How to Save for Retirement if You Start Late

You'll likely discover spending patterns that surprise you. Maybe you're spending more on dining out than groceries, or perhaps those small entertainment expenses add up to a significant chunk. This isn't about guilt—it's about awareness. Knowledge is power, and knowing exactly where your money goes gives you the power to redirect it toward what truly matters to you.

Evaluating Your Savings and Investments

Open all those financial statements you've been avoiding. List every account—checking, savings, retirement funds, brokerage accounts. Note their current balances and, crucially, their growth rates. That emergency fund sitting in a basic savings account? It might actually be losing purchasing power if it's not keeping up with inflation. Meanwhile, your investment accounts could be either outperforming or underperforming your expectations—you won't know until you look.

Compare your current savings rate to recommended benchmarks. Financial experts often suggest saving 15-20% of your income, but your ideal percentage depends on your goals and timeline. If there's a gap between where you are and where you want to be, don't panic—just start adjusting. Even small increases in your savings rate can create dramatic differences over time thanks to compound growth.

Debt Management

Gather every debt statement you have—credit cards, student loans, car payments, personal loans. Create a simple spreadsheet listing each debt's balance, interest rate, minimum payment, and due date. Seeing all your debts in one place can be overwhelming at first, but it's the crucial first step toward conquering them. You might notice that some small debts actually carry shockingly high interest rates, making them more urgent to pay off than larger but lower-interest debts.

Consider the snowball versus avalanche methods for debt repayment. The snowball method (paying smallest debts first for quick wins) works well for motivation, while the avalanche method (tackling highest-interest debts first) saves more money long-term. Choose the approach that best fits your personality and financial situation—the best debt strategy is the one you'll actually stick with.

Creating a Realistic Budget

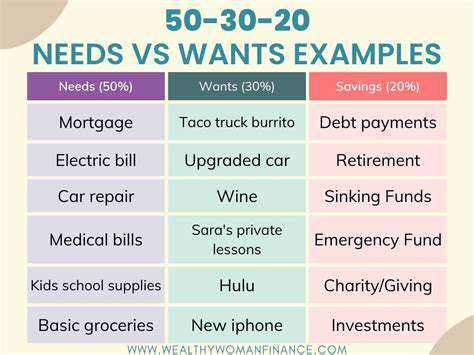

Budgeting isn't about restriction—it's about intentionality. Start with the 50/30/20 framework as a baseline: 50% for needs, 30% for wants, 20% for savings/debt repayment. Then customize it to your actual spending patterns and goals. The magic happens when you align your spending with your values—suddenly cutting back feels less like deprivation and more like choosing what matters most.

Build flexibility into your budget. Life happens—car repairs, medical bills, unexpected travel. Include a miscellaneous category (about 5-10% of your budget) for these surprises. Review and adjust your budget monthly at first—you'll likely need several iterations before it feels truly realistic. Remember, a budget is a living document, not a straitjacket.

Identifying Financial Goals

Dream big, then get specific. Instead of save more, try save $10,000 for a house downpayment in 18 months. Instead of pay off debt, aim for pay off $5,000 in credit card debt by December. The more vivid and measurable your goals, the more likely you are to achieve them. Write them down and place them where you'll see them daily—this constant reminder helps maintain focus when temptation strikes.

Balance short-term wins with long-term planning. Maybe you want to take a vacation next year (short-term) while also saving for retirement (long-term). Assign dollar amounts and timelines to each goal, then work backward to determine how much you need to save monthly. Celebrate milestones along the way—financial responsibility shouldn't mean joyless deprivation.

Leveraging Investment Strategies for Growth

Diversifying Your Portfolio for Long-Term Gains

Think of diversification like nutrition—you need a balanced diet of different asset classes for financial health. Stocks offer growth potential but come with volatility. Bonds provide stability but often lower returns. Real estate and commodities behave differently still. The sweet spot lies in finding your personal risk tolerance—that point where you can sleep at night while still pursuing meaningful growth. A good rule of thumb: subtract your age from 110—that's the percentage you might consider allocating to stocks, with the rest in bonds and other assets.

