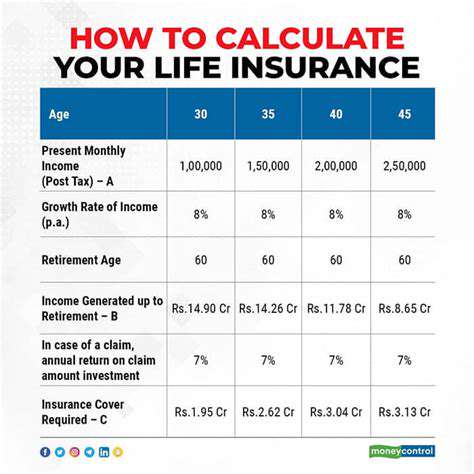

How to Choose the Right Amount of Life Insurance

Evaluating Debt Types

Not all debt is created equal. Federal student loans often have fixed rates and flexible repayment options, while credit cards typically charge steep interest that compounds daily. Recognizing these differences is like knowing which fires to put out first—some debts burn much hotter than others. Medical debt might have lower interest but can impact credit scores just as severely if left unpaid.

Analyzing Repayment Schedules

Calendar alerts can be financial lifesavers. Track every payment due date and note which debts have grace periods or late fees. Some creditors offer interest rate reductions for automatic payments—always worth asking about. This level of detail transforms chaotic money management into a strategic operation where you control the timeline. You might even discover you can align most bills with paydays for smoother cash flow.

Considering Potential Income Sources

Your financial picture isn't complete without examining all income streams. Beyond your primary job, consider freelance work, rental income, or dividends from investments. Many people overlook smaller but consistent income sources like online surveys or cash-back apps that could help chip away at debt. Documenting these helps create a realistic budget with breathing room.

Developing a Realistic Action Plan

Financial plans should evolve like fitness routines—what works today might need adjustment next year. Start with manageable steps, like paying an extra $20 toward high-interest debt each month. The most successful plans incorporate regular check-ins, celebrating small wins while staying flexible for life's inevitable curveballs. Consider setting quarterly money dates to review progress and make necessary tweaks.

Calculating Your Income Replacement Needs

Understanding Income Replacement

Income replacement planning acts as a financial safety net during job transitions or unexpected life events. It's not just about matching your salary—it's about maintaining your quality of life. This calculation separates those who weather financial storms from those who get swept away. Many professionals recommend having three to six months' worth of living expenses saved, but your ideal number depends on job stability and personal circumstances.

Potential income sources form a patchwork quilt of financial security. Savings accounts provide immediate access, while investments may offer growth potential. Government programs like unemployment insurance can bridge gaps, though benefits often cover only a fraction of normal income. The most robust plans weave together multiple threads of financial resources. Don't forget about less conventional options like rental income or monetizing hobbies during transitional periods.

Methods for Calculating Income Replacement

The percentage approach simplifies complex calculations—many experts suggest aiming to replace 70-80% of pre-tax income. However, new parents or those with hefty medical expenses might need closer to 100%. This method works well for quick estimates but may overlook specific financial obligations.

For precision, the expense-based method shines. Track every dollar spent for three months to create a detailed spending map. You'll likely find surprises—that daily coffee habit adds up, while some assumed expenses prove smaller than expected. This approach reveals exactly what income level maintains your current lifestyle.

Consulting a financial advisor brings professional perspective to the process. A good advisor doesn't just crunch numbers—they help navigate emotional financial decisions and spot opportunities you might miss. They can run scenarios showing how different strategies play out over time, from aggressive savings plans to investment approaches. Many offer free initial consultations to assess if their services match your needs.

Blending methods often yields the clearest picture. Use percentage estimates for long-term planning while expense tracking handles immediate needs. Regular updates ensure your plan stays relevant as life circumstances change—a plan made during singlehood likely needs revising after marriage or home purchase.

Considering Your Lifestyle and Goals

Understanding Your Needs

Personal finance isn't one-size-fits-all. A recent college graduate's priorities differ dramatically from someone nearing retirement. List non-negotiables first—housing, healthcare, debt payments—then layer in discretionary spending. This exercise often reveals surprising insights about what truly matters to you versus what's just habit.

Lifestyle considerations go beyond current spending. Future plans like starting a business or traveling the world require different financial preparations than more conventional paths. Self-employed individuals face unique challenges—irregular income demands larger cash cushions than traditional employment. Documenting these aspirations makes them tangible and achievable.

Assessing Your Financial Obligations

Debt assessment requires brutal honesty. That small credit card balance grows alarmingly when only making minimum payments. Mortgage calculators can show how extra payments shorten loan terms and save thousands in interest. Seeing these numbers in black and white often motivates more aggressive repayment strategies.

Future obligations deserve equal attention. College tuition costs rise faster than inflation—starting education savings early leverages compound growth. Anticipated home repairs or vehicle replacements shouldn't be surprises but planned expenses. Building these into your financial blueprint prevents future scrambling.

