Guide to Understanding 529 Plans (Education Savings)

Contribution Limits and Eligibility

Contribution limits vary by state and plan. It's essential to research the specific limits for the state's 529 plan you are considering. Eligibility for 529 plans often depends on the relationship between the account holder and the beneficiary. Typically, the beneficiary is a dependent or family member who is pursuing or will pursue higher education.

Understanding these limits and eligibility requirements is crucial to ensure you're maximizing the benefits of the plan and avoid potential issues down the line.

Investment Options and Growth

529 plans typically offer various investment options, ranging from conservative to aggressive. The investment choices can significantly impact the growth potential of the account over time. Carefully considering these options and selecting investments that align with your risk tolerance and long-term financial goals is essential to maximize potential returns.

Tax Advantages of 529 Plans

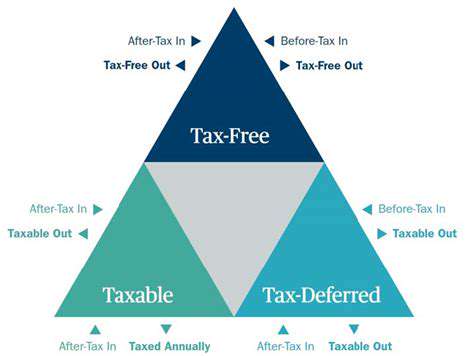

One of the key advantages of 529 plans is the tax-advantaged growth. Contributions are often made with after-tax dollars, but any earnings within the account grow tax-deferred. This means that the money grows without being taxed until it's withdrawn for qualified education expenses. This can significantly reduce the overall cost of education by saving on taxes.

Qualified Educational Expenses

Qualified educational expenses are crucial for understanding how 529 plans work. These expenses must be directly related to tuition, fees, room and board, or books for eligible educational institutions. Understanding the specific criteria for qualified expenses is essential to ensure that withdrawals are used for their intended purpose and avoid penalties.

It's important to note that not all education-related expenses are qualified. Understanding the specifics is crucial to avoid unnecessary penalties and ensure the funds are used effectively.

Withdrawal Rules and Penalties

529 plans have specific rules regarding withdrawals. Withdrawals used for qualified education expenses are typically tax-free and penalty-free. However, withdrawals for non-qualified expenses may be subject to income tax and a 10% penalty. Understanding these rules is crucial to avoid potential financial penalties and maximize the benefits of the plan.

Different Types of 529 Plans: Choosing the Right Fit

Traditional 529 Plans

Traditional 529 plans are the most common type and offer a flexible way to save for higher education expenses. These plans typically allow for contributions from both the student and the family, and the earnings grow tax-deferred. This means you don't pay taxes on the investment growth until the money is withdrawn for qualified education expenses. This can lead to significant savings over time, as the tax-advantaged nature of the plan allows your investments to compound more quickly. Choosing a traditional 529 plan can be a great way to secure your child's future education funding, leveraging tax benefits and potentially higher returns.

With a traditional 529 plan, you have the freedom to invest in different asset classes to potentially maximize your returns. However, it's crucial to understand the potential tax implications of withdrawals for non-qualified expenses, and to ensure your contributions and withdrawals align with your long-term financial goals. While the tax benefits are compelling, it's wise to consult with a financial advisor to ensure the plan aligns with your specific circumstances and financial strategy.

529 Prepaid Tuition Plans

Unlike traditional 529 plans that invest the contributions, prepaid tuition plans allow you to pay for future tuition at participating colleges and universities in advance. This approach locks in tuition rates at the time of purchase, providing a degree of certainty and protection against future tuition increases. This approach can be particularly beneficial if you know the institution your child will attend and want to secure the tuition cost at that time. However, if the intended institution changes, you may face challenges or penalties.

Prepaid tuition plans offer a guaranteed cost for future tuition, but they are tied to specific institutions. If your child's educational path takes a different direction, you might not be able to use the funds as flexibly as with a traditional 529 plan. Careful consideration of the institution and your child's potential future educational needs is essential when selecting a prepaid plan.

Coverdell Education Savings Accounts (ESAs)

Coverdell ESAs are another option for saving for education expenses, but they have some limitations compared to 529 plans. These accounts are often more restrictive in terms of contribution limits and are only available to families with lower incomes, as eligibility is based on adjusted gross income guidelines. While the tax advantages of Coverdell ESAs are attractive, understanding the specific limitations and income requirements is crucial before you choose this option.

The contribution limits for Coverdell ESAs are generally lower than those for 529 plans, which might make them less suitable for covering the entire cost of higher education. This type of account is a worthwhile alternative if you're looking for a modest saving plan that is tax-advantaged.

