just paperwork - they can spot opportunities you might miss, like net unrealized appreciation strategies for company stock. They also stay current on changing regulations that might affect your transfer.

For those with substantial retirement savings, the cost of professional advice often pays for itself in avoided mistakes and optimized strategies. Think of it as an investment in your future financial security rather than just an expense.

Read more about Guide to Understanding Retirement Account Rollovers

![Best Renters Insurance Companies [2025 Review]](/static/images/30/2025-05/CompanyB3AExcellentCustomerService26ClaimsHandling.jpg)

![Best Investment Strategies for High Inflation Environments [2025]](/static/images/30/2025-05/BeyondtheBasics3AExploringAlternativeInvestments.jpg)

Hot Recommendations

- Tax Planning Tips for Homeowners [2025]

- How to Get Insurance for a Short Term Rental Property

- Understanding the Benefits of a Roth IRA

- How to Manage Business Debt After a Downturn

- How to Use a Barbell Investment Strategy

- Best Ways to Track Your Progress Towards Financial Freedom

- Tips for Managing Credit Card Rewards While Paying Off Balances

- Tax Planning Tips for Stock Options

- How to Plan for Retirement if You Didn't Save Early

- Guide to Managing Legal Debt