Considering Your Family's Needs

Family financial planning resembles a chess game—each move affects multiple pieces. Young children's needs evolve rapidly, from daycare costs today to orthodontics tomorrow. Creating separate savings buckets for different needs prevents one expense from derailing others. Regular family money discussions ensure everyone's on the same page about priorities and trade-offs.

Spousal considerations require delicate balance. Some partners prefer maintaining identical lifestyles, while others adapt to changed circumstances. Open conversations about expectations prevent resentment later. Remember that financial security isn't just about numbers—it's about peace of mind for those you love.

Evaluating Your Income and Earnings Potential

Income analysis should look backward and forward. Review pay stubs to understand net pay after taxes and deductions—the number that actually hits your bank account. Future projections might include expected raises, career changes, or potential part-time work in retirement. This dual perspective helps balance current needs with long-term planning.

For primary earners, consider how dependents would manage without that income. Life insurance calculators can help determine appropriate coverage amounts, but also think about non-financial contributions like childcare or home maintenance that would need replacing. Comprehensive planning addresses both the checkbook and the household logistics.

Seeking Professional Guidance

Understanding Your Needs

Professional advice becomes valuable when you hit financial complexity or decision paralysis. The first step is recognizing where you need help—is it investment strategy, tax planning, or debt management? Many people benefit most from help navigating major transitions like inheritance receipt or business startup. Clear objectives make the search for the right professional more efficient.

Preparation transforms generic advice into personalized strategy. Before meetings, organize financial documents and prepare specific questions. This shows respect for the professional's time while ensuring you cover critical topics. Think of it like a doctor's visit—the better you describe symptoms, the more accurate the diagnosis.

Identifying the Right Professional

The financial advice landscape contains various specialties—CFPs for comprehensive planning, CPAs for taxes, investment advisors for portfolio management. Credentials matter, but so does chemistry—you'll share personal details, so trust and comfort are essential. Interview multiple candidates, asking about their typical client profile and problem-solving approach. Many professionals offer free introductory meetings precisely for this matching process.

Fee structures vary widely—some charge percentages of assets managed, others hourly rates or flat fees. Understand exactly what services each fee covers and how often you'll meet. Transparency here prevents misunderstandings later. Don't hesitate to ask for references from clients with situations similar to yours.

Setting Realistic Expectations

Financial improvement resembles fitness journeys—visible results take time and consistent effort. Beware of anyone promising overnight solutions or guaranteed returns—legitimate professionals manage expectations, not manufacture false hope. Ask for sample timelines showing when you might expect to see certain milestones based on your specific situation and commitment level.

The professional's role is guide, not magician. They provide expertise and accountability, but implementation rests with you. Come prepared to discuss not just goals but also your willingness to make potentially uncomfortable changes. The most successful relationships balance professional guidance with personal responsibility.

Preparing for the Guidance Process

Maximizing professional value starts before the first meeting. Gather recent tax returns, pay stubs, investment statements, and debt information. Creating a simple net worth statement (assets minus liabilities) provides instant financial snapshot. Note any pressing concerns or upcoming decisions so these get addressed first. This preparation turns abstract discussions into concrete planning.

Consider keeping a money journal for two weeks—record all spending and any financial worries that arise. Patterns often emerge that even careful budget tracking misses. This qualitative data helps professionals understand not just your numbers but your money mindset and pain points.

Navigating Potential Challenges

Financial conversations can feel vulnerable—many people equate money with self-worth. Remember professionals have heard it all—no situation shocks them, and judgment-free guidance is their job. If certain topics feel uncomfortable, say so—good advisors will adjust their approach. It's better to address difficult subjects early than have them undermine progress later.

Implementation hurdles are normal. When recommendations feel overwhelming, ask about phased approaches—what's the minimum viable first step? Celebrate small victories to maintain motivation. Regular check-ins allow for course corrections before small detours become major wrong turns.

Sustaining Momentum and Achieving Results

Advice only creates value when implemented. Schedule follow-ups before leaving each meeting—this commits both parties to accountability. Treat financial plan updates like important medical check-ups—regular maintenance prevents major crises. Between meetings, note questions or changes in circumstances so nothing gets forgotten.

As progress occurs, revisit initial goals—some may need adjusting as life evolves. What seemed crucial a year ago might matter less now, while new priorities emerge. This dynamic approach keeps your financial strategy aligned with your actual life rather than some theoretical plan.

Read more about How to Choose the Right Amount of Life Insurance

![Best Homeowners Insurance Companies [2025 Review]](/static/images/30/2025-05/TopTierHomeownersInsuranceProvidersin2025.jpg)

![Best Tools for Debt Management [2025]](/static/images/30/2025-05/DebtManagementPlans28DMPs293APersonalizedStrategiesforRepayment.jpg)