State-Specific 529 Plans

Numerous states offer their own 529 plans, often with specific investment options and tax benefits tailored to that particular state. These state-specific plans can provide access to unique investment opportunities or additional state tax advantages. Understanding the specific features of your state's 529 plan can help you optimize your savings strategy. Research the different state plans thoroughly to see if any offer additional tax benefits that might be particularly beneficial to your situation.

Roth 529 Plans

Roth 529 plans allow for after-tax contributions, but withdrawals for qualified education expenses are tax-free. This means that while you contribute after-tax dollars, you avoid paying taxes on the earnings when withdrawing funds for qualified educational expenses. This type of plan can be particularly appealing to those who want to maximize their tax savings potential. However, the lack of upfront tax benefits might make them less attractive in situations with high current tax burdens.

Choosing the Right Plan for Your Needs

Ultimately, the best 529 plan for you depends on your individual circumstances, financial goals, and the specific needs of your child. Consider factors such as your income, investment strategy, and projected education costs. Careful analysis of the various options, including traditional, prepaid, and state-specific plans, can lead to an informed decision. Seeking professional advice from a qualified financial advisor can help navigate the complexities and make the best choice to support your child's future educational aspirations.

Understanding Investment Options and Fees

Understanding Diversification

Diversification is a crucial aspect of any investment strategy, and it involves spreading your investments across a variety of assets to mitigate risk. By not putting all your eggs in one basket, you reduce the impact of any single investment's poor performance on your overall portfolio. This strategy can help you weather market fluctuations and potentially achieve more consistent returns over the long term. Diversification is a proactive approach to managing risk in the investment world. It helps to ensure that market downturns or sector-specific issues don't completely derail your investment goals.

Different asset classes, such as stocks, bonds, real estate, and commodities, have varying levels of correlation. Diversifying across these classes helps to balance out potential losses in one area with gains in another. This balance is essential for long-term investment success, allowing your portfolio to adjust to market changes more effectively. Understanding the correlation between different asset classes is key to creating a well-diversified investment portfolio.

Exploring Different Asset Classes

Stocks represent ownership in a company, offering the potential for substantial returns but also carrying higher risk. Bonds, on the other hand, are essentially loans to corporations or governments, providing more stable returns and lower risk. Real estate investments can offer both income and potential capital appreciation, but they often involve higher transaction costs and complexities.

Commodities, such as gold or oil, can serve as a hedge against inflation or currency fluctuations. Considering these diverse asset classes is essential for building a balanced and resilient investment portfolio. Each class has unique characteristics and risks, so careful consideration is paramount.

Evaluating Risk Tolerance

Your risk tolerance significantly influences your investment choices. A high-risk tolerance might lead you to invest heavily in stocks, seeking potentially higher returns, while a low-risk tolerance might favor bonds or other less volatile investments. Understanding your risk tolerance is a crucial step in creating an investment plan that aligns with your personal financial goals and comfort level.

It's important to be realistic about your risk tolerance, considering your financial situation, time horizon, and personal circumstances. You should seek professional advice if necessary, as a financial advisor can help you assess your risk tolerance objectively and recommend appropriate investment strategies. Accurately assessing your risk tolerance is critical to avoid impulsive or emotionally driven investment decisions.

Understanding Investment Time Horizons

Your investment time horizon greatly affects your investment strategy. A longer time horizon, such as retirement planning, allows for a more aggressive approach with a higher allocation to potentially higher-growth assets. Conversely, a shorter time horizon, such as saving for a down payment, might necessitate a more conservative approach focused on preserving capital.

Short-term investments prioritize liquidity and safety, while long-term investments are designed to ride out market fluctuations and potentially generate significant returns. Understanding your time horizon is paramount to creating an investment plan that aligns with your specific needs and goals. This crucial element should be a key component of your investment strategy.

The Importance of Professional Advice

Seeking professional financial advice can significantly benefit your investment journey. A qualified financial advisor can help you develop a personalized investment strategy, taking into account your specific circumstances, goals, and risk tolerance. They can guide you through complex investment options and provide ongoing support and adjustments as your needs evolve.

They can also offer insights into market trends, economic forecasts, and potential investment opportunities. Financial advisors are valuable resources for navigating the complexities of the investment world and making informed decisions. Seeking expert advice is often a necessary step to ensure your investment decisions are aligned with your long-term financial goals.

Read more about Guide to Understanding 529 Plans (Education Savings)

![How to Stop Impulse Buying and Save Money [Budgeting Tips]](/static/images/30/2025-06/BuildinganEmergencyFund3APreventingFinancialCrisesandReducingStress.jpg)