Rebalancing is diversification's often-overlooked partner. Market movements will naturally throw your carefully planned allocations out of whack over time. Set a reminder to rebalance quarterly or annually—selling some of what's done well to buy more of what's underperformed. This disciplined approach forces you to buy low and sell high without emotional decision-making.

Implementing a Consistent Investment Schedule for Future Security

Automation is the unsung hero of investing success. Set up automatic transfers from your paycheck or checking account to investment accounts—treat these like any other non-negotiable bill. This set it and forget it approach removes emotion from investing and harnesses the power of dollar-cost averaging. You'll naturally buy more shares when prices are low and fewer when they're high, smoothing out market volatility over time.

Increase contributions gradually. If saving 15% of your income feels impossible right now, start with 5% and schedule automatic 1% increases every six months. You'll adjust to slightly smaller paychecks without feeling the pinch. Whenever you get a raise, divert at least half of it to investments before lifestyle inflation creeps in. These small, consistent steps create massive results over decades.

Mindfulness is the practice of being present in the moment, fully engaging with the here and now without judgment. It involves acknowledging your thoughts, feelings, and sensations without trying to change or suppress them.

Creating a Realistic Savings Timeline and Budget

Understanding Your Current Financial Situation

Track every dollar for 30 days—no exceptions. You'll likely discover money leaks—those small, frequent expenses that add up without you noticing. Maybe it's unused subscriptions, convenience fees, or premium services you don't actually need. Plugging just a few of these leaks can free up hundreds annually with minimal lifestyle impact. Compare your spending to regional averages—are you spending significantly more on housing or transportation than similar households?

Establishing Realistic Retirement Goals

Envision your ideal retirement day. Are you traveling? Volunteering? Pursuing hobbies? Now price it out. Healthcare often surprises people—a couple retiring at 65 might need $300,000 just for medical expenses. Break massive retirement numbers into manageable chunks—saving $1 million sounds impossible, but $500/month at 7% return gets you there in 40 years. Use multiple calculators (try the AARP, Fidelity, and Vanguard tools) to cross-check estimates.

Developing a Savings Strategy

Stack your savings vehicles strategically. First, contribute enough to your 401(k) to get any employer match—that's free money. Next, max out a Roth IRA for tax-free growth. Then circle back to your 401(k) or consider a taxable brokerage account. This bucket approach optimizes both tax advantages and accessibility of funds at different life stages. Don't forget about HSAs if you have a high-deductible health plan—they offer triple tax advantages and can become a stealth retirement account after age 65.

Creating a Detailed Budget

The envelope system goes digital. Allocate virtual envelopes for spending categories using apps like YNAB or Goodbudget. When the dining-out envelope empties, no more restaurants until next month. This creates natural accountability without the rigidity of traditional budgets. Build in a fun money category—complete deprivation leads to budget rebellion. Even 5% of your income spent guilt-free on whatever you want makes the other 95% discipline easier to maintain.

Tracking Progress and Making Adjustments

Schedule quarterly money dates—review accounts, track progress toward goals, and adjust as needed. Did you get a raise? Increase savings accordingly. Unexpected medical bill? Temporarily reduce discretionary spending to compensate. Regular check-ins prevent small drifts from becoming major course corrections. Celebrate wins—paid off a credit card? Treat yourself to a modest reward. Positive reinforcement builds lasting financial habits.

Utilizing Retirement Planning Tools

Beyond basic calculators, explore Monte Carlo simulations that test your plan against thousands of possible market scenarios. Personal Capital's Retirement Planner and Fidelity's Retirement Score offer particularly robust analyses. Remember, tools provide guidance, not guarantees—use them to identify potential gaps, not predict the future. Consider consulting a fee-only financial planner for a one-time checkup if you feel overwhelmed—sometimes professional perspective is worth the investment.

Read more about How to Save for Retirement if You Start Late

![Best Health Insurance Plans for Families [2025]](/static/images/30/2025-05/EvaluatingCoverageandBenefits.jpg)

![Best Travel Insurance Policies [2025 Review]](/static/images/30/2025-05/CrucialConsiderations3ATripTypeandDestinationImpact.jpg)