How to Research Investment Funds

Defining Your Investment Goals

What exactly do you want your money to accomplish? Maybe you're saving for a home, preparing for retirement, or building a college fund for your kids. Clear goals act like a compass for your investment journey—they keep you moving in the right direction. Make them SMART: Specific, Measurable, Achievable, Relevant, and Time-bound.

Assessing Your Risk Tolerance

How do you feel when your investments take a dip? Some investors can watch their portfolio swing up and down without losing sleep, while others prefer steady, predictable growth. Knowing your comfort level with risk is crucial because different investments come with different levels of volatility. Choosing investments that match your risk tolerance helps prevent sleepless nights and financial regrets later.

Identifying Your Time Horizon

When will you need this money? Retirement savings might have a 30-year timeline, while a house down payment might need to be ready in 5 years. Your investment strategy should match this timeline. Time is your greatest ally—the longer your money can grow, the more risk it can typically weather. Short-term goals usually call for safer, more stable investments.

Exploring Different Investment Options

With your goals and risk profile in mind, you can start looking at investment types. Stocks might offer growth, bonds provide stability, while ETFs give you instant diversification. Real estate and precious metals can add variety to your portfolio. Each option has its own risk-reward balance that should align with your personal financial picture.

Considering Diversification Strategies

Don't put all your eggs in one basket—that's the golden rule of diversification. By spreading investments across different asset types, you reduce the impact if one investment underperforms. A diversified portfolio might include a mix of stocks for growth, bonds for stability, and other assets for balance. This approach helps smooth out the investment ride over time.

Seeking Professional Advice

While there's plenty you can learn on your own, a financial advisor can provide personalized guidance. They can help create an investment plan tailored to your unique situation and goals. Professional advice becomes especially valuable when dealing with complex financial situations or major life changes. Think of them as a co-pilot on your financial journey.

Pain generally falls into two categories: acute and chronic. Acute pain comes on suddenly, often from an injury, and typically fades as healing occurs. Chronic pain lingers, sometimes for months or years, and can affect every aspect of daily life. Recognizing which type you're dealing with is the first step toward effective treatment. The approaches for managing these pain types differ significantly, making early identification crucial.

Understanding the Fund's Investment Portfolio and Asset Allocation

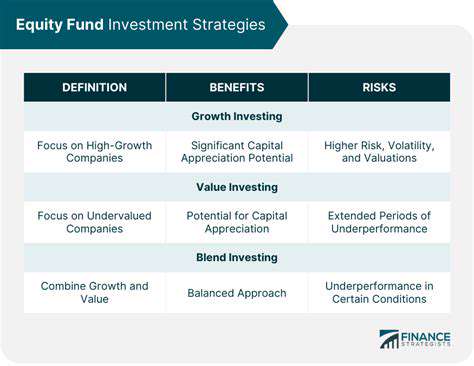

Understanding the Fund's Investment Strategy

Every mutual fund has a unique approach—some focus on steady value stocks, others chase fast-growing companies, while many blend both strategies. The fund's prospectus explains this philosophy in detail. This strategy document is like the fund's DNA—it reveals what makes the fund tick and how it might perform in different market conditions. Matching this strategy to your own goals is essential.

Evaluating Asset Allocation

Where a fund puts its money tells you about its risk level. Heavy in stocks? Expect more ups and downs. More bonds? Generally smoother sailing. The right allocation balances growth potential with your personal comfort zone for risk. It's about finding that sweet spot where you can sleep at night while your money works for you.

Analyzing the Fund's Holdings

Looking under the hood at a fund's actual investments reveals its true character. Are tech stocks dominating? Is there international exposure? These holdings show how the fund's strategy plays out in real investments, and whether it aligns with your vision for your portfolio.

Assessing the Fund Manager's Expertise

The person steering the fund matters. How long have they been at the wheel? How did they navigate past market storms? A seasoned manager with a consistent approach can be the difference between a good fund and a great one. Their track record doesn't guarantee future success, but it shows their ability to handle market challenges.

Considering the Fund's Historical Performance

Past performance isn't a crystal ball, but it can reveal patterns. Look beyond the best years—how did the fund weather economic downturns? Consistency across different market conditions often speaks louder than short-term spikes in performance.

Understanding the Fund's Expenses

Fees eat into returns, sometimes significantly. Compare a fund's expense ratio to similar options—lower costs mean more money stays in your pocket. Over decades, even small differences in fees can compound into substantial amounts.

Checking the Fund's Risk Profile

Every fund has its own risk fingerprint. Some bounce around with market swings, others hold steadier. Understanding this risk personality helps ensure it matches your own tolerance for investment ups and downs. The right fund should challenge your money to grow without challenging your peace of mind.

Read more about How to Research Investment Funds