How to Understand Investment Fees

Understanding Fee Structures

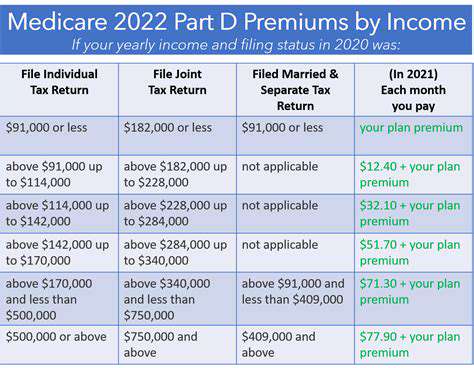

Investment fees are often overlooked, but they can significantly impact the overall return on your investment. Understanding the different types of fees, such as management fees, transaction fees, and advisory fees, is crucial for accurately calculating the true cost. These fees are often expressed as percentages of the assets under management, or as flat annual charges, and can vary widely between different investment products and platforms. It's important to scrutinize the fee structure to understand how they will affect your investment's performance over time, and to compare different investment options based on their total expense ratios.

Different investment vehicles, such as mutual funds, exchange-traded funds (ETFs), and individual stocks, typically have varying fee structures. Knowing these differences is vital to making informed investment decisions. For example, mutual funds often have ongoing management fees, whereas ETFs typically have lower expense ratios. Understanding the specifics of these fees can help you determine which investment vehicle aligns best with your financial goals and risk tolerance.

Impact of Fees on Long-Term Returns

The cumulative effect of fees over a long investment timeframe can be substantial. Even seemingly small fees can erode returns significantly if left unaddressed. Compounding fees over decades can dramatically reduce the overall gains you might otherwise achieve. Careful consideration of the potential fee implications is essential, as it can affect your portfolio's growth trajectory.

Investors need to be aware that these fees are not just added at the start; they are deducted periodically throughout the investment period. This consistent deduction, even if small, can subtract from the growth potential of the investment. Therefore, evaluating the long-term impact of fees on potential returns is vital for reaching financial goals.

Comparing Fee Structures Across Platforms

Investment platforms vary significantly in their fee structures. Some platforms offer lower fees for certain investment types, while others may charge higher fees for access to specialized or exotic investment opportunities. Comparing the fee structures of different platforms is essential to finding the best fit for your investment needs. Thorough research into the different fee schedules can help investors avoid unnecessary cost burdens.

Fee Implications on Different Investment Strategies

Different investment strategies, such as active management or passive index funds, have varying fee implications. Active management often comes with higher management fees, while passive index funds typically have lower expense ratios. Understanding which strategy aligns with your investment goals and risk tolerance is important for assessing the associated fee implications. Investors must consider how these differing fee structures will affect their investment returns over time.

Calculating the Net Return After Fees

To get a truly accurate picture of your investment's profitability, you must calculate the net return after accounting for all fees. This involves subtracting all applicable fees from the gross returns. This precise calculation is essential for evaluating the actual performance of your investments. By calculating the net return, investors can make more informed decisions regarding their portfolios and their financial future.

Tax Implications of Investment Fees

Investment fees can have tax implications, depending on the type of fee and the applicable tax laws. Understanding these tax implications is crucial for accurately calculating the true cost of your investments. Certain fees might be tax-deductible or subject to different tax rates. Careful consideration of the tax implications of investment fees is vital for optimizing your overall financial strategy.

Every great gallery wall starts with a showstopping centerpiece that commands attention. That anchor piece should be something that makes visitors pause - maybe it's your largest canvas, a photograph with striking contrast, or a sculpture with unusual textures. Try hanging it about 57 inches from the floor (eye level for most adults) and slightly left of center, since our eyes naturally travel there first when entering a room.

Strategies for Minimizing Investment Fees

Diversification: Spreading Risk

A crucial strategy for minimizing investment risk is diversification. Instead of putting all your eggs in one basket, diversification involves spreading your investments across various asset classes, such as stocks, bonds, real estate, and even precious metals. This approach helps mitigate the impact of a downturn in any single investment area. By diversifying, you can potentially limit the overall volatility of your portfolio and reduce the chance of significant losses.

Diversification also extends to within asset classes. For example, within the stock market, you could invest in different sectors, like technology, healthcare, and consumer goods. This further spreads risk by reducing the impact of a potential downturn in a specific sector. Holding a mix of stocks, bonds, and other assets can help to balance out the performance of your portfolio, making it more resilient to market fluctuations.

Risk Tolerance Assessment

Understanding your risk tolerance is paramount to developing a sound investment strategy. Consider how comfortable you are with the potential for your investments to fluctuate in value. A higher risk tolerance often corresponds to a portfolio with a greater allocation to stocks, which tend to offer higher potential returns but also carry higher volatility.

Conversely, a lower risk tolerance might lead to a portfolio emphasizing safer assets like bonds. This approach prioritizes stability and preservation of capital over aggressive growth. A thorough assessment of your risk tolerance should be a cornerstone of any investment strategy, helping to ensure you feel confident and comfortable with your chosen approach.

Long-Term Perspective

Investment success often hinges on a long-term perspective. Markets are inherently cyclical, and short-term fluctuations are common. Focus on achieving your long-term financial goals, whether it's retirement, a down payment on a home, or funding your children's education. This long-term view allows you to weather market downturns and benefit from market recoveries.

Avoid making impulsive decisions based on short-term market movements. A long-term focus helps you stay disciplined and committed to your financial plan, even when faced with temporary setbacks.

Dollar-Cost Averaging (DCA)

Dollar-cost averaging is a disciplined investment strategy that can help smooth out the volatility of the market. Instead of investing a lump sum all at once, DCA involves investing a fixed amount of money at regular intervals, such as weekly or monthly. This approach can help you buy more shares when prices are low and fewer shares when prices are high. This method helps to reduce the impact of market fluctuations and can potentially lead to more consistent long-term growth.

Regular Review and Adjustments

Investment strategies are not static; they should be regularly reviewed and adjusted to adapt to changing circumstances and market conditions. Periodically evaluate your investment portfolio to ensure it aligns with your current financial goals and risk tolerance. Regular reviews allow you to make necessary adjustments to your asset allocation and rebalance your portfolio to maintain the desired risk profile.

Life events, such as marriage, the birth of children, or career changes, can significantly impact your financial goals. Regular review allows you to adapt your investment strategy to accommodate these changes and ensure you remain on track to achieve your long-term objectives.

Read more about How to Understand Investment Fees

![How to Cut Unnecessary Expenses [Actionable Steps]](/static/images/30/2025-05/NegotiatingBillsandUtilizingDiscounts.jpg)

![Best Car Insurance Companies in 2025 [Review]](/static/images/30/2025-05/CustomerServiceandClaimsHandling3AACrucialAspect.jpg)

Hot Recommendations

- Tax Planning Tips for Homeowners [2025]

- How to Get Insurance for a Short Term Rental Property

- Understanding the Benefits of a Roth IRA

- How to Manage Business Debt After a Downturn

- How to Use a Barbell Investment Strategy

- Best Ways to Track Your Progress Towards Financial Freedom

- Tips for Managing Credit Card Rewards While Paying Off Balances

- Tax Planning Tips for Stock Options

- How to Plan for Retirement if You Didn't Save Early

- Guide to Managing Legal